Worried that the Federal Reserve is driving our economy off a cliff?

I’ve got two words for you:

Drugs ‘n diapers.

Actually, I forgot one. Dividends.

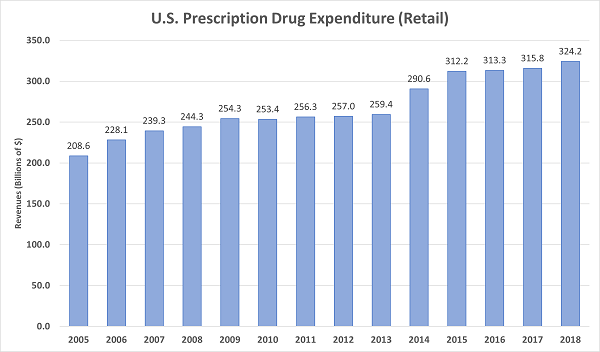

These companies are about as recession-resistant as they come. Let’s start with drugs because, well, it’s always a bull market on prescription spend in America:

Source: Centers for Medicare and Medicaid Services

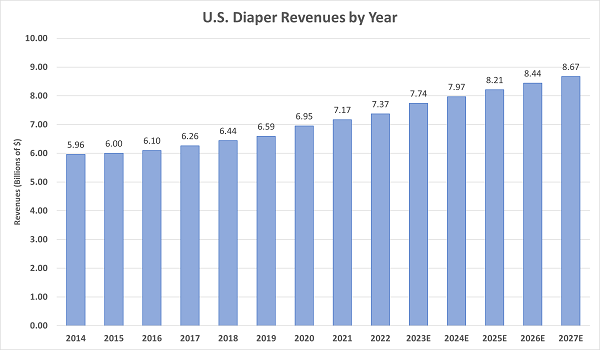

While some of us are popping pills, others are changing diapers. (Or using them—we don’t judge!)

Without naming names we can see that someone is making consistent deposits. The trajectory of diaper spend is a one-way trade, too:

Data source: Statista Market Insights

Let’s start on the changing table with a 2.5% payer and work our way up. Or front to back. (Sorry, couldn’t resist the girl dad joke.)

Procter & Gamble (PG)

Dividend Yield: 2.5%

The diaper business is extremely concentrated among just a few players. In fact, nine of the top 10 brands by revenue worldwide are owned by just two companies:

Procter & Gamble (PG) and Kimberly-Clark (KMB)

The former is responsible for Pampers and Luvs, as well as relative newcomer All Good, launched in 2020 specifically for sale in Walmart (WMT) stores.

Of course, Procter & Gamble offers many more pivotal consumer staples products, including as Head & Shoulders and Herbal Essences shampoos, Crest and Oral-B dental products, Olay and Secret personal care brands, Tide and Gain laundry detergents, Cascade and Mr. Clean home care, Bounty paper towels, and Charmin toilet paper. (And those are just some of P&G’s biggest brands.)

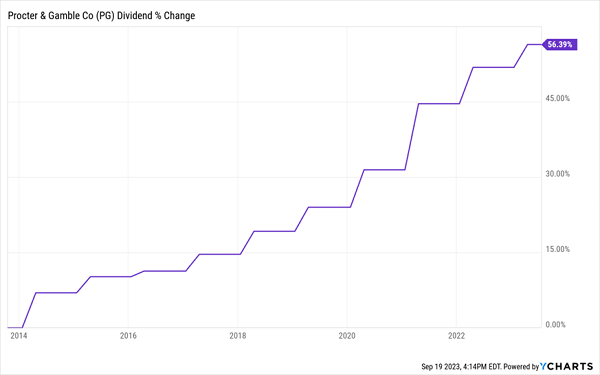

P&G is one of the longest-standing Dividend Aristocrats, boasting 67 consecutive payout hikes (and 133 consecutive years of dividends paid). That includes a 3% increase announced earlier this year.

Usually, when a company has improved dividends for as long as P&G has, dividend hikes tend to get a little chintzy thanks to slowing profit growth and a typically high payout ratio. But P&G is spryer than you’d think. Only a little more than 60% of profits are going toward the dividend—high, but not so high that the company is capable of only token raises going forward—and indeed, dividend growth has been at least respectable over the past decade.

Procter & Gamble: Good (Not Great, But Good) Dividend Growth

The big downside? Headline yield. Procter & Gamble delivers a mere 2.5% right now, which is less than many plain-vanilla dividend ETFs.

That’s not to say PG is a lousy long-term holding—far from it. But if investors do flock toward income amid an economic stumble, P&G probably won’t be a top beneficiary.

Kimberly-Clark (KMB)

Dividend Yield: 3.5%

While not ideal, Kimberly-Clark’s (KMB) 3%-plus dividend is at least another step in the right direction.

Kimberly-Clark is responsible for Huggies, Pull-Ups, KleenBebé, Goodnites, DryNites and Little Swimmers diapers. And like P&G, it’s a broader consumer staples giant, boasting massive brands including Kleenex tissues, Cottonelle and Scott toilet paper, Viva paper towels, Kotex feminine care and Depend adult care.

KMB shares have been both volatile and unproductive for years. While shares quickly rebounded from their COVID drop and even eked out some gains, Kimberly-Clark’s stock is virtually flat from the start of 2020—even when including dividends. Consumer staples as a whole have underperformed the market in that time, but not by nearly so much.

Kimberly-Clark: Virtually Nothing to See Here

Among KMB’s issues have been high input costs—indeed, margins still remain lower than their pre-COVID levels. Also hobbled is K-C Professional, which took a hit from the mass exodus from offices.

It’s a mixed bag on the income front, too. On the one hand, Kimberly-Clark is another longtime Aristocrat that has delivered more than half a century of uninterrupted dividend growth, and it delivers a better yield than P&G. However, its dividend growth has been slightly less robust over the past decade or so, and its payout ratio is higher, at 72%. That’s not to say KMB’s dividend will suddenly implode, but the potential for dividend growth isn’t quite as high.

Pfizer (PFE)

Dividend Yield: 4.8%

We can find more substantial, attractive yields in the healthcare space right now, starting with pharmaceutical giant Pfizer (PFE).

Pfizer, of course, gained some acclaim during the pandemic for creating one of the primary COVID-19 vaccines as well as antiviral Paxlovid. But it boasts dozens of pharmaceuticals and other treatments, including Eliquis (blood clots), Prevnar (pneumococcal disease), Vyndaqel (cardiomyopathy), Xeljanz (arthritis) and Ibrance (breast cancer).

Like with many pharma companies, Pfizer constantly has to refresh its pipeline to make up for revenues that are about to fall off the patent cliff. In PFE’s case, it has to make up for $17 billion worth of revenues that it’ll lose between 2025 through 2030. Fortunately, Pfizer has a deep pipeline—over the next 18 months alone, it’s expected to launch some 19 products or indications, 15 of which are from its own R&D. Pfizer has been plenty acquisitive, too, however, snapping up Global Blood Therapeutics and Biohaven, and it’s currently in the process of buying Seagen.

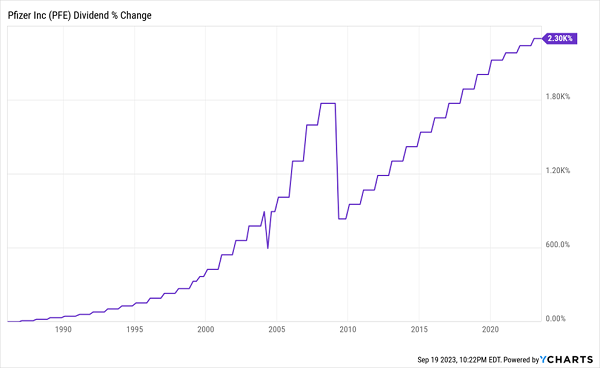

While Pfizer has a rich dividend history of more than 80 years’ worth of consecutive payouts, its dividend increase track record isn’t quite as robust—it has hiked for a little more than a decade following its 2009 cut alongside its $68 billion buyout of Wyeth.

Pfizer Has Been Good About Raising Dividends, But Its Track Record Isn’t Unblemished

That said, the payout is up about 70% over the past decade or so. And Pfizer has a lot of room to raise—only a bit more than 40% of profits go to fund the dividend right now.

Viatris (VTRS)

Dividend Yield: 4.9%

Pfizer also has a connection to another high-yielding pharma name: Viatris (VTRS), which was formed in 2020 when Mylan merged with Upjohn, Pfizer’s off-patent branded and generic established medicines business.

The Viatris portfolio includes a number of juggernauts that, even if off-patent, still generate considerable revenues. That includes Lipitor (cholesterol), Norvasc (blood pressure), Lyrica (nerve and muscle pain), EpiPen (allergic reactions), Viagra (erectile dysfunction), Zoloft (depression) and Xanax (anxiety).

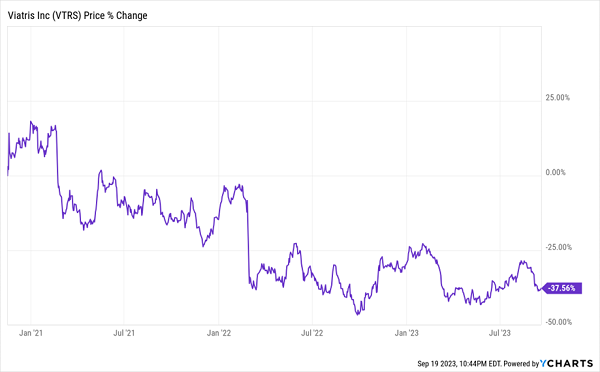

Despite this lineup, VTRS has been in a deep funk ever since its formation:

VTRS Is Hardly a Picture of Health

This is a company that’s still trying to find itself. Right now, it’s trying to divest non-core assets and low-margin businesses while investing in higher-margin businesses. Recent moves including buying up Tyrvaya (dry eye disease) and selling its biosimilars portfolio.

Because it was formed by merger, Viatris’s dividend history is difficult to splice, and thus not helpful for understanding where it’s going. Worryingly, however, the company’s last dividend hike was a 9% bump in January 2022—so it’s long overdue for a raise.

It’s not that VTRS can’t afford it—dividends account for just 30% or so of profits. But the company has a strong focus on paying down debt and buying back shares, which is a distraction from appeasing income-minded folks like us.

Organon (OGN)

Dividend Yield: 5.9%

We’re getting a fairly juicy yield with Organon (OGN), the spinoff of several Merck (MRK) businesses.

Specifically, Organon is made up of Merck legacy products (62% of revenues), women’s health treatments (27%), biosimilars (8%) and other drugs (3%). Treatments include Singulair (allergies/asthma), Nasonex (allergies), Atozet (cholesterol), NuvaRing (birth control) and Nexplanon (birth control).

And like with Viatris, Organon has had a difficult go of things:

Why Is a Broad-Based Pharma Stock Dropping This Much?

Organon’s woes are fairly straightforward: Like with Viatris, Organon was a dumping ground for (among other things) older treatments, which allowed Pfizer and Merck, respectively, to focus on growth. Revenues for many of these products are unsurprisingly flat or in decline.

So, why would we buy stocks like OGN?

Well, the dividends, for one—Organon, at a nearly 6% yield, pays out 4x what the market does. Also, Organon has a decent business case. This is a diversified pharmaceutical portfolio with a specialization in women’s health, which is expected to be a $50 billion market by 2025. Also, OGN is largely expected to deploy capital into M&A to rejuvenate its growth.

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

But like Viatris, Organon is a company that’s still trying to get its feet on solid ground. Is it a potential bounce-back candidate? Sure. But is it the kind of stock you want to depend on to keep your retirement portfolio buoyant during a recession? I have my doubts.

No, for now, I’m sticking with a small, overlooked basket of recession-resistant stocks that haven’t just been surviving over the past couple years of market tumult—they’ve been thriving.

In fact, they look like they could be the market’s best protective plays for the recession to come, regardless of whether it hits during the last few months of 2023 or sometime in 2024.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here to get a copy of my 5 Recession-Resistant Dividend Stocks With 100% Upside report, including full analyses of each pick … and I’ll throw in a few other bonuses, too!

Recent Comments