Monthly dividend stocks baby. Most income investors don’t even realize they exist!

Out of the few thousand stocks that trade publicly, only a few dozen pay monthly dividends. These hidden gems tend to have market caps in the hundreds of millions rather than billions.

Their relative obscurity is perfect for us. We’ll take them over their blue-chip quarterly cousins.

Quarterly dividends are pay days we prefer not to wait for. Plus, the payouts typically disappoint.

Let’s consider the distributions from a $500,000 portfolio split evenly among a group of five mega-cap dividend payers. These are uber-popular, widely held blue chips that you’ll see near the top of most major large-cap funds. Unfortunately their payment schedules all over the place and their yields are miserable, too!

Quarterly Payouts: Small and Erratic

Source: Income Calendar

But look at how much easier our retirement planning becomes if we take the same $500,000 nest egg and spread it across the five monthly dividends we’ll review today.

Monthly Payouts: Meaningful and Steady

Source: Income Calendar

Most monthly dividend payers fall within the high-yield acronyms—real estate investment trusts (REITs), business development companies (BDCs), etc. That’s great in that we can typically count on monthly payers to be bountiful payers, too.

But it does require us to sniff out whether these 5.8%-15.6% payouts are just par for the industry course, or whether they’re distressed dividends that could end up being a lot less in a short period of time.

Apple Hospitality REIT (APLE)

Dividend Yield: 6.2%

Apple Hospitality REIT (APLE) is a REIT whose properties include 224 hotels in 87 markets across 37 states. And as is usual in the hotel REIT world, Apple doesn’t just serve one hotelier—118 of its hotels carry a Hilton (HLT) brand, 101 are Marriotts (MAR) and five sport the Hyatt (H) brand.

APLE’s focus on select-service hotels is ideal given their high margins, and it has access to not just cities but high-end suburbs, which is a nice diversifier. Its broader industry is trickier. An economic slowdown could affect hotels (and thus hotel REITs like Apple Hospitality), and high interest rates can also weigh heavily on the cost of capital.

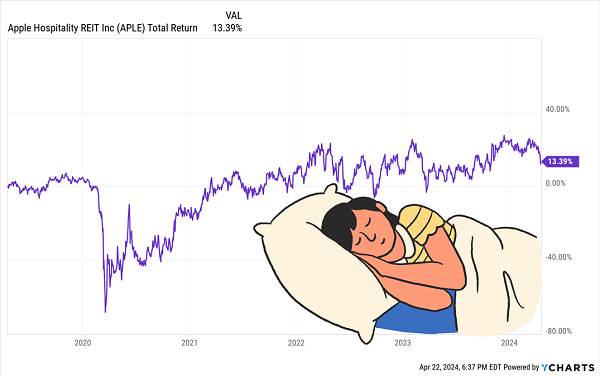

Those headwinds are pretty evident in APLE shares, which have been stuck in neutral ever since it reclaimed its pre-COVID highs in mid-2021.

APLE Has Been Hitting the Snooze Button for Years

When I last checked in on APLE last October, I was looking toward its next dividend announcement for some sort of sign it might be emerging from its funk. It didn’t—Apple’s payout, while well-covered, is where it has been since 2022. And so far in 2024, the REIT is suffering from soft RevPAR (revenue per available room) trends like many of its competitors.

Apple is decently priced at less than 10 times funds from operations (FFO) estimates, and the 6%-plus yield is much better than the sector norm. It has a well-positioned portfolio for growth, given the right economic circumstances, and insider ownership is high. It’s interesting in a bubble, at least, but it could stand for at least a little Fed cooperation.

Realty Income (O)

Dividend Yield: 5.8%

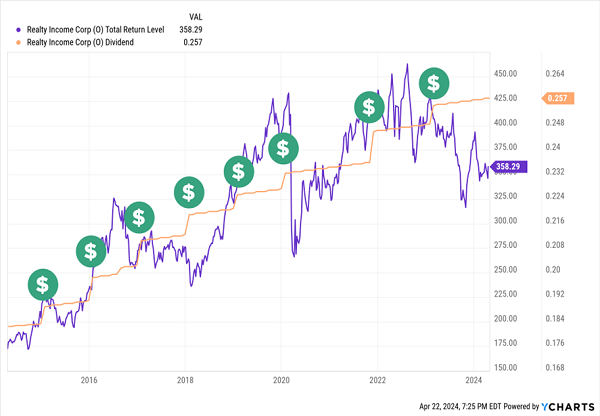

Realty Income (O) is one of the biggest REITs you’ll find, and long considered a standard-bearer for quality among net-lease real estate firms. The company currently claims nearly 15,500 commercial real estate properties rented out to 1,326 clients in 86 industries—not just here in the U.S., but increasingly in Europe.

Some of that scale has come through the individual and small deals common among REITs. But Realty Income has been highly active in large-scale acquisitions over the past few years, buying VEREIT in 2021, a 151-property purchase from CIM Real Estate Finance Trust in 2023, and closing on its merger with Spirit Realty Capital earlier this year.

Indeed, Realty Income has become so big that it’s having to expand upon its core business to keep scaling up. It’s now up to more than 450 assets in Europe, and it’s entering other property types including gaming sites and data centers.

But the only real growth investors have seen in the past couple years has been in its monthly dividend, which has improved for 106 consecutive quarters.

Will the Dividend Magnet Pull Realty Income Higher Again?

Realty Income expects 4.3% adjusted funds from operations (AFFO) growth in 2024, which, if the guidance is met, would be near the top of the industry. So the seeds for growth are there. But we wouldn’t exactly be buying at bargain prices, with shares going for roughly 13 times AFFO estimates currently.

AGNC Investment Corp. (AGNC)

Dividend Yield: 15.6%

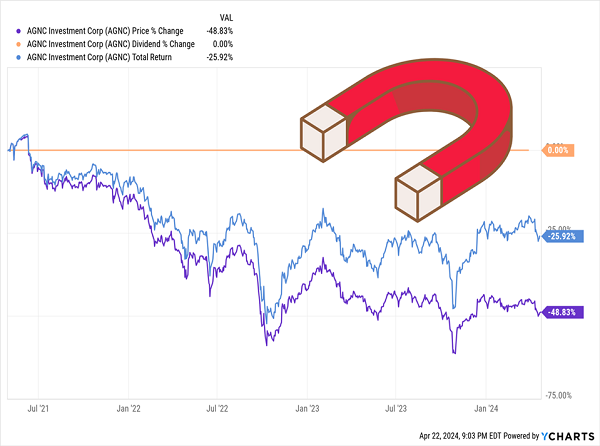

AGNC Investment Corp. (AGNC) is another blue-chip REIT, but one that deals in the mortgage space. At $6.4 billion in market cap, it’s second only to Annaly Capital Management (NLY)—a true juggernaut in this extremely high-yield corner of the real estate space.

Too bad that doesn’t count for much these days.

No Dividend Growth, No Dividend Magnet

AGNC uses heavy leverage to deal in agency residential mortgage-backed securities (MBSs). Of course, the business in general involves heavy leverage—its current leverage of 7.1x is actually low compared to an 8.2x historical average. But who can blame it? This has been a terrible time to deal in MBSes.

The business goes like this: mREITs buy mortgage loans and collect the interest. They make money by borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are higher, which they usually are).

Thus, the past few years of rising and high rates have been miserable for mREITs. And while they’ve been dying for respite from the Federal Reserve, that relief keeps getting pushed back as persistent inflation keeps staying Jerome Powell’s hand.

Mortgage REITs are largely a waiting game for now. Spreads should tighten if the Fed finally starts easing, which should provide some lift under mREITs in general, and better operators like AGNC in specific. Action could be rocky until then, though, and while the dividend seems reasonably covered for now, investors still might face anxiety over a payout reduction just given the company’s history.

Main Street Capital (MAIN)

Dividend Yield: 6.0%*

Main Street Capital (MAIN) is another best-in-class name, this time in the business development company space. It provides debt and equity capital solutions to lower-middle-market companies, and debt financing (primarily floating-rate first lien senior secured debt) to middle-market firms.

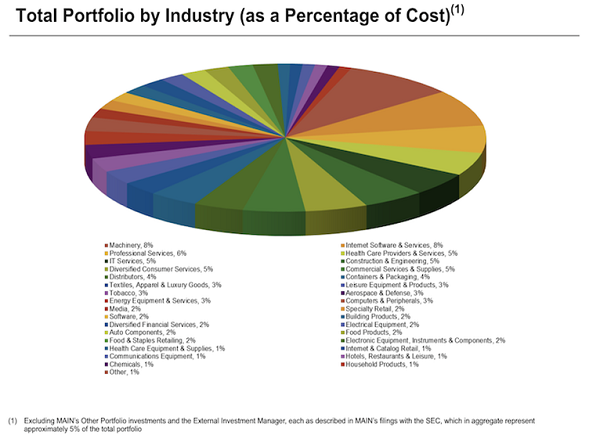

MAIN’s typical target company generates annual revenues of between $10 million and $150 million, and roughly $3 million to $20 million in earnings before interest, taxes, depreciation and amortization (EBITDA). Currently, its portfolio is made up of 190 companies, with the largest one representing less than 4% of total investment income.

Source: Main Street Capital Q4 2023 Presentation

Main Street pays monthly dividends that currently yield 6%, but it also uses special dividends pretty commonly. Add in its special payouts from the trailing 12 months, and we get an extra 1.2 points for a total yield north of 7%.

Operationally, this is a king among BDCs. Its Q4 2023 report showed better-than-expected net investment income (NII) and declining leverage and non-accruals. And its preliminary Q1 2024 results provide a net asset value (NAV) estimate of $29.51 to $29.57 per share, which would represent 1.1% to 1.3% quarter-over-quarter growth.

And MAIN Shares Have Responded by Taking Off

There’s just one problem: MAIN has gone from being wildly expensive to laughably expensive.

Back in October, Main Street’s stock traded at a 45% premium to NAV. Based on the company’s own estimates for Q1, shares now trade at a 63% premium.

MAIN is perpetually overpriced, sure, but this is excessive even by its own lofty standards. And even top-flight operators like Main Street can’t defy valuational gravity forever. But while it’s too rich to touch, I wouldn’t bet against MAIN, either.

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 10%

Back here on Planet Earth, PennantPark Floating Rate Capital (PFLT) isn’t exactly a steal, either, trading at just a hair over NAV. But it’s another good BDC operator trading at a relative value compared to the industry—and it’s sporting a double-digit yield—so it’s worth a quick peek.

PFLT primarily invests in companies owned by established middle market private equity sponsors that typically support their portfolio companies. Portfolio companies typically generate $10 million to $50 million in annual EBITDA. The portfolio currently represents 141 companies spanning 45 industries.

The company’s recent preliminary Q1 results show strong net growth and a nearly 2% improvement in NAV. While it did add a new loan to non-accrual, non-accruals still account for less than 1% of the portfolio. And the company started the year off with high deal activity in what’s normally a quiet quarter.

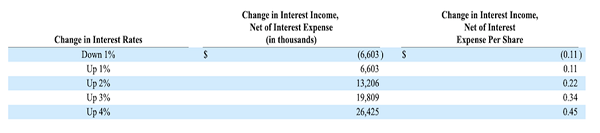

One point of serious concern, though, is the debt the company deals in. PFLT largely works with first lien senior secured debt (86%), with virtually all of the remaining 14% in preferred and common equity. That’s not a problem—but the fact that 100% of the portfolio is floating-rate in nature is. That makes PFLT considerably rate-sensitive; here’s what to expect should the Fed finally start throttling back on its benchmark rate:

Source: PennantPark Floating Rate Capital Q4 2023 10-Q

Of particular concern would be a rapid pullback in rates, which could trigger not only selling in PennantPark shares, but a potential shave to what has historically been a largely resilient dividend.

Earn a Reliable 8%+ in Retirement—Paid MONTHLY

Frankly, I don’t want to sit at my desk and recalculate how Fed rate cuts could cut into my monthly retirement income.

And I don’t think you do, either.

We need reliability in our post-career years. We need regular checks to supplement Social Security and keep us housed, fed, and comfortable —everything we’ve earned after a lifetime of work.

That’s why I have no interest in fragile or sensitive payouts, and why I certainly have no interest in overpaying for those stocks.

That’s also why I prefer the relative safety of the boring, high-yielding blue chips in my “8%+ Monthly Payer Portfolio.”

Yes. A high level of yield is a given here.

But it’s more than high yield. It’s high yield generated by steady-Eddie holdings with the potential to deliver meaningful price upside, too.

We don’t need to grab the Pepto every time the S&P gets the jitters.

We don’t need to stress about nest-egg shrinkage in our 60s, 70s, 80s, and beyond, either. Because unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

If you put this portfolio to work with a mere $500,000—less than half of what most financial gurus insist you need to retire—you’ll generate a nearly $40,000 annual income stream.

That’s $3,330 every month in regular income checks!

Don’t wait any longer to whip your retirement into shape and lock down these core income holdings. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments