Although some tariff hikes have been paused, a recession is still very much in play.

Just a few days ago, I wrote that “this is the time to recession-proof our retirement holdings.” And why not? GDP estimates have tanked. So has consumer sentiment.

Goldman Sachs made headlines for raising its probability of recession (from 20% to 35%). Fine, but equity analysts often get caught up in crowds.

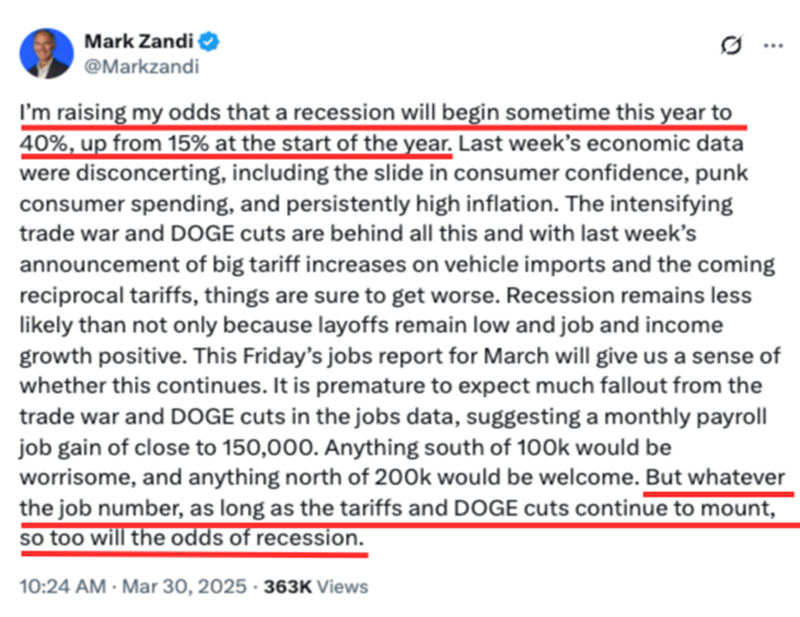

What was more striking was hearing a similar message from the debt watchers. Consider this post from Mark Zandi, Moody’s Analytics’ chief economist:

In my previous post, I showed readers how to recession-proof their portfolio with municipal debt.… Read more

Recent Comments