One of the best ways to grab a dividend payer set to surge is a strategy you never hear about anymore: Pick up shares of a conglomerate.

I know, I know. The word brings to mind “old school” companies like 3M (MMM)—which we discussed a couple weeks ago—and Honeywell International (HON).

The deal on these companies is that they’re basically a collection of businesses that often have little overlap. They’re hated by Wall Street because they’re just too much work for the suits to value!

That’s great for us because these firms often have the most value waiting to be unlocked—especially if you buy as they tighten their focus on a specific industry.

I was thinking about conglomerates the other day when I was researching shares of Danaher Corporation (DHR), which yield just 0.4%—a number that masks the fact that the payout has shot 170% higher than it was just a decade ago.

We’re talking a steady staircase of dividend raises here with, as we’ll see, more hikes likely.

Hands up if you know what Danaher does. (No worries if you don’t—plenty of investment pros don’t, either.)

The nutshell version: It’s a conglomerate that traces its roots to the 1960s. It used to own businesses making everything from automotive tools to water-testing gear. These days, it’s shedding those operations—and buying others—to focus on healthcare.

As Danaher continues its transition, it’ll likely get on more analysts’ radar. As it does, more will likely turn bullish on the stock.

A Well-Timed Healthcare Expansion

It’s no secret that the US population is getting old fast: According to a January report from the Alliance of Lifetime Income, 2024 will see 11,000 Americans turn 65 every day.

Big-pharma stocks like Johnson & Johnson (JNJ) are the logical buys here. But if we’re talking drug makers, we only want those with lots of treatments in the pipeline, since, on average, a new one takes 10 to 15 years to develop.

Moreover, according to a 2018 MIT study, just 14% of drugs in clinical trials end up getting the green light from the FDA. In other words, a new drug can flunk out any time before then, taking all the company’s R&D cash with it.

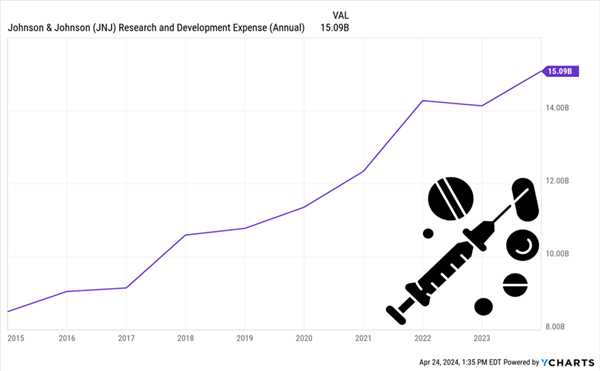

And we’re talking a lot of cash here: Consider that JNJ spent $15 billion on R&D alone last year—a total that continues to march steadily higher, with no cap in sight:

Danaher Looks to Help Drug Firms Cut This Ever-Growing Cost

So, as you can imagine, anything that could shorten that timeline, and reduce the risk, would be in high demand.

A “Pick-and-Shovel” Play

That’s just what Danaher, under the leadership of current CEO Rainer M. Blair, has done. Blair probably wouldn’t use the same words I do, but he’s basically turned Danaher into a “pick-and-shovel play” on the drug biz.

The idea goes back to the California gold rush, where it was the businesses that sold the picks, shovels, booze and food the miners needed—not the gold-panners themselves—who made the real cash.

So it is with Danaher, which peddles the gear that makes the industry run. The company is set up on three lines: Biotech makes essential equipment like bioreactors, which create an ideal environment for chemical and biological reactions to happen.

Life Sciences focuses on cutting drug development, with the goal of doing so by 50%. Right now, it aims to tap the power of AI through its CellXpress.ai automated cell-culture system, which, as the name suggests, grows cells necessary for new treatments.

Finally, Diagnostics makes tests that help doctors deliver more accurate diagnoses.

The key takeaway here is that Danaher doesn’t have to worry about the long timelines and high costs of developing drugs—it’s too busy profiting from them!

A Savvy Buyer—and Seller, Too

The company made two recent moves to cement its place in healthcare.

In September of last year, it spun off Veralto (VLTO), whose products test food, water and pharmaceuticals. Then, in December 2023, it closed its $5.7-billion acquisition of UK-based Abcam, maker of antibodies, proteins and cellular-imaging systems.

Danaher has acquisitions, quite literally, in its blood. It started out in the 1960s as a real estate investment trust (REIT) focusing on seniors’ housing.

Then, in 1984, brothers Steven and Mitchell Rales took over, switched the name to Danaher and went on a buying spree, mostly in the manufacturing business.

Since then it’s bought (and sold) businesses ranging from Matco Tools (automotive) to ChemTreat (water-treatment systems) and X-rite (color monitoring). All told, the last decade of acquisitions account for 50% of Danaher’s current revenue.

In other words, this management team knows when they see a company that would add value—and they know how to avoid the risks.

In any case, Danaher has the balance sheet to manage its risk, keep its acquisition machine running and protect its payout: Its long-term debt is $12.5 billion, net of cash on hand, easily manageable for a firm its size (its market cap is $184 billion).

Of Picks, Shovels and … Magnets?

Let’s talk a bit more about that dividend, which, as I said earlier, is all about payout growth rather than current yield. We love dividends that soar because they tend to pull their shares up with them—a phenomenon I call the “Dividend Magnet”.

You can see that in action with Danaher over the last five years:

Danaher’s Dividend Magnet Goes to Work

As you can see here, Danaher’s stock has not only tracked its dividend higher, it’s run ahead of its payout growth in the last five years. We normally like to see a stock fall behind its payout, so we can ride along as it plays catch-up.

But this trend isn’t surprising given that the stock started to really pull ahead as Danaher focused more on medical devices during the pandemic.

In other words, it’s that value unlock I mentioned earlier in action.

So where does that leave us? The company’s latest earnings report, delivered last week, showed smaller earnings and revenue declines than expected, pointing to a rebound in biotech and an easing of overhangs on the sector, including a glut in demand for COVID-19 tests.

Finally, as the dust settles on its latest moves, management will have a more streamlined—and healthcare-driven—portfolio of businesses to focus on. That will likely be music to the ears of Wall Street analysts, and mainstream dividend investors, too.

My System Produced Fast 57% and 148% Gains. Here Are Its Next 5 Winners

Few people stop to think about the connection between dividend growth and share-price growth. But a growing payout is the No. 1 driver of share price gains!

By tracing that connection, I’ve uncovered gain after gain for my readers.

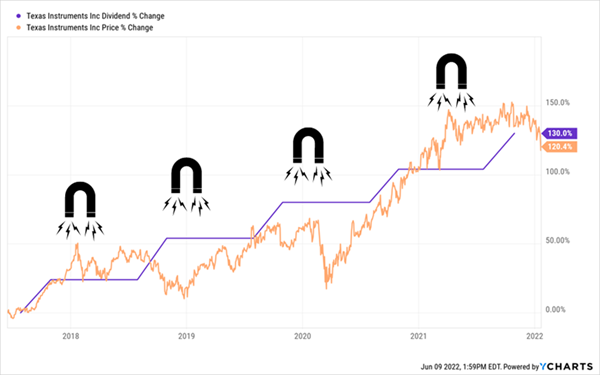

Including Texas Instruments (TXN), whose dividend marched 130% higher during our holding period, driving a 120% jump in the share price!

We Rode TXN’s Dividend Magnet to a Massive Gain …

Add dividends and those share price gains together and you get a 148% total return!

Or American Tower (AMT), whose payout rose every quarter in the little more than three years we owned it, from November 2018 to March 2022, ultimately soaring 65%.

The share price? It soared 54%, resulting in a 57% total return!

… And American Tower’s, Too

Now I’ve zeroed in on my NEXT five Dividend Magnet winners, and I can’t wait to show them to you.

Recent Comments