One of the market’s most secure, steady sources of generous yield is going through a rare turbulent moment. But these 7% to 8% yields—paid monthly, no less!—are selling at discounted prices we only see once every five years or so.

Is it time for us contrarians to consider “backing up the truck” to load up on these monthly dividend machines?

Why “Preferred” Dividends are This Cheap

“Preferred” stocks are stock-bond hybrids that rarely make Wall Street’s highlight reels. We like it that way, because these funds pay.

These underappreciated secrets don’t usually suffer this bad, either.

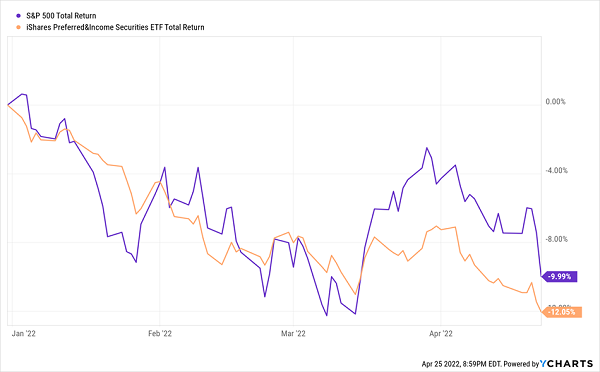

You Rarely See Preferreds Get Clobbered This Bad

The reason preferreds are usually so steady is that they simply collect income.… Read more

Recent Comments