If you’ve been following the AI space lately (and honestly, who hasn’t?), you’ve probably seen stories about tech investors feeling a bit shortchanged on the profits they’re getting.

That’s actually good news for the rest of us—a sign the market is maturing and ripe to be tapped for income.

Specialists Often Miss the Bigger Picture

Experts make this mistake all the time. There are a few reasons for this, but probably the biggest is overreach: You can be a wizard at technology, you can even be a genius at investing in technology, but you can still be wrong if growth happens differently than you expect.

A classic example occurred in the 1930s, when many investors rightly saw cars as the future of transportation. Those who placed their faith in Henry Ford became rich. Those who went with Preston Tucker, however … did not. That’s despite the fact that Tucker produced some beautiful machines.

History never repeats, but it does rhyme, as the saying goes, so today the story is a bit different. We’re seeing some AI firms lose to others, just as Tucker lost to Ford. But that’s not really what AI’s major investors are worried about. They worry the real AI gains are going somewhere else entirely.

Imagine you own a company, and you need 100 reports written. Each report takes eight hours, so 100 reports require 100 workdays to produce. Now you give your employees an AI tool that cuts the production time to seven hours. You now have one hour per report for those employees to use for something else (or you could employ fewer people). Either way, the AI tool has increased your profit margin.

So the AI story is really about gains across the entire economy, not just the tech sector.

This is a lot different than what we saw from the last generation of tech advancements. Then, companies like Alphabet (GOOGL), Amazon.com (AMZN), Apple (AAPL) and Meta Platforms (META) found ways to essentially tax each transaction a firm made, whether it was on products sold through ads, like on Alphabet and Facebook, or items selling directly through a third-party marketplace, as occurs through Amazon or the Apple App Store.

AI tools, on the other hand, are more supportive—more like an administrative assistant or even an intern doing a lot of busy work. They simply cannot command as much of a premium of the client’s revenue as, say, Apple can command from app developers selling their wares on its app store.

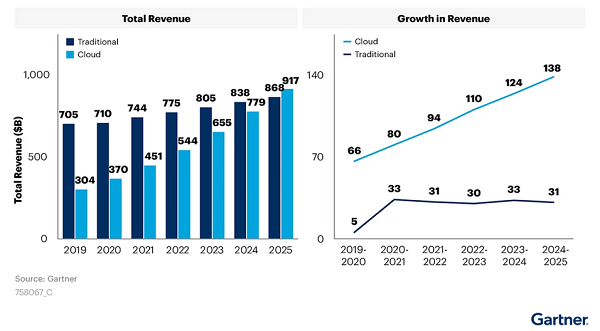

Of course, none of this is really news. Market-research firms like Gartner have been pointing this out for a while, noting that the rate of demand for cloud computing, for example, was growing before generative AI tools came out. And while AI has helped sustain that trend of rising growth (the chart on the right above), that pattern was already underway in the 2010s and hasn’t really changed.

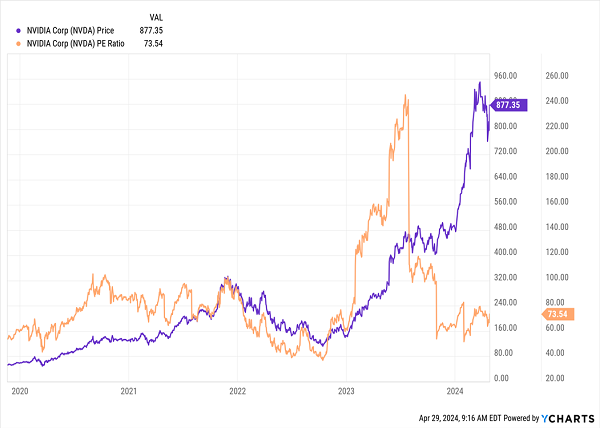

Now, if you own a stock like leading AI chipmaker NVIDIA (NVDA), you might be a little concerned. After all, competition among chipmakers is heating up, and the stock has more than doubled in a year. And reading both what I’ve written above and the headlines about disappointed AI investors, you may think AI stocks are ripe to pull back.

But consider this chart.

How Much Risk Is Here, Really?

The purple line above shows the change in NVIDIA’s stock price. What most investors miss is the orange line, which represents the stock’s price-to-earnings (P/E) ratio. At 73.5, it seems expensive.

But NVIDIA’s P/E has averaged 56 in the last decade, which is also considered high. Investors who were deterred by that have missed out on serious gains.

Of course, this doesn’t make NVIDIA a no-brainer buy. We still have the risk of competition limiting its growth, so if other firms make more successful AI chips, then yes, NVIDIA would be a sell.

But remember that the efficiencies AI generates are also highly profitable, and they’re flowing to the larger economy. If NVIDIA makes chips for the next generation of AI tools, great, the greater economy will benefit (with the exception of NVIDIA’s competitors!). If another company makes those chips, the economy still benefits (except NVIDIA).

This is why we look to a diversified approach for AI investing, “cherry-picking” funds—closed-end funds (CEFs), to be specific—that give us exposure to both strong tech stocks and those from across the economy that are utilizing AI.

That way we benefit from whichever firm wins the race to make the best AI chips. But more important, we’re grabbing a slice of the efficiency gains that countless firms that use AI are realizing.

A Diversified Pick for AI Gains, 6% Dividends

Consider, for example, a fund like the Gabelli Dividend & Income Trust (GDV), whose top-10 holdings include Microsoft and Alphabet, which gives us some nice “direct” AI exposure.

But then we get loads of “indirect” AI exposure, too, through firms like industrial conglomerate Honeywell International (HON), pharmaceutical firm Eli Lilly & Co. (LLY), Mastercard (MA) and American Express (AXP).

Moreover, GDV pays a 6% dividend and trades at a 17% discount to net asset value (NAV, or the value of its underlying portfolio). That means we don’t have to worry about overpaying for any of its holdings—we’re essentially buying in for 83 cents on the dollar!

GDV’s 6% Payout Is Chump Change. These 7.8% Dividends Are the Real Deal.

GDV is a good way to profit as AI ignites profits across the US economy. But its 6% dividend is, frankly, a little skimpy as CEFs go.

I know that might sound a bit greedy, considering that many tech stocks pay 0% dividends! But big dividends are a given when we invest in CEFs—like the 7.8% average payouts we can pocket from my top 4 AI CEFs to buy right now.

These funds invest in AI developers, yes, but also get us plenty of exposure to companies that are boosting their efficiency (and ergo their profits!) through AI, too.

That’s exactly in line with our “dividends-first” AI-investing plan.

Plus, these 4 funds are terrific bargains, too! But that won’t last as AI’s efficiency gains start to show up in more corporate earnings reports. The time to buy is now.

Recent Comments