“Buy bonds!” – Contrarian Outlook, 2H 2022

Two years later, the herd finally hopped on our fixed-income bandwagon…

“Buy bonds!” – Wall Street, 2H 2024

Yes, it is satisfying to be right. But it also makes me nervous that mainstream (“vanilla”) investors now agree with us.

If you bought with us, you are sitting pretty. On the other hand, if you are trying to put new money to work today, this is a challenging time. I don’t like buying high and I especially avoid purchasing popular names.

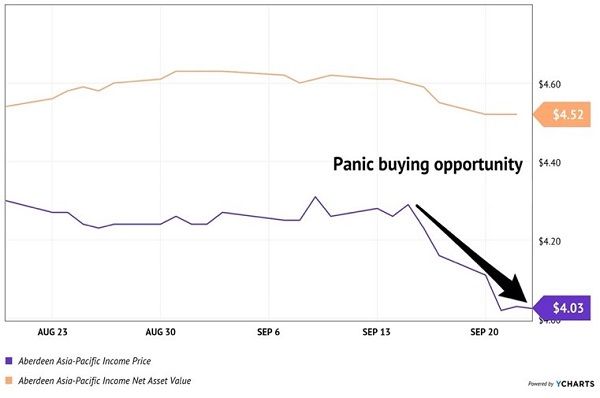

Case in point, my favorite PIMCO products in the closed-end fund (CEF) space.… Read more

Recent Comments