There are three very clear signs the stock-market bull will keep stampeding. Let’s dive into them, then talk about two discounted funds set to ride those gains (and pay us rich dividends up to 11.4% in the process).

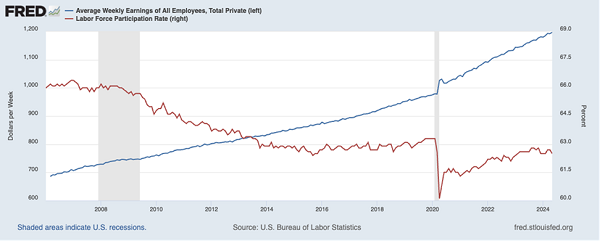

Bullish Signal #1: The US Worker is Strong

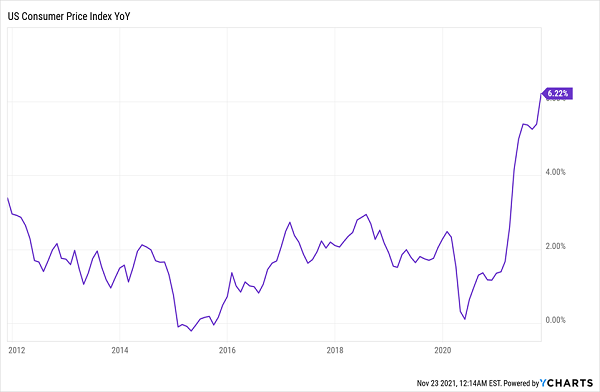

There’s a lot of pessimism about the US economy out there, even though it’s doing well. We’ve discussed why this is before—it’s ultimately due to the media getting more pessimistic—but this chart proves the point.

Since the Federal Reserve started tracking workers’ average weekly earnings in 2006, they’ve risen at a steady rate of about 2.6% annualized from then to 2020.… Read more

Recent Comments