Some are fast. Some are slow.

Some are high. Some are low.

None of them is like another.

Don’t ask us why, go ask your mother.

– Dr. Seuss

Here at Contrarian Outlook, we prefer slow—as in slow-moving share prices. And high—as in high yields.

As to why, well, I need to address why other (less sophisticated) investing websites have bad information regarding a very good fund. So bad, in fact, that vanilla investors are scared to buy this perfectly safe 8.4% dividend!

Before I send you to ask your mother, I’ll explain why our website is right and other websites are wrong.

Our overall mission here, as always, is to retire on dividends and leave our capital intact. To accomplish this, we’re looking for safe meaningful yields. I’m talking 6%, 7% and even 8% or better. Such as the elite 8.4% dividend we so often wax eloquently about from Cohen & Steers Infrastructure Fund (UTF).

UTF is a “retirement maker.” It is my go-to utility fund—the ticker I type when I believe utilities are about to rally. I prefer UTF over individual stocks because, as a closed-end fund (CEF), UTF’s mission in life is to dish us a generous dividend.

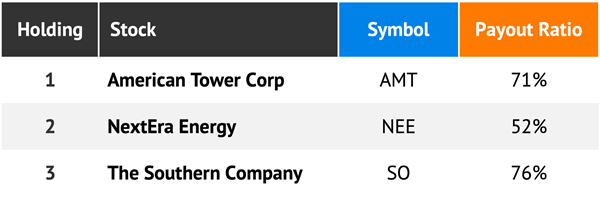

Portfolio manager Benjamin Morton handpicks a collection of 229 infrastructure and utility stocks. We’re talking about cell phone tower landlord American Tower Corporation (AMT), high-growth utility NextEra Energy (NEE) and “OG” utility The Southern Company (SO).

Morton’s mission? Fund the 8.4% dividend with a mixture of payouts and price gains. Dish us 15.5 cents monthly. Rinse and repeat.

He’s good at what he does. We’ve held UTF twice in our Contrarian Income Report portfolio and have enjoyed 95% and 19% total returns (including the monthly payouts).

CEFs are funny. As favorites of individual (“retail”) investors, they are subject to panics, where they trade below their net asset values (NAVs). As well as to bouts of FOMO, when they drift above their fair values!

As I write, UTF trades at a 1% premium to its NAV. Which means investors are paying $1.01 for a dollar in assets. Not egregious, but I’d prefer to buy it for 95 cents on the dollar—like we did last June.

Since then, shares have returned a neat 9%, mostly in dividends. Some readers, however, sadly didn’t buy. They were paralyzed by this gem from Yahoo! Finance:

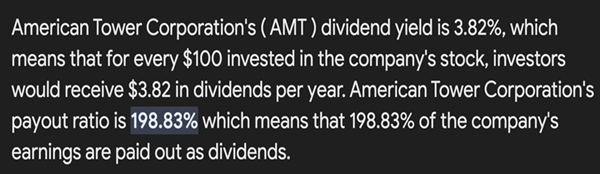

Pro Tip: UTF’s Payout Ratio is Not 489%

The footnote should say “just kidding.” Seriously. In reality, Yahoo! Cites Morningstar as the original source of this information.

Which is why, as I was explaining to my nine-year-old, plagiarism is pointless. Lazy, sure, but it’s worse than that. Why copy something word-for-word when it could be wrong?

Better to use our own brains. Let’s make my daughter proud (which is, I’ll admit, tough to do) and revisit UTF’s top three holdings and their actual payout ratios:

Off the cuff, AMT is a tricky one. Most websites report its payout ratio in the 200% range—even those that Google cites as authorities!

If true, this would be problematic. We don’t like companies that pay dividends that are double their earnings. If true for AMT, UTF’s ownership of the stock would be a problem.

Fortunately, once again, the Internet is wrong.

What is an acceptable payout ratio for AMT? And what is its actual payout ratio—the dividends it is paying with respect to its real cash flow?

Let’s do this calculation the right way. (Take notes, Internet!) AMT is a REIT. Adjustable funds from operations (AFFO) per share is the metric we want, and AFFO breaks the internet’s calculator. Cookie cutter data services treat it incorrectly.

So, being contrarians and very much not cookie cutter, we do the “unthinkable” and open AMT’s investor literature. Here, we see that the company earned $2.29 per share in AFFO in its most recent quarter:

Which means AMT’s most recent quarterly dividend of $1.62 works out to a 71% payout ratio. That is great! Here’s why.

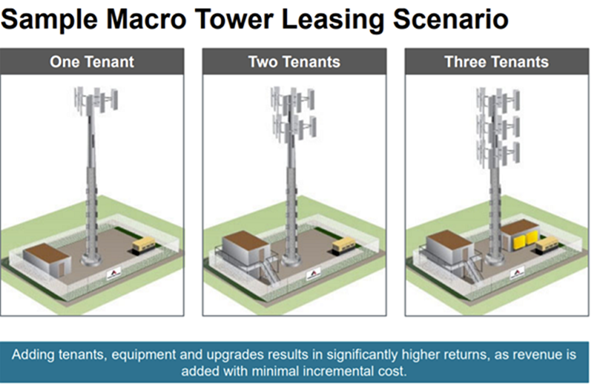

AMT owns vertical towers and leases space on them to telecom providers. Multiple tenants can install their own communication equipment on the towers to help connect customers. Typical tenants are all the big names: Verizon, AT&T, T-Mobile, DISH—as well as many other medium and even smaller businesses offering wireless communications.

The returns on investment for one tower expand with more tenants. The cost is in the construction; it costs next to nothing to add them. So, while one tenant isn’t that profitable for AMT, bringing only a 3% annual return on investment (ROI), each new tower tenant boosts it. With three tenants, AMT earns a 24% ROI!

Oh, those poor vanilla income investors! They are being scared from perfectly good income stocks and funds by widely reported dividend information that is wrong! So much for checks and balances on the Information Superhighway.

And if you think AI tools will improve upon this, well, where do you think they scrape their quick answers from?

We’ll keep doing our own research here at Contrarian Outlook, thank you very much. And oh by the way, while we are thinking originally, let me leave you with a parting thought that is, of course, a bit contrarian.

UTF is cheaper than it seems at a 1% premium today. The shares it owns have pulled back sharply in recent weeks because many high-paying utilities trade opposite interest rates.

If you believe, as I do, that rates are closer to a top than not here, then UTF is about to look quite cheap. Better to buy now and lock in this 8.4% dividend while we can.

It’s important for us to debunk the shade being thrown at UTF, which is a near-perfect retirement investment.

See how doable it is to secure a safe 8.4% dividend? If you like UTF, well, I have some more perfect income investments that are right up your alley.

Recent Comments