Don’t believe anyone who tells you there’s such a thing as a safe investment. Truth is, every asset—from Treasuries to houses to dividend stocks—involves risk.

The “safest” investment, according to the Financial Industry Regulatory Authority (FINRA), is a short-term US Treasury bill. You lend the government $100, say, and you’ll get $105.17 back in a year. Not bad.

But there are some caveats:

- Short-term Treasury rates fluctuate, and the Federal Reserve has said they’ll try to get them lower later this year.

- In a truly apocalyptic disaster, you might find that the Federal Reserve doesn’t pay your money back. In fact, you might find that money itself is worthless.

That second point might sound silly, but I’m pushing the boundary here to highlight the point that nothing in life is risk-free. When investors talk about “risk-free returns,” like with Treasuries, they’re assuming tomorrow will look like today. But it may not.

For this reason, we have to accept that no matter where we put our money, there’s a chance of losing some.

Inflation Risk Is Far More Dangerous Than People Think (Especially Now)

What about cash, supposedly the ultimate safe investment? That’s even riskier. Due to inflation, if you saved $100 in cash five years ago, it’s worth $78.80 now.

The reason for this is that our current 3.5% inflation rate devalues money by that much from just a year ago, but of course inflation ate into money’s value the year before that, and before that, and before that … you get the idea.

In other words, not even cash is safe.

I’m not writing this to worry you! Instead, look at it this way: Your wealth is yours to master and turn into more wealth. The key is to embrace risk and put a bit more focus on the rewards investors get for taking it on.

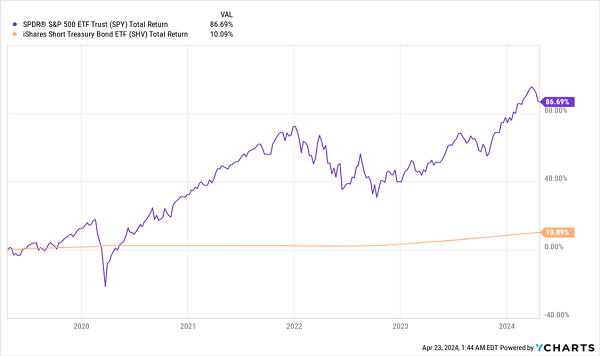

Consider, for example, how someone who bought short-term US Treasuries five years ago—shown through the iShares Short Treasury Bond ETF (SHV) in orange below—would have done compared to an investor who bought the SPDR S&P 500 ETF Trust (SPY), the benchmark S&P 500 index fund (in purple).

“Low” Risk = Low Returns

That period included a pandemic, an inflation spike and all kinds of other pandemonium. Even so, stocks crushed short-term Treasuries. It just shows that letting fear rule too many of our investing decisions is more detrimental than we realize.

Sounds reasonable, you might be thinking, but surely there’s a way to ease stock volatility without sacrificing much in returns and ensuring my money is there when I need it.

This concern is perhaps the most common one among individual investors. And (of course!) Wall Street has an answer: the target-date fund.

Here’s how it works: Let’s say we want our money available in 20 years, so we buy a fund with a target date 20 years out, put our money in, keep investing and ride the wave.

It helps to show this through a real-world example, so let’s put together a little scenario.

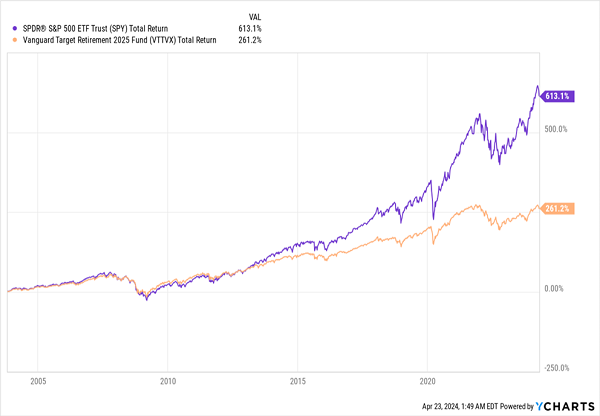

Let’s say an investor back in 2003 wanted to retire in a bit more than 20 years, so they bought the (then) newly launched Vanguard Target Retirement 2025 Fund (VTTVX).

Our investor is drawn by the fund’s set-it-and-forget-it nature. They also find VTTX appealing because over time it will lower their exposure to stocks and shift to bonds to increase safety and ensure their money is there when they retire. Plus the fund is cheap, with a fee of just 0.08% of assets.

Sounds great, right? Well, not so fast.

Good Intentions Lead to Mediocre Returns

With VTTVX (in orange above), our investor’s current value would be less than half of what it would’ve been if they’d invested in the stock market. A $100,000 investment in VTTVX would now be around $261,200, while the S&P 500 index fund produces about $613,100.

In other words, fear cost them over $350,000—the cost of a house or a Lamborghini.

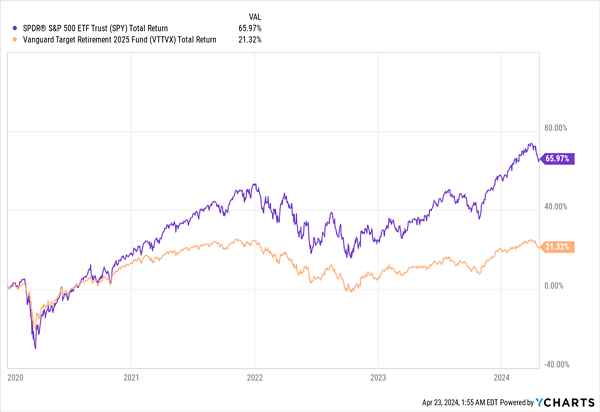

True, SPY’s dips have been worse than those of VTTVX, but this is an illusion. If we zoom in on times of stress, like 2020, we see that VTTVX’s strategy didn’t help much.

VTTVX’s Conservative Strategy Didn’t Save It During COVID …

VTTVX still fell 20% during the crash, which is better than 30% drop in the S&P 500. But the index also recovered faster. So VTTVX holders were spared the pain of losing an extra 10% of their gains, but they also suffered the pain of a slower recovery.

In fact, their recovery was never fully finished, as VTTVX has underperformed since the COVID crash.

… And It’s Still a Laggard Today

There’s still one issue here: liquidity.

In 2023, VTTVX paid a 4% dividend, while the average S&P 500 stock pays about 1.3%. So a lot of investors point to target funds as a great income option. Sure, you sacrifice profits, goes the thinking, but you have more cash flow as compensation.

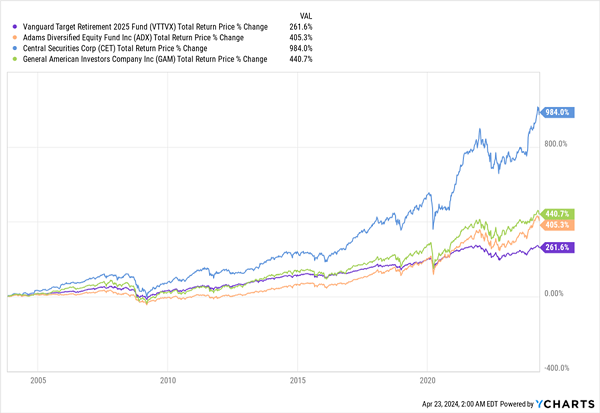

Not exactly. At least not when you compare VTTVX with the asset class every investor should be looking to for long-term gains and high dividends: closed-end funds (CEFs).

Below we see the total returns of VTTVX (at the bottom, in purple) versus those of three CEFs that focus on large cap stocks: the Adams Diversified Equity Fund (ADX), in orange, Central Securities Corporation (CET), in blue, and General American Investors Co. (GAM), in green.

As you can see, all three have crushed the target-date fund:

CEFs Outrun Target-Date Fund, With Much Bigger Dividends

CET, in particular, really took off, thanks to the magic of compounding stemming from the fact that it did much better than its peers during the Great Recession. From the start of 2008 to the start of 2015, CET gained 53.3%, while ADX and GAM returned around 35% each.

Consider also that these funds have paid out over 7% in dividends on average during this period, and you can see why target funds don’t make much sense. They offer less cash flow, lower returns and not much less risk.

The final word is that if you’re looking to grow your retirement savings, target funds may seem compelling, but their low-risk approach also means there’s a high chance of low returns, which, of course, nobody wants.

Yes, Income Investors Can Reap Huge Payouts From AI. Here’s How

Another big benefit of CEFs is that they can help us target many different parts of the economy, including real estate investment trusts (REITs), blue chip stocks (as we just saw), corporate bonds, preferred shares and more.

We can also use them to reap big dividends, and gains, from revolutionary megatrends like artificial intelligence (AI).

In fact, I’ve built you a simple four-CEF “mini-portfolio” that does just that. These four CEFs not only give you access to big-name AI plays like Microsoft (MSFT), but up-and-comers, too, as well as non-tech firms poised to reap the biggest gains as AI supercharges their operations.

The best part? These 4 AI-Powered funds are cheap—and between them they crank out a monstrous 7.8% average dividend!

Recent Comments