We just saw the first real signs that the “vibecession” is becoming something more—and this is our cue to pluck from our portfolios (or avoid adding!) three funds that are way into bubble territory. (Names and tickers below.)

Let’s start with that slowdown signal.

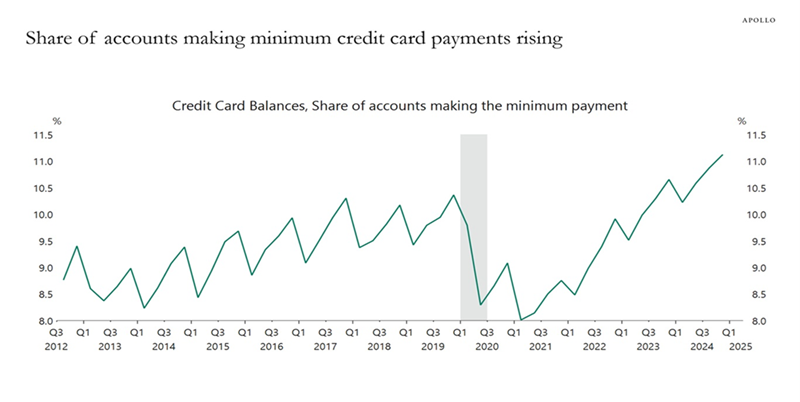

In this chart, from Apollo Global Management, we see that the total number of Americans who are only making the minimum payments on their credit cards is at its highest level in over a decade. This tells us that inflation and a slowdown in the job market are putting direct (and increasing) pressure on household budgets.

There are other signs, too.… Read more

Recent Comments