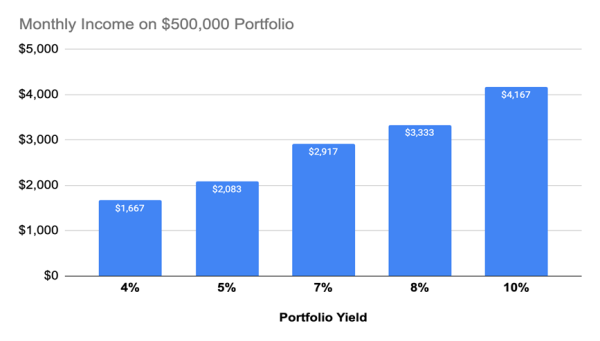

If there’s anything better than monthly dividends, well, we contrarians don’t want to know about it. Getting paid on the same schedule as our bills (monthly!), makes retirement planning easy.

We still need enough yield, though, to get rid (and stay rid) of our day jobs. Our pile of savings is what it is at this point, so we look to larger dividends to do the heavy lifting for us.

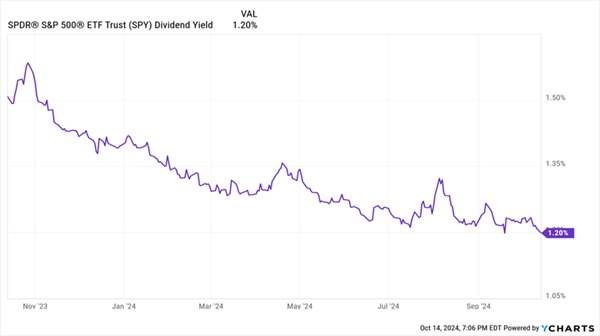

The S&P 500, needless to say, won’t cut it. First, the “SPY” pays quarterly—not often enough! Second, it pays 1.2%—not high enough!

“The Market” Is Paying Just Pennies

Even yield-focused funds’ yields are pretty lame right now.… Read more

Recent Comments