When I explain the appeal of closed-end funds (CEFs), I usually start with the big headline and throw a few bullets afterwards, kind of like this:

CEFs yield an average 8%, and many of those dividends are sustainable and growing.

- CEFs invest in a variety of reliable and popular assets, like stocks, bonds and real estate investment trusts (REITs).

- CEFs often trade at discounts to the value of their portfolios. This is known as the discount to net asset value (NAV), and it means we can buy stocks, bonds and real estate through CEFs for less than we’d pay on the open market.

- Many CEFs either meet or beat their benchmarks, with a number of them topping the S&P 500 over a decade or more.

And when you start to really dig into the CEF universe, you start to see even more opportunities. Take, for instance, the Cohen & Steers Quality Income Realty Fund (RQI), which mainly invests in REITs and yields 8.6%.

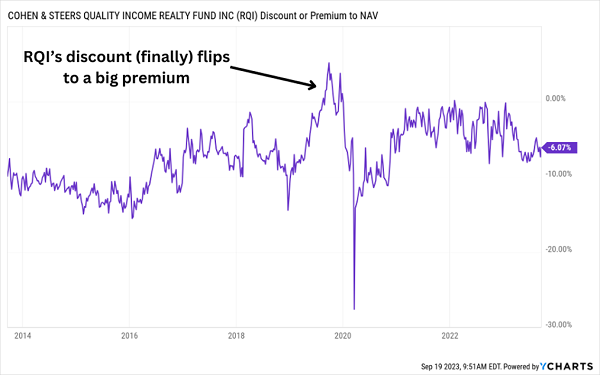

I’ve kept close tabs on RQI for years, and it stands out for the stability of its discount, which is around 6% now and usually floats around that level—except when it weirdly shot to a big premium back in 2019:

RQI’s Discount Takes a Strange Turn

This is a good example of how we can use CEF discounts to position ourselves for gains. I first spotlighted RQI’s value in a weekly article on our Contrarian Outlook website back in November 2017, thanks to its prudent use of leverage at a time when interest rates were going up (sound familiar?).

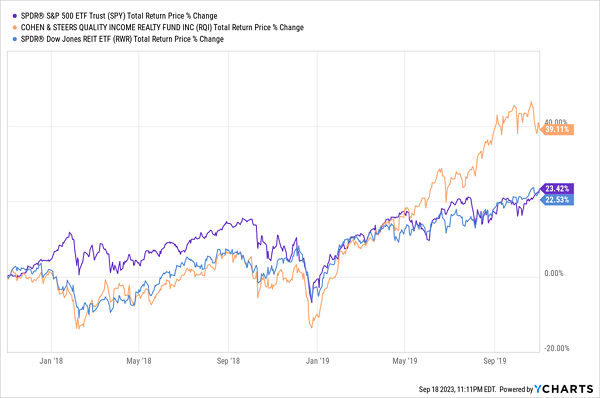

Over the next two years, its market price outran both the S&P 500, shown below by the performance of the SPDR S&P 500 ETF Trust (SPY)—in purple—and the REIT index, the SPDR Dow Jones REIT ETF (RWR)—in blue—a more appropriate benchmark, since RQI focuses on real estate.

RQI Beats Stocks and REITs

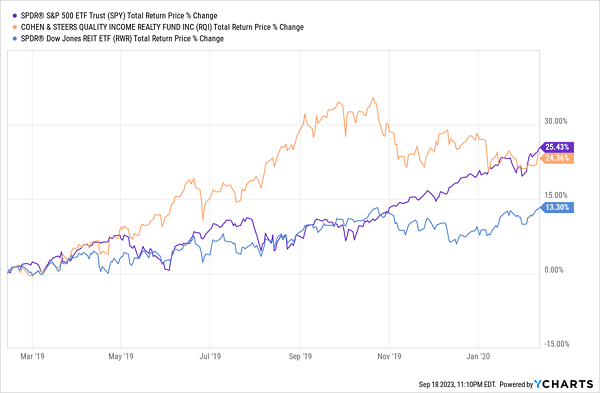

Of course, not all of those gains came at once. As you can see above, RQI really took off in the middle of 2019, right when its discount started to narrow. This is why I brought it to readers’ attention again in February of that year again pointing out its outperformance potential.

February 2019 is a good reference point for our example, because RQI’s discount eroded quickly thereafter, soaring to a premium as high as 5% in late September before falling back to its customary level of around 6% by early January 2020. You can see the corresponding rise and fall in the fund’s return, in orange below.

RQI’s Discount Drives Its Rise—and Fall

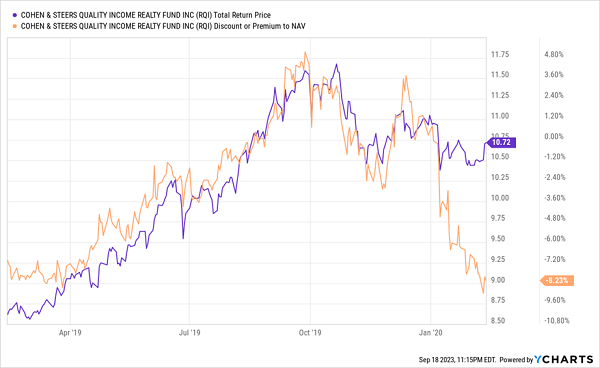

That long period of outperformance was a clear sell sign that really opened up in June and stayed open for a full seven months. Not only that, at the time the sell sign was made even clearer by the contrast between RQI’s market price–based return and its plunging discount, as you can see in this chart:

A Clear CEF Swing-Trade Indicator

RQI’s discount stays around 6% or 7% over the long term, but rising demand for REITs and real estate in 2019 (in response to the oversold market in 2018) was a huge opportunity.

But as more people cottoned on to this money-making inefficiency in the market, RQI’s discount morphed into that 5% premium—something that hadn’t happened since before the Great Recession of 2007 to 2009.

That highly unusual shift was an obvious sell sign, and it illustrates the power of CEF discounts in dictating our moves into and out of these funds.

This swing-trade opportunity with CEFs is true magic, because if you are wrong, you’re still getting paid the whole time. RQI was paying an 8% dividend in February 2019, and it yields 8.6% now, so even if you missed the sell signal, you were still collecting a huge income stream along the way.

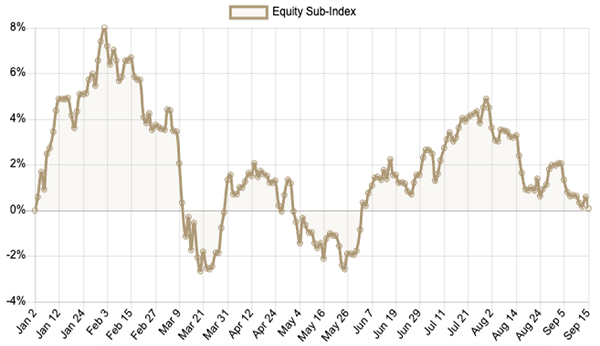

Similar opportunities exist across the CEF space now, especially among equity funds.

Equity CEFs Stall, Even as the S&P 500 Pops

Source: CEF Insider

As our CEF Insider Equity Sub-Index shows, equity CEFs (the majority of which hold S&P 500 stocks) are up just 0.1% year to date, while the S&P 500 is up 14.5%.

This makes no sense.

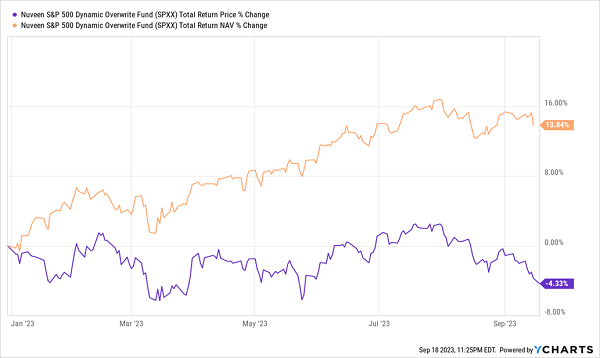

Perhaps one of the strangest examples of this disconnect is the Nuveen S&P Dynamic Overwrite Fund (SPXX), which has posted a strong return on a NAV basis this year, since the fund owns the entire S&P 500. But for some reason, CEF investors have been selling it off, which is why the fund’s market price is actually down year-to-date!

SPXX’s Portfolio Is Up, But Its Market Price Is Down

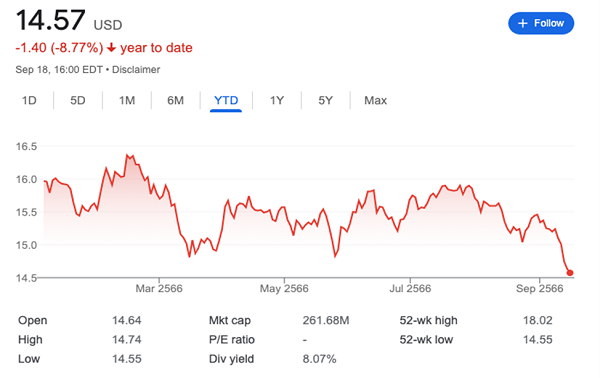

To drive this point home, let’s look at SPXX on Google Finance, which shows us the decline on a price-only basis (as opposed to total returns in the chart above). See how it’s down sharply year to date, even though it owns S&P 500 stocks and gets extra income by selling covered call options on its portfolio?

SPXX’s Strong Portfolio Performance Falls Flat With Investors

Source: Google Finance

The result is a 9% discount to NAV—on a fund that’s averaged a 1.9% premium over the past 52 weeks!

For contrarians who like to buy low, when others are eager to sell, a fund like SPXX is an appealing option. It has a strong portfolio, a sound strategy and an 8.1% dividend yield. It shouldn’t be down while its portfolio is going up in value!

This isn’t just happening with SPXX, by the way. Literally hundreds of CEFs are ripe for a swing trade like RQI was back in 2019: this is a market where still-wary (and therefore mostly sidelined) retail investors have handed us an opportunity to pick up cheap income. Don’t miss out on it.

Revealed: The 4 Best CEFs (Yielding 9.5%!) for This “Disconnected” Market

When I say there are plenty more CEFs out there trading at bizarre discounts, I’m not kidding. I’ve handpicked 4 sporting such deep discounts I expect 20%+ price gains out of them in the next 12 months.

Plus, they yield an outsized 9.5% on average!

Click here and I’ll tell you more about how I use CEF discounts to uncover gems in this comically overlooked corner of the market. I’ll also give you the opportunity to download a free Special Report naming these 4 undervalued 9.5% payers. Don’t miss it!

Recent Comments