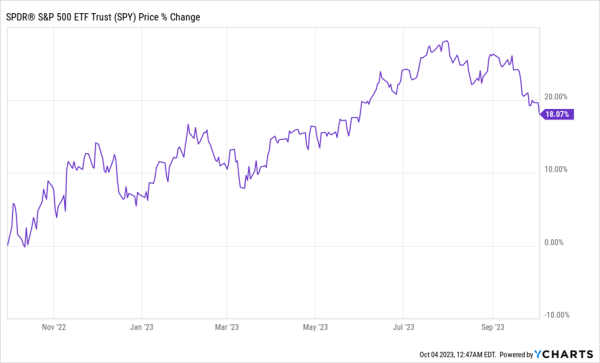

I recently got a really good question from a reader, who wondered how our current market situation compares to the 2008–2009 crash.

The short answer is that it really doesn’t. But the longer answer is much more interesting, and profitable, because it outlines the unique opportunity we now have to collect historically high dividends from my favorite income plays: closed-end funds (CEFs).

The Current State of Play for Income Investments

On cue, the current selloff has prompted the media to get on the gloom-and-doom train. As a result, we’re starting to see more fear in the markets. It’s tough to understate the impact this fear can have. Last year, for example, overwrought worry prompted stocks to tank, even as GDP kept rising.

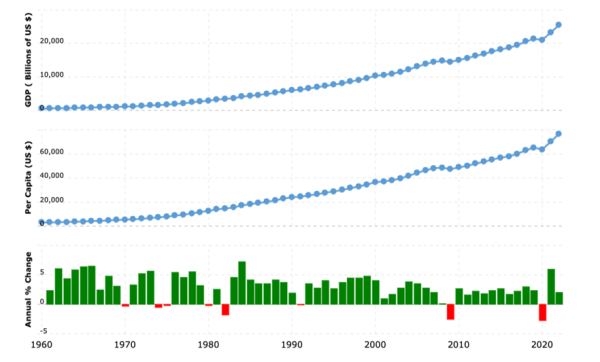

Bigger Economy, More Wealth … Lower Stocks?

Economic growth was 2.1% in 2022, which was of course much lower than in 2021. But 2021’s numbers were stacked up against 2020’s COVID shutdowns. Plus 2022’s growth almost perfectly hit the average of the last 30 years.

Stable Economic Growth = Stock Crash?

Source: Macrotrends

That made the dip in stocks we saw last year even more unusual. To be sure, stocks will sometimes dip before a recession, but this time they started tanking 22 months ago and hit bottom a year ago, and we still aren’t in a recession! This has never happened before, and it’s the start of our opportunity here.

GDP/Market “Disconnect” at the Heart of Our 2023 Buying Opportunity

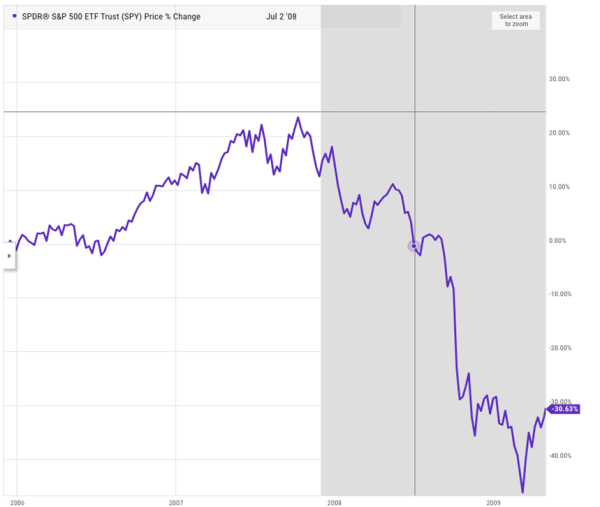

Of course, in 2009 a similar opportunity to buy the bottom appeared, which suggests that 2023 is closer to 2009 than 2007–2008, before the crash. But there’s another reason to think today is far from the peak of a market bubble.

Because we’re now in the fourth quarter of 2023, a technical recession—defined by two consecutive quarters of contraction—is impossible for this year. That means the stock market started tanking at least a full two years before any recession could begin! If we look back at two years before the 2008 recession began, we see a very different picture.

Big Hopes and a Big Drop

Stocks were up about 15% when the recession began in 2007, and they actually stayed up until the recession was nearly halfway over.

Before the 2008 market collapse and global recession, there was euphoria as houses back then inspired a bubble similar to what we saw in crypto, meme stocks and profitless techs this time around. But these latest bubbles turned out to be far from economy-killers—and are now sources of nostalgia.

So no, the data doesn’t suggest we’re in a pre-Great Recession style bubble, nor that we have any reasons to fear a stock crash or a decline in our dividend income.

And that, in turn, means we have a nice “buy-the-dip” opportunity on high-yielding corporate bonds, fast-growing tech companies and many more investments that have delivered gains and upside in high- and low-interest-rate environments.

What’s more, even if we are in another 2007, which the data shows we aren’t, it still doesn’t matter. Because even in that instance, you won’t lose out if you avoid risky assets and invest in high-quality funds that pay out as much of their profits as possible to shareholders as dividends. This is a defining feature of CEFs.

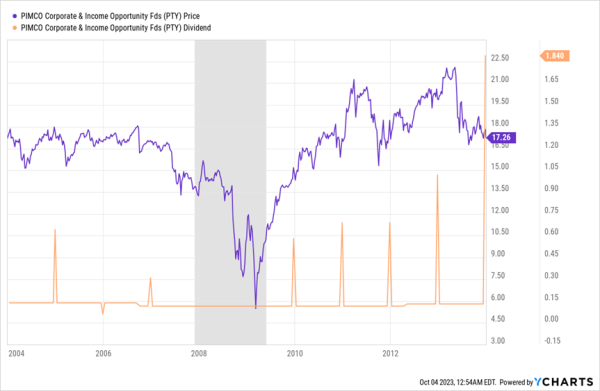

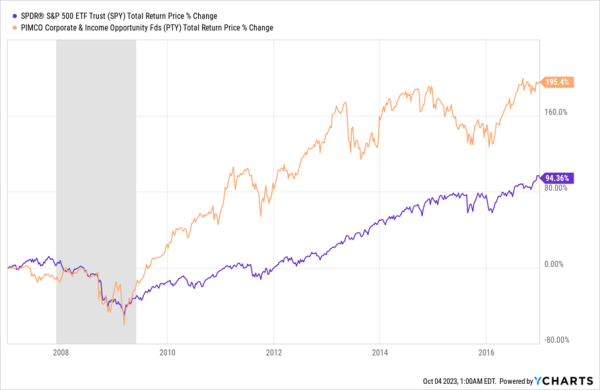

An “Ironclad” 13.1% Dividend That Cruised Through the 2008 Mess

There are particularly interesting dividend ideas in bond CEFs lately, like the PIMCO Corporate and Income Opportunity Fund (PTY), which now yields an incredible 13.1%. The historical record suggests strong returns over the long term from this fund.

Let’s look at 2007–2009, when PTY, like just about everything, was steeply sold off, as you can see in the purple line in the chart below (the gray shaded area indicates recession).

But the key thing about this fund, which is run by PIMCO, a storied name in CEFs that traces its roots back to the “Bond King,” Bill Gross, is that it never stopped paying distributions. And in fact, its distributions—shown in orange below—actually rose in the years immediately following the crisis, thanks to the incremental extra income PTY earned in the early 2010s, which it paid out to investors as special dividends.

PTY Outlasts the Subprime Mortgage Crisis

Heck, even if you bought PTY at the peak of the market in 2007, you still would’ve been just fine—more than fine, actually:

Pre-2008 PTY Buyers Booked Market-Crushing Returns

If you bought PTY at the start of 2007, at the height of the subprime-mortgage bubble, you would’ve outperformed the S&P 500 by more than double and earned an 11.4% total annualized return over that 10-year period. Obviously buying during the crash earns you even bigger profits.

So the key takeaway here is that whether it is 2007 or not, now is a good time to buy PTY. But the best news is that the data tells us we’re more like 2009 than 2007, although we’re really like neither because there’s no recession or even decline in economic activity in the data to worry about.

We Love PTY … But These 9.2%-Yielding CEFs Are FAR Better Pullback Buys

This selloff has laid out a rich hunting ground of dividends in front of us. PTY is an excellent choice: it comes from a top firm and has a history of soaring after a pullback.

There’s just one small sticking point: the fund currently trades for 22% more than its portfolio value. That’s actually normal—more or less in line with its five-year average premium. PIMCO holds sway over investors’ imaginations in the same way Apple captures the imagination of consumers.

Luckily for us, there are plenty of CEF bargains out there, starting with the 5 monthly paying CEFs I’m recommending now.

These 5 funds yield 9.2% on average and sport big discounts. Between them, they hold top bonds, global stocks, blue chip US stocks and real estate investment trusts (REITs).

And yes, they all pay dividends monthly.

Click here and I’ll give you their full backstory and let you in on some of my very best tips for picking winning CEFs. Then I’ll give you the opportunity to download a free Special Report naming all 5 of these bargain-priced monthly payers, so you can start collecting their rich 9.2% payouts.

Recent Comments