The safest dividend is usually the one that was just raised. Recession or no landing, bull or bear, these payers don’t care.

And neither should their shareholders because these stocks are growing their payouts between 33% and 100% per year. Per year!

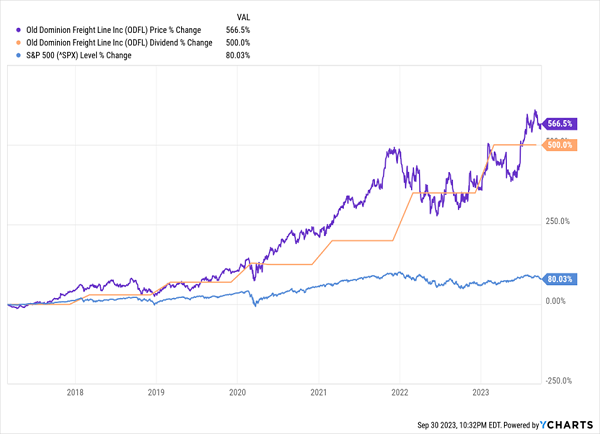

Here’s why we have safety in growth. Let’s consider Old Dominion Freight Line (ODFL), a less-than-truckload (LTL) freight shipping specialist with trucks crawling America’s interstates.

While transportation is a cyclical business, ODFL is a pinnacle of stability, delivering 30% annual profit growth on average over the past seven years. And while the stock hasn’t gone up in a straight line, it has crushed the broader market in that time.

ODFL’s Price Chases Its Payout

Who would think a “measly” 0.4% dividend would deliver 567% price gains! But look closely. The reason the yield is so low is that ODFL’s “dividend magnet” keeps towing its shares higher.

This virtuous refueling cycle keeps Old Dominion perpetually off the GPS of vanilla income investors.

With obscurity comes outsized profits. Want to get rich with stocks safely? It’s easy. Find the dividends that are growing the fastest.

Here are five dividend growers that should announce raises over the next three months. One year ago, these firms hiked between 33% and 100%. (That’s right, an instant dividend double!) If you’re looking for growth ideas, start here.

Coca-Cola Consolidated (COKE)

Dividend Yield: 0.3%

2022 Hike: 100%

Projected Q4 Dividend Announcement: Early December

No, no, not that Coca-Cola (KO).

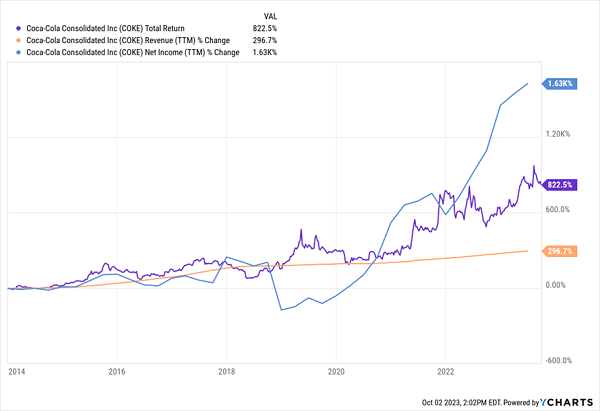

Coca-Cola Consolidated (COKE) is the largest bottler of Coca-Cola in the U.S., and also manufactures, sells, and distributes beverages for more than 300 brands and flavors—not just for Coca-Cola, but also Keurig Dr. Pepper (KDP), Monster Beverage (MNST) and other drinks names.

COKE has quietly put up one of the more impressive five-year strings of financials you’ll see. Revenues managed to grow during COVID (though net income took a step back before hitting the launching pad).

Coca-Cola Consolidated Takes Off

What’s really noteworthy is the separation COKE has made from both consumer staples (its actual sector) and industrials (given the nature of its business, a similar sector) over the past three years.

COKE Is Not Just Another Boring Staples Name

Despite this growth, COKE for years kept its dividend level at 25 cents quarterly—until December 2022, when it announced a massive $3-per-share special dividend, and a doubling of its regular payout.

But this December (expect an announcement early in the month) could tell us whether last year’s mega-hike was a one-time deal, or if Coca-Cola Consolidated is about to become a dividend-growth juggernaut. A laughably meager 3% payout ratio suggests it absolutely has the room to.

Owens-Corning (OC)

Dividend Yield: 1.5%

2022 Hike: 49%

Projected Q4 Dividend Announcement: Early December

Owens Corning (OC) is a global manufacturer of insulation, roofing and fiberglass composites. Its composites are used in everything from building structures to pools and showers to pools and showers to flooring and decking to wind-energy turbine blades.

Owens Corning is a largely cyclical company whose fates are tightly tied to the housing and construction markets. Indeed, insulation and composites are both seeing pullbacks, though the pros still think OC will escape this year with profit growth. That’s largely because input costs are also on the decline, which should help maintain or even grow margins, especially in roofing.

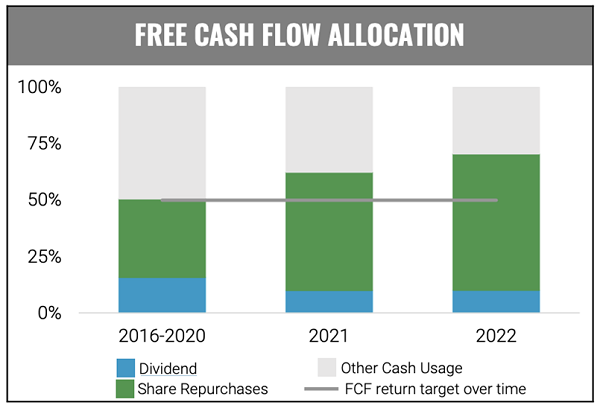

OC theoretically has a lot of headroom to raise the distribution given a skinflint dividend payout ratio of about 12%. But it’s worth wondering how many big raises are still in the company’s future. Back in November 2021, Owens-Corning said it planned to return 50% of free cash flow to shareholders over time. However, it has well exceeded that percentage over the past two years … and the lion’s share of that cash spend has been on buybacks, not dividends.

Source: Owens Corning Presentation, September Jefferies Industrial Conference

When you consider OC’s cyclical nature, it makes sense to keep the dividend (which investors expect to remain stable to rising all the time) lean, and instead favor buybacks, which the company can shift higher or lower without much pushback from investors.

Still, Owens-Corning hasn’t exactly been chintzy with payout hikes over the past few years, and has in fact doubled its dividend in just two years.

We’ll likely see what comes next in early December.

Marriott International (MAR)

Dividend Yield: 1.1%

2022 Hike: 33%*

Projected Q4 Dividend Announcement: Mid-November

Big payout raises in the hospitality industry have been commonplace for the past couple years. But that’s largely because many hotel and entertainment names had to slash or suspend their dividends during the worst of the COVID outbreak, and are now just trying to get back up to speed.

That’s very much the case for Marriott (MAR), a hotelier that needs little introduction.

Marriott is more than just Marriott, however. It actually boasts more than 30 brands, including Ritz-Carlton, St. Regis, W Hotels, Sheraton, Westin, Renaissance, Gaylord, Springhill Suites, Courtyard and Aloft.

At a recent analyst day event, Marriott put out a bold outlook for RevPAR, incentive fees, EBITDA, net rooms growth and numerous other metrics that largely exceeded expectations. Scale is a massive advantage for Marriott, whose Bonvoy loyalty program is now at 186 million members, who drive 61% of room nights globally and 67% in the U.S.

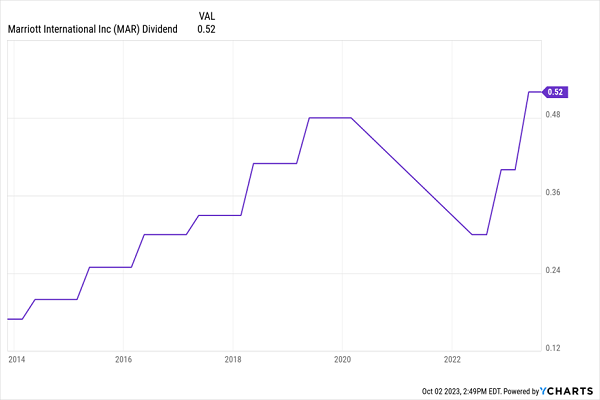

Marriott has been glad to share its renewed fortunes. MAR shares paid 48 cents per share quarterly prior to a 2020 dividend suspension. The payout resumed in May 2022 at 30 cents per share—then in November 2022, Marriott announced a 33% hike to 40 cents, then another 30% jump to 52 cents announced this May.

Marriott’s Dividend Is Officially Back

If another hike is coming, early November is one of the places it could show up. The question is: Will Marriott keep on the pedal or hit the brakes?

On the one hand, Marriott’s dividend now exceeds pre-COVID levels—it’s possible the steep raising over the past year-plus has just been catch-up speed. Also, MAR, as another cyclical name, understandably spends far more on buybacks than dividends ($2.6 billion vs. $321 million last year).

On the other hand, Marriott was pretty generous about its hikes prior to the COVID suspension. It’s possible the hotelier is just getting back on track.

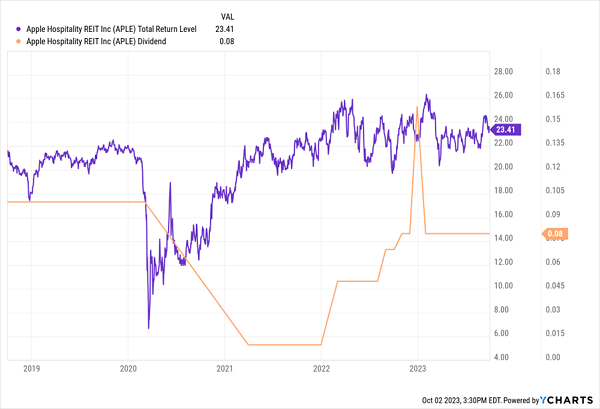

Apple Hospitality REIT (APLE)

Dividend Yield: 6.3%

2022 Hike: 60%

Projected Q4 Dividend Announcement: Mid-October

Apple Hospitality REIT (APLE) is a real estate investment trust (REIT) that boasts 220 hotels in 87 markets across 37 states. Just like many other hotel REITs, Apple doesn’t just serve one hotelier—119 of its hotels carry a Hilton (HLT) brand, 97 are Marriotts and four sport the Hyatt (H) brand.

Apple Hospitality, like many hotel REITs, was absolutely gutted during COVID. Its share price sank by nearly two-thirds at its nadir, and the company quickly hacked at its dividend, suspending it for a few quarters in 2020.

APLE was relatively lucky—shares reclaimed all of their ground within a year, though shares managed to float only slightly higher since then.

Apple Hospitality is a tricky place. Its focus on select-service hotels is ideal given their high margins, and it has access to not just cities but high-end suburbs, which is a nice diversifier. The problem is moreso where the industry stands. An economic slowdown could affect hoteliers like MAR and hotel REITs like Apple Hospitality alike, but high interest rates also weigh heavily on cost of capital—less a concern for Marriott, which has a capital-light business, but more so for APLE.

The next time we can expect to hear Apple Hospitality weigh in on its dividend (in one way or another) is mid-October. And I’m very curious about what it has to say.

Is Apple Hospitality’s Payout Stuck Again?

Apple Hospitality resumed the payout in 2021 at a penny per share, then quickly raised it to 5 cents per share in early 2022. It raised twice more that year—to 7 and 8 cents per share, with the last announcement coming in mid-October 2022. Since then, the monthly dole has been flat, so the last chance for APLE to start a regular habit is this month.

Any dividend growth on an already generous (6%-plus) yield would be a welcome sweetener. And even a return to pre-COVID levels of 10 cents per share would represent a 25% hike from here—bringing the yield to nearly 8%.

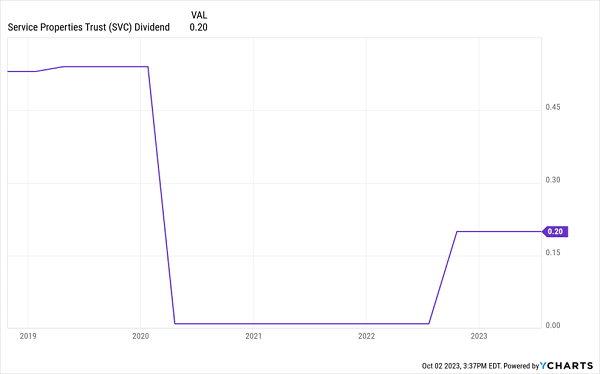

Service Properties Trust (SVC)

Dividend Yield: 10.6%

2022 Hike: 100%

Projected Q4 Dividend Announcement: Mid-October

Another high-yielding hospitality REIT that hasn’t yet brought its dividend back to par is Service Properties Trust (SVC).

But maybe, just maybe, it’s getting serious about fixing that.

Was Last Year Just the Start?

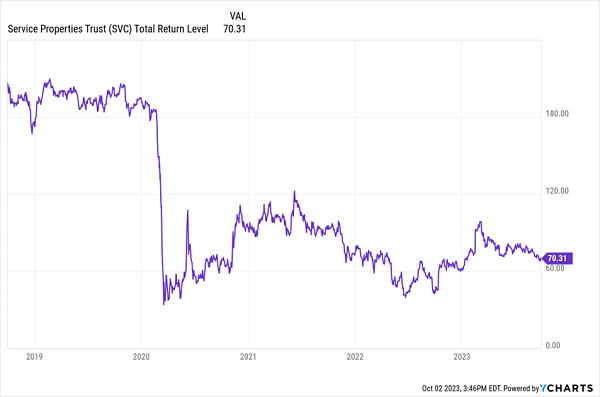

Service Properties Trust isn’t a pure-play hotel REIT. It does have a portfolio of 221 largely extended-stay hotels across most of the U.S., Puerto Rico and Canada. But it also has 763 service-focused retail net-lease properties, leased to the likes of TravelCenters of America, The Great Escape and Life Time Fitness.

SVC was particularly hard-hit during COVID. While diversification is usually a boon in down times, Service Properties Trust found itself exposed not just to hotels (which saw their business fall off a cliff) but also travel centers and discretionary retailers (which also saw their business fall off a cliff).

But unlike many of the above stocks, Service Properties Trust has been extremely slow off the mat.

SVC Still Trades at a Fraction of Its Pre-COVID Price

But again, the dividend makes me curious.

Last October, the REIT announced it was doubling its dividend to 20 cents per share—its first hike since cutting it by 81% in 2020. Which begs the question: Are bigger dividends in store?

SVC has largely delivered middling performance since COVID, though it’s largely expected to make significant leaps in funds from operations (FFO) over the next two years. And while pundits have warned of its dividend coverage, its FFO so far this year is more than double what SVC needs to tackle the payout.

The bigger question mark is the balance sheet. Service Properties Trust has unloaded more than 100 hotels since 2020, and this year, it also sold TravelCenters of America to BP (BP) for roughly $380 million. Nonetheless, it still has more than $1 billion in debt maturities to address in both 2024 and 2025.

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

That’s not to say SVC can’t tackle this issue—but it is to say you can find surer bets.

And given the potential for an economic slowdown or even recession, you want surer bets.

I don’t sweat economic pullbacks because I focus on rapidly rising dividends, which are often signs of a recession-resistant stock. But they’re not a perfect indication—hotel-related investments like Marriott and SVC clearly need the U.S. economy to hum along if they want to keep the pedal down on their dividends.

However, that’s not the case for a small, overlooked basket of recession-resistant stocks that haven’t just been surviving over the past couple years of market tumult—they’ve been thriving.

Better yet? They look like they could be the market’s best protective plays for the recession to come, regardless of whether it hits in 2023 or 2024.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here to learn more, including how to get a copy of my 5 Recession-Resistant Dividend Stocks With 100% Upside report, including full analyses of each pick … and I’ll throw in a few other bonuses, too!

Recent Comments