I have to admit, every year it gets harder and harder to do my taxes.

The process isn’t any more difficult—or at least if it is, my accountant isn’t saying! No, my problem is the money I end up owing.

Having to write a check to Uncle Sam for more than I earned in my first three years of working is hard to do. Which is why I’m always looking for ways to cut my taxes.

And really, the best way for me (and most likely you, too) is through a “boring” sounding investment called a municipal bond. There are three reasons why:

- Municipal bond, or “muni,” returns can amount to more than 9% per year for those in high tax brackets.

- Munis offer low volatility and are safe, with default rates below 0.2%.

- Munis provide income that’s 100% federally tax-free for most investors.

Any one of these points by themselves make munis attractive, but all three make them a no-brainer. So let’s dig into each one.

Big Tax-Free Returns

Munis are issued by local and state governments, mainly to fund infrastructure projects. To attract investment, the US government allows the interest these governments pay to be tax-free to the creditor. In other words, buy a muni bond and the income you get is not taxed by the federal government.

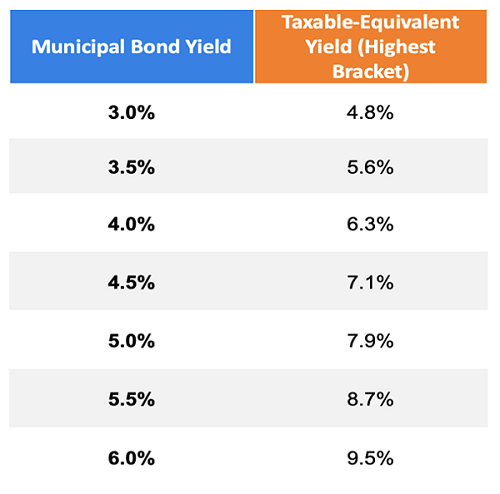

As a result, if we compare munis’ yields to those of corporate bonds or stocks, we have to adjust for the taxes we’d pay on those assets. The difference is huge.

For instance, a muni bond paying 4% interest would, for those in the top tax bracket, be the same as a 6.3% yield from bonds or stocks.

Right now, the average muni-bond focused closed-end fund (CEF) yields 5%, which is equal to 7.9% for high income earners. (CEFs, by the way, are our favorite way to buy munis, for reasons we’ll get into shortly.)

If we can get a 6%-yielding municipal-bond fund, though, that’s roughly the same as a 9.5% yield in stocks or bonds for investors in the highest tax bracket. And bear in mind that stocks historically boast total returns around 8% per year in the long run.

In other words, if you buy muni-bond CEFs at the right time and hold it for long enough, you might actually beat the market.

Munis Offer Low Volatility, Even in Times of Maximum Stress

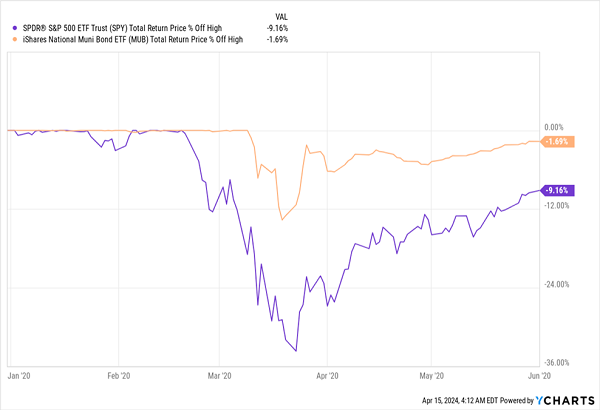

Another strength of municipal bonds is that they can lower the volatility in your entire portfolio. Consider this chart:

Munis Held Up Much Better Than Stocks in the 2020 Mess

In the early days of the pandemic, I’m sure you’ll recall, it felt like the world would never be the same again, with stocks selling off so fast that trading had to be halted in a number of sessions.

While munis did fall (everything did!), they didn’t decline nearly as much as stocks, and they recovered much faster, as you can see by the performance of the benchmark iShares National Muni Bond ETF (MUB), in orange in the chart above.

That lower volatility is because munis are known to be stable and reliable income sources. There are strict laws and rules that ensure these bonds get their capital and income back—laws and rules that don’t exist for stocks and corporate bonds.

That’s why the muni default rate is so low: 0.16%, a fraction of the rate for corporate bonds.

Why CEFs Are Our Best Option for Tax-Free Muni Income

The trouble with munis, from an individual investor’s standpoint, is that choosing one—heck even accessing this market—isn’t easy.

Munis aren’t very liquid, and muni-bond issuers tend to offer their best bonds to their best clients: banks and large firms managing billions, even trillions, of dollars.

Fortunately, you can get the best muni bonds through a muni-bond CEF. But there are literally hundreds to choose from, so how do we choose the right fund? To show how to analyze a muni-bond CEF, let’s pick three and unpack each one’s strengths and weaknesses.

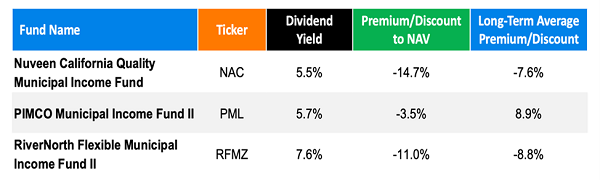

The Nuveen California Municipal Income Fund (NAC) and PIMCO Municipal Income Fund II (PML) are managed by two of the world’s largest muni-bond buyers (Nuveen and PIMCO). Both also offer similar yields, making them comparable.

NAC is limited to California, which makes it less diversified. But on the plus side, some California muni bonds are also free of California’s notoriously high state taxes, adding to their appeal for the state’s residents.

That could eventually prompt NAC to trade at a premium to net asset value (NAV, or the value of the bonds it holds), which would be a big jump from its current 14.7% discount (which, as you can see above, is nearly double its long-term average of a 7.6% discount—another sign of potential upside).

Now let’s swing over to PML, which, while national in scope, also has a California connection: It’s run by PIMCO, which is based in the state and is well-known by wealthy investors there. For that reason, PML, like most PIMCO funds, typically trades at a premium to NAV—an 8.9% premium over the long-term, in this case. So the fund’s current 3.5% discount shows there’s value—and upside—here.

That brings us to the RiverNorth Flexible Municipal Income Fund II (RFMZ). Its 7.6% yield would be 12.6% on a taxable-equivalent basis for those in the highest tax bracket.

I emphasized “would” here because RFMZ is a bit unique in that it isn’t fully tax-free.

The fund pays some of its income from taxed municipal bonds, which are a niche in the industry and often provide higher yields (which RFMZ needs, considering its own high yield). So RFMZ doesn’t offer complete tax-free income, and its current yield on NAV (or the yield as calculated on its NAV, and not its discounted market price) of 6.8% means it needs to keep looking for higher-yielding muni bonds.

That doesn’t mean RFMZ is a poor choice, but it isn’t the tax-free haven PML and NAC are. So if you’re focusing on taxes, it isn’t your best option.

5 MONTHLY Dividends With Payouts So High You Won’t Care About the Tax Bill

Okay, maybe that’s an exaggeration, but not by much!

Because the 5 other CEFs I’m pounding the table on now offer such an incredibly high dividend yield that, even though they are taxable, they’ll still pay you a bundle.

I’m talking about a monster 9.5% average payout here—and these funds’ dividends come your way every single month!

Recent Comments