Smart income investors know that the best REITs (real estate investment trusts) do just fine as rates rise. That’s been the case historically, and they’re rally again during this rate hike cycle too.

Why? Because elite landlords simply keep raising their rents. These higher cash flows translate to higher dividends, and higher stock prices, regardless of what the Fed is up to.

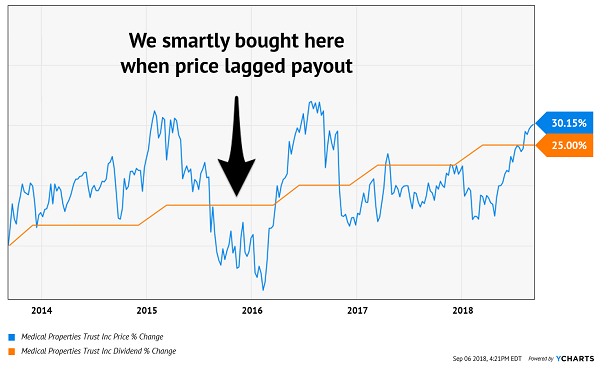

For example, almost three years ago I recommended Medical Properties Trust (MPW) to my Contrarian Income Report subscribers. It was paying nearly 8% at the time – discarded to the bargain bin because the first-level types fretted that higher rates would harm its ability to collect rent checks from its hospital operators.

Those fears were silly. MPW continued to “play Monopoly” in the hospital space, acquiring more and more valuable assets. Its higher rent income helped it generate higher and higher funds from operations (FFO) – which it then paid to us in the form of three dividend increases:

MPW Rises 15% Thanks to 3 Dividend Increases

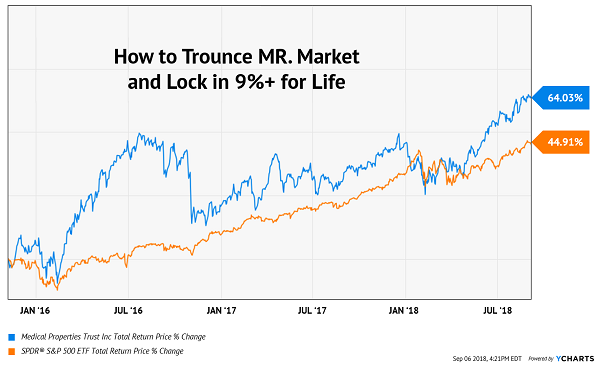

Once again it paid to be contrary and buy a perfectly safe, solid stock that the mainstream media simply hadn’t heard of. We banked the capital gains above plus 7% to 8%+ yields along the way, resulting in 40% total returns that beat the broader market to boot:

Have Your Big Yield and Beat the Market!

Who says we can’t have yield and growth? We have both – and our yield on cost is up to 9%!

What’s the next MPW? Let’s consider nine REITs that not only boast current yields of up to nearly 8% but are also extremely likely to announce a payout raise to their shareholders sometime over the next two months. When these REIT payouts rise, be ready for their share prices to follow.

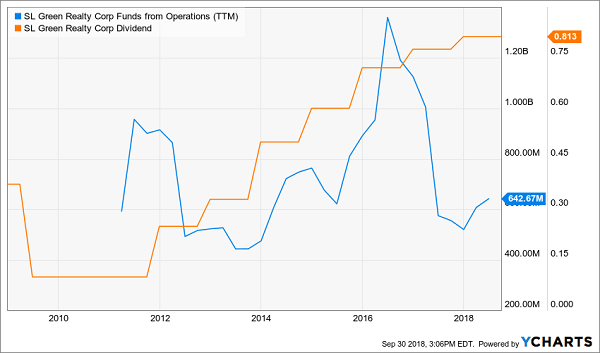

SL Green Realty (SLG)

Dividend Yield: 3.4%

Real estate’s broader malaise hasn’t even spared New York City’s largest commercial landlord, SL Green Realty (SLG). SLG shares are off about 4% year-to-date, matching the return of the Vanguard REIT ETF (VNQ).

This company’s ownership interests are split among 116 Manhattan buildings and 21 suburban buildings in Brooklyn, Westchester County and Connecticut. The former is performing admirably, with last quarter’s same-store occupancy rising 40 basis points sequentially to 95.9%. That helped drive an 8% year-over-year boost in same-store cash net operating income (NOI).

Investors should expect a bump in the quarterly dole to be announced sometime in late November or very early December – but don’t expect much. While the company’s dividend has blossomed by more than 60% since 2014, payout growth has slowed considerably during the past couple years.

SL Green’s (SLG) Payout Is Slowing Amid Choppy FFO

Simon Property Group (SPG)

Dividend Yield: 4.6%

Retail REITs were pummeled in 2017, largely thanks to the rotting of anchor-store retailers such as Macy’s (M), JCPenney (JCP) and Sears (SHLD). Things haven’t gotten any better for the latter two this year, but a rebound by Macy’s as well as numerous other retailers has breathed new life into at least a few REITs in the space, including the largest one: Simon Property Group (SPG).

Simon Property Group owns or has an interest in 234 retail properties, mostly malls and outlet malls, across North America, Europe and Asia. It has been a busy REIT over the past few months, too, opening up a new outlet center in Denver and partnering with Macerich (MAC) in a joint venture to open another outlet facility in Los Angeles. But perhaps most interesting is its solution for failing Sears locations, turning them into retail, fitness, dining … even hotel and office space.

Simon is starting to show true signs of resilience on its income statement, too, including a mighty 20% pop in funds from operations (FFO) in its Q2 report, prompting the company to improve its full-year guidance for the second straight quarter. Occupancy ticked up to 94.7%, too.

Simon’s dividend-hike schedule hasn’t been consistent over the past few years, and the company actually upped its payout as part of its Q2 report. But SPG has delivered a late-October dividend-hike announcement in each of the past two years, so keep an eye open for the possibility of another one this month.

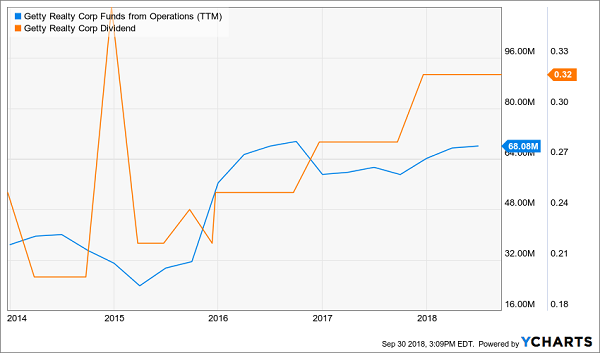

Getty Realty (GTY)

Dividend Yield: 4.6%

Getty Realty (GTY) is the kind of REIT that I expect to stand up well to the Amazon.coms (AMZN) of the world. That’s because Getty owns 932 gas station and convenience-store properties across 30 states, operating under brands such as Exxon Mobil (XOM), BP (BP) and Valero (VLO). That’s because Amazon hasn’t figured out gasoline sales (yet), and while Amazon can deliver almost anything, if you’re already on the road, convenience stores and gas stations still make the most sense.

The means stability and easy growth for Getty, which engages in long-term triple-net leases with rent escalations of 1%-2% per year.

2017 was a big year of expansion, with Getty snapping up 103 properties, and that’s starting to bear fruit in 2018. Through the first half of the year, Getty’s adjusted FFO has come to 85 cents per share – an improvement on last year’s 83 cents. That should help finance another dividend raise for GTY, which has kept the pedal down on its payout for years. Expect Getty to make the announcement in the last week or two of October.

Getty Realty (GTY) Pumps Out a Dividend Growth Story

Stag Industrial (STAG)

Dividend Yield: 5.3%

I write about warehouse owner STAG Industrial (STAG) pretty frequently. That’s no accident. STAG is a 5%-plus monthly dividend payer whose management prioritizes payout growth.

STAG is a highly diversified real estate play that owns 370 buildings across 37 states, leasing them out to companies in more than a dozen different industries, including automobiles, materials, transportation and retailing. Occupancy is a high 95.6% as of the last quarter.

The company also isn’t beholden to just holding crappy properties for the sake of maintaining ever-large numbers – it frequently sells underperforming properties so it can put the money back to better work. For instance, in the second quarter, STAG made acquisitions in 13 different markets.

Better work, indeed: AFFO for the first six months of 2018 came to $87.9 million – 19% higher than the year-ago period. That’s good news for continued growth in the monthly dole; management typically announces its intent to boost the payout in the first week of November.

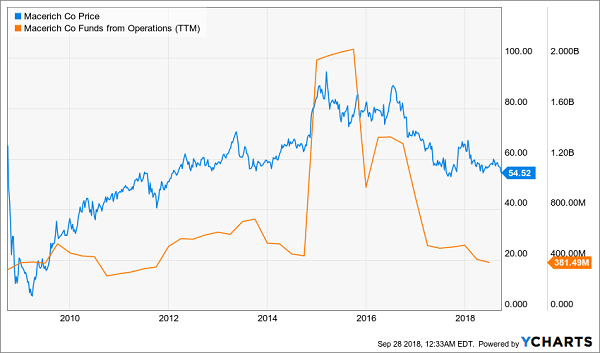

Macerich (MAC)

Dividend Yield: 5.4%

Macerich (MAC) is a high-end retail REIT with 48 properties heavily concentrated in the East and West Coasts – markets that are densely populated and have high barriers to entry.

While a focus on more well-to-do consumers is more often than not a winning strategy, Macerich has stagnated from a performance standpoint, with FFO falling to the bottom of its 10-year range.

Macerich (MAC) Still Reflects the Weakness in Retail

Like Simon, Macerich is trying to think outside the box to cure its occupancy ails, such as flexible workplaces in its malls, and the aforementioned outlet-mall JV with Simon. But results haven’t been as bright and shiny, with FFO actually trailing a bit in the real estate operator’s most recent report.

Dividend growth has trailed off, too, with the company’s regular 3-cent annual hike representing an ever-smaller percentage that has drifted down to the low single digits. There’s little to think that will change in the back half of October, when Macerich typically announces a payout boost.

Preferred Apartment Communities (APTS)

Dividend Yield: 6.0%

I’ve previously called Preferred Apartment Communities (APTS) a perfect buy for rising rates, in part because of its penchant for keeping its payout aloft with dividend increases.

I expect that to continue with an announcement in late October or early November, when it typically informs shareholders of a raise.

Preferred Apartment Communities is a multifamily residential real estate operator, but a pretty diverse one that steps outside its primary business. While it owns 31 multifamily communities, it also owns 31 multifamily communities, 43 grocery-anchored shopping centers, seven student housing properties and five office buildings.

APTS has plenty of fuel for a dividend hike: The company has earned 63.3 cents in AFFO through the first six months of the year (up 8.6% year-over-year), but has doled out only 50.5 cents per share in dividends – a very responsible 80% payout ratio.

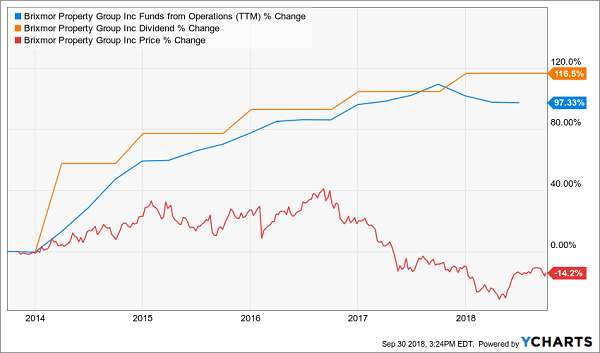

Brixmor Property Group (BRX)

Dividend Yield: 6.5%

Brixmor Property Group (BRX) – which at more than 475 commercial real estate properties in 36 states is one of the largest owners of open-air shopping centers – is squarely in Amazon’s crosshairs. After all, its tenants include the likes of Walmart (WMT) and grocery mega-chain Kroger (KR), among others.

You’d know it by looking at the share price over the past couple years, but not by looking at operational performance and management’s cool-as-a-cucumber demeanor.

Is a Bargain Developing at Brixmor (BRX)?

But the stock does appear to be stabilizing in the latter half of 2018, perhaps in part because they how much progress Brixmor is making in improving its foundation. The company has freed up all of a $1.3 billion credit facility and now is working on knocking out future-year debt.

I don’t expect Brixmor to forget its obligation to shareholders, even if it is pinching pennies to pay off debt. Another dividend-hike announcement should come in or around the final week of October.

Iron Mountain (IRM)

Dividend Yield: 6.9%

Iron Mountain (IRM) is the data-center REIT that’s oh so much more than that. Yes, the company offers high-tech solutions such as data-center storage, imaging services, media restoration and even workflow automation. But it also has a presence in physical documents, including secure records and media storage, shredding and industry-specific services.

The company is an unsurprisingly steady bloomer that has improved its normalized funds from operations by roughly 26% in just three years. Things continue to go well this year, including FFO of 56 cents per share in the second quarter that was enough to beat analyst estimates.

Iron Mountain pays out only 73% of its funds from operations as dividends, so expect another payout-hike announcement sometime in late October, when IRM typically shares good news with its stockholders.

Kite Realty (KRG)

Dividend Yield: 7.8%

Kite Realty (KRG) is the highest-yielding REIT on this list, at nearly 8%, but it has gotten to that ballooned yield the wrong way: a hemorrhaging share price.

Kite Realty (KRG) Could Use a Gust of Wind

Shares have plunged 18% this year despite some decent results, including a 4% sequential improvement in AFFO for its second quarter, as well as 1.5% year-over-year growth in same-store net interest income. Moreover, the REIT is aggressively deleveraging, with 6.5x leverage nearing its goal of 6x leverage.

But the company has been suffering longer-term from the narrative and very real numbers. Kite Realty is a retail REIT that specializes in neighborhood and community shopping centers, so everyone knows its tenants are right in the crosshairs of Amazon, which rightfully makes them fearful. But the company’s FFO has been consistently dipping too – so this may not be just a boogeyman story.

All that said, Kite Realty has been good for a dividend-raise announcement near the end of November for years, and its operating results should keep that in play for this year.

My Top 2 REIT Buys: Recession and Rate-Proof Landlords for 7.5%+ Yields with 25% Upside

My two favorite REITs today are comfortably positioned in recession-proof industries. They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what President Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks, and then it sends most of the profits our way as dividends (a legal requirement to have REIT status).

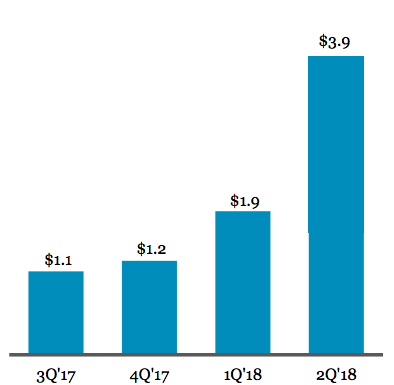

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

Quarterly Origination Volume ($ in Billions)

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, while it makes the investments which will drive its payout and share price higher from here.

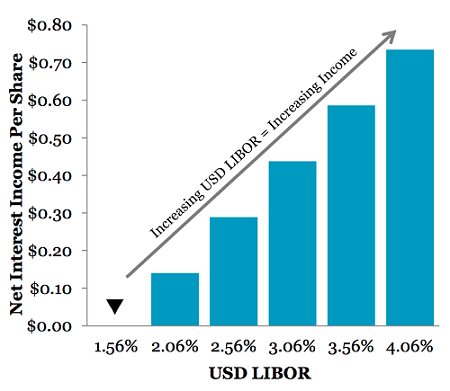

Plus, this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

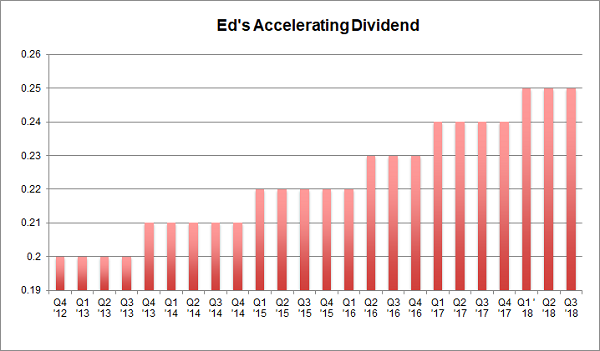

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

Its founder Ed admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well, his dream and plan were plenty – the visionary entrepreneur parlayed them into $6.7+ billion in assets!

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so it can afford to pay us shareholders more. And an accelerating payout is a flat-out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So, leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile, investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy (after we already own it, of course).

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever. Click here and I’ll share how you can get a complimentary copy of my premium REIT research.

Recent Comments