The stock market doesn’t just hand out safe yields up to 11.8%, vanilla money managers will tell you. And they are mostly right—but sometimes wrong.

When these 11.8% dividends are safe to buy, it can really pay to be contrarian.

An 11.8% yield means that a million-dollar portfolio can generate $118,000 in passive income per year. That is a solid six-figure salary to start with.

It is dividends like these that make mREITs (mortgage real estate investment trusts) so attractive. We’ll highlight three today that yield between 10.3% and 11.8%. But first, a business primer.

mREITs: Big Dividend Rewards (with Risks)

Equity REITs own and maybe even operate a number of properties, be they malls, hotels, hospitals or even driving ranges. They’re required to pay 90 cents of every dollar in taxable profits as dividends to investors. So, they tend to out-yield most traditional sectors, making them a popular choice among retirement planners.

mREITs don’t own any physical properties—but they still dish big dividends, thanks to their corporate status.

mREITs deal in paper—mortgages, to be exact, and usually of the residential or commercial kind. They try to borrow at cheaper short-term rates, then buy up securitized mortgages, effectively “lending” at (hopefully higher) longer-term rates.

It’s a capital-efficient business that can produce big payouts. 10%+ dividends are common, and mREITs typically pay the most of all REITs.

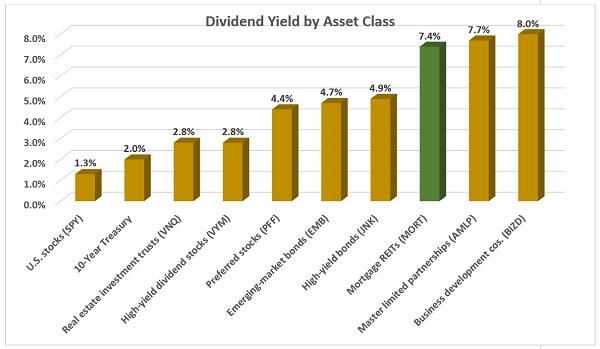

mREITs: Some of the Fattest Dividends You Can Find

On average, the sector pays 7.4%. As mentioned, most yields this generous carry question marks. (If they didn’t, their yields would be less because their prices would get bid higher by other income investors looking for yield.)

Traditional mREITs do best when long-term interest rates either remain flat or decline. That’s because as long-term rates decline, new loans pay less, making existing mortgages more valuable.

This dynamic tends to suffer when rates rise because it shrinks the value of these mortgage portfolios. Historically speaking, periods of rising interest rates have rocked mREIT prices and caused many companies in the space to shrink their dividends.

This is a problem right now because:

- The Federal Reserve itself collectively predicts it will raise benchmark rates three times in 2022.

- The CME FedWatch Tool, which acts as a barometer of markets’ expectations for future rate hikes, shows a 60% likelihood of five rate hikes this year.

- Goldman Sachs, Bank of America and a few other research firms are predicting seven interest-rate increases before 2022 ends.

That’s a disastrous setup for all but the most resilient of mREITs, which is largely why the industry has collectively declined more than twice as fast as the broader market.

Are any mREITs worth buying today? We want to make sure the payout and the price are safe. After all, what’s the point of an 11.8% yield if we lose 11.8% per year in price?

Let’s look at that mREIT trio I mentioned earlier.

Ready Capital

Dividend Yield: 11.8%

Ready Capital (RC) originates, acquires, finances and services small- and medium-sized balance commercial loans. Ready’s primary business is in small balance commercial (SBC) loans, with originations (35%) and acquisitions (13%) combining to make up roughly half of core earnings. Another quarter or so comes from Small Business Administration 7(a) loans, 19% is from residential mortgage banking and the remainder is a peppering of various other investments.

The bigger-picture breakdown of Ready Capital’s business—at least as it pertains to our current rising-rate situation—is its percentage of fixed-rate loans versus floating-rate. Good news there: Virtually all of its SBA 7(a) loans and more than two-thirds of its SBC loans are floating-rate, which means RC is better positioned to roll with the punches of rising interest rates than competitors who are more heavily beholden to fixed-rate mortgages.

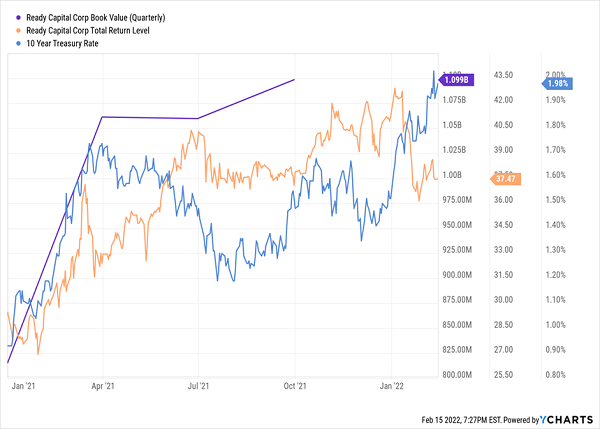

We’ve yet to see how RC did during Q4 2021, let alone in Q1 2022 when interest rates really took off. But you can see in the chart below that an escalation in rates at the start of last year certainly did nothing to hurt the company’s book value.

RC Holds Its Own Amid Rising Rates

One thing to note is that Ready Capital recently completed a 7 million-share equity raise in mid-January But to the company’s credit, it did so the “right way”—announcing the share sale while it was trading at well more than book value, resulting in a sale that still occurred somewhat above book value.

But again, the most important thing here is Ready Capital’s portfolio construction, which sets it up perfectly to weather what’s expected to be an active Federal Reserve this year.

AGNC Investment Corp. (AGNC)

Dividend Yield: 10.5%

Let’s look at the flip side of the coin.

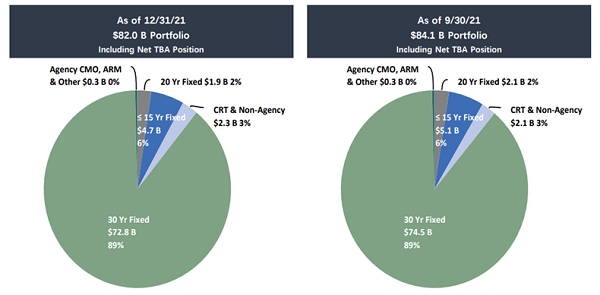

AGNC Investment Corp. (AGNC) invests almost exclusively in agency mortgage-backed securities (MBSs). As of the end of 2021, AGNC’s $82.0 billion portfolio included $52.6 billion in residential MBSs, and most of the rest ($27.1 billion) in a “TBA” position.

And yes, that does indeed mean “to be announced.” We know they’re going to involve AGNC either buying or selling MBSs, but we have no idea at what price, face amount, who’s issuing, etc. We will at a later date, just not now.

If this sounds familiar, that’s because I examined AGNC back in mid-November and cautioned readers about its portfolio construction. At the time, almost 90% of its agency portfolio was in 30-year fixed mortgages, and not much has changed since then.

Source: Q4 2021 Shareholder Presentation

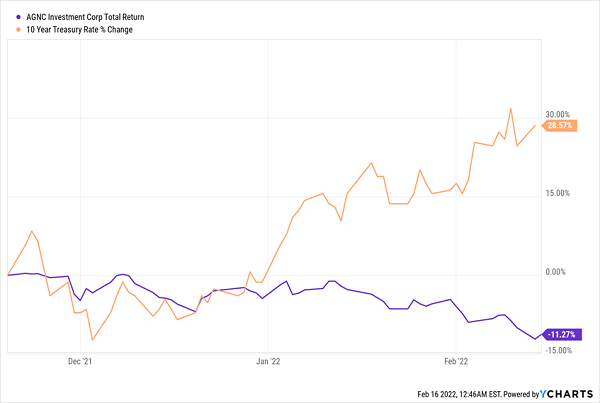

I said at the time this was a warning sign—and investors who heeded that warning have avoided double-digit losses.

Higher Rates Have Hampered AGNC

Couple this with management that has no compunction about slicing the dividend—the company has pared back its payout four times in the past six years—and you have an mREIT that’s ill-equipped for the next few years of hawkish Fed rule.

Ellington Financial (EFC)

Dividend Yield: 10.3%

Mortgage REIT Ellington Financial (EFC) offers a 10%-plus dividend and quite a diversified mortgage portfolio, with assets split roughly 50-50 between credit and agency loans.

A Durable, Diversified Collection of Loans

On the agency side, Ellington is overwhelmingly invested in fixed-rate specified pools, though it has trace holdings in reverse mortgage pools, floating-rate specified pools and other instruments.

But things are a little more rising-rate friendly on the credit side. The majority of assets are in residential mortgage loans and real estate owned (REO), but there’s also sizable holdings in commercial mortgage-backed securities, commercial mortgage loans, non-agency residential MBSs, consumer loans, investments in loan origination entities, even corporate debt. Various aspects of this are floating-rate in nature, including virtually the entirety of its small balance commercial mortgage loan portfolio.

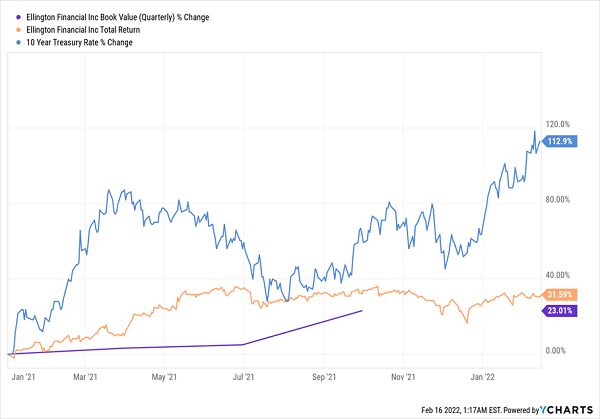

Like with Ready Capital, we’ve yet to see how the past four or five months have affected Ellington’s book value, but what we have seen over the past year before that is encouraging.

What’s less encouraging is EFC’s dividend history, which includes six different cuts to its monthly dividend since 2013—from 77 cents per share down to as little as 8 cents in 2020 before rebounding to its current 15 cents. So while it seems like Ellington has built something of an all-weather portfolio here, it’s exceedingly difficult for serious income investors to trust that this payout will remain stable over extended periods.

Sky-High Dividends You Can Count on for DECADES

But isn’t that how it always seems to go when it comes to high-yield stocks? They always seem to have so many “buts.”

- Nice yield … but rising rates will tear it to shreds.

- Great payout … but it’s always being cut, not increased.

- What a dividend … but the stock swings around like Tarzan.

The majority of the market’s most mouth-watering payouts force you to make some sort of critical tradeoff. But a few select gems offer it all: The right payout, the right price, the right potential.

And these stocks are all part of my “Perfect Income” portfolio.

Most of my readers have told me that these stocks have doubled and even tripled the dividends they were earnings from their old income portfolios. (And in a couple of rare cases, readers reported a 4x jump in their regular checks!)

That alone is a massive upgrade to any set of retirement holdings. But more important is that my Perfect Income Portfolio delivers that level of cash while also…

- Paying those dividends consistently, predictably and reliably.

- Surviving, even thriving, in market crashes.

- Delivering double-digit returns across several safe investments.

- Gambling your hard-earned nest egg on flimsy day-trading strategies, options contracts or penny stocks.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Let me show you how to get 2x to 4x your current income with this simple, straightforward system. Click here to get a FREE copy of my Perfect Income Portfolio report, including tickers, dividend yields, full analyses of each pick … and a few other bonuses!

Recent Comments