Vanilla investors buy stocks that Wall Street approves of.

Why?

If a stock is showered with Buy ratings, then who is left to bid the price even higher? Nobody!

This lame “strategy” feels good but ends up with latecomers top ticking the market. Which is why we contrarians aim differently—for the bottom of the barrel.

Give us stocks with Sell ratings. Which often means there’s nobody left to sell!

Today we’ll discuss a pack of discarded dividend stocks paying up to 12.6%. Not only are these yields real, and spectacular, they have price upside potential to boot.

After all, a stock slathered with Sell labels has nothing but upgrades in its future. So let’s go dividend dumpster diving and fish out these 6% to 12.6% payers together (how romantic, I know).

Analysts’ Trash Is Our Treasure

Here’s why this tactic works. Let’s say Corporation Inc. (FIRM) has roughly doubled in price over the past year. It’s a mega-cap stock, so a whopping 40 analysts cover it, and every last one of those analysts says Corporation is a screaming Buy.

Wall Street literally can’t get any more bullish on FIRM. And that’s a problem. There’s virtually nowhere to go but down. And a crack or two in that wall of optimism could easily open the floodgates on those crowded shares.

Now take the flip side. Imagine Corporation Inc. has lost half of its value over the past year, and every analyst who covers it says it’s a Hold or a Sell.

Now, you have the opposite situation. You have virtually nowhere to go but up, and an upgrade or two could send buyers into the stock, which drives the price higher and convinces more analysts to upgrade their views so they don’t look like they’re behind the 8-ball, which drives more buying, and—I think you get where I’m going with this.

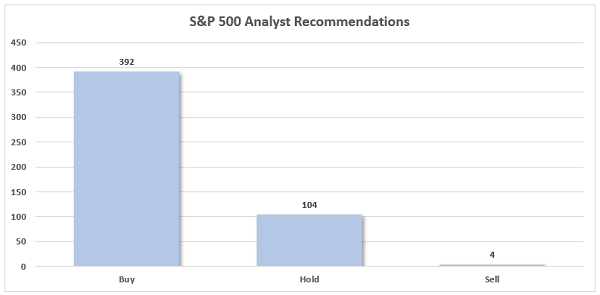

Bearish calls are also interesting to us because they’re rare. Analysts know how they get their advantageous access, and it’s by putting a positive spin on whatever they can. So it’s extremely unusual to find stocks that are consensus Sells.

How unusual? The S&P 500 has just four right now!

Source: S&P Global Market Intelligence

The only thing better than a true contrarian stock, of course, is a contrarian stock with a massive dividend. So, let’s sit down and explore what Wall Street can’t stand right now—a seven-pack of massive yields in the 6.3% to 12.6% range.

Regular Stocks

B&G Foods (BGS, 6.3% yield) might not be a first-to-mind name in the consumer staples space, but it boasts some of America’s most well-known grocery brands, including Crisco, Cream of Wheat and Green Giant.

You’d think a consumer staples name would look good against a potential recessionary backdrop, but that’s not the case here. No analyst currently calls BGS a Buy, while five say it’s a Hold and one says it’s a Sell. And again, Wall Street typically wears rose-colored glasses, so that’s a pretty bearish consensus Hold call.

You might remember that BGS was a Dividend Swing Trader play—and importantly, it was never anything more for us because of its weak fundamentals.

In 2022, a couple years after we exited, B&G Foods cut its dividend by 60%, to 19 cents per share, where it remains today. The company is still loaded up on debt—more than $2.2 billion worth, which is more than twice its market cap.

BGS does trade at just 40% of sales, however, and a reasonable 11 times earnings estimates. But that’s only a “value” if B&G’s fundamentals start improving.

B&G Foods Has Spoiled Since the Start of 2022

In April, I said investors should sell Cracker Barrel Old Country Stores (CBRL, 6.8% yield), and here’s hoping you did—CBRL shares have lost a quarter of their value since then. But just about any stock is worth a re-examination after a move that big.

On the upside, Cracker Barrel has seen success with budget offerings, such as its $5 takeout meals, and it is also expanding its catering business. But costs continue to weigh hard on the restaurant—in its latest earnings report, management lowered its Q4 revenue estimates, which also brought down its full-year implied revenue estimates. Lowered Q4 margin expectations also dragged full-year implied estimates, to the lower 4% area from upper 4% previously.

Wall Street is actually more bullish on CBRL than it has been in prior months, albeit at two Buys, five Holds and three Sells—still a bearish consensus. But I’m no more optimistic about Cracker Barrel than I was back in April.

REITs

It’s not uncommon to find hated high yields in the real estate investment trust (REIT) space.

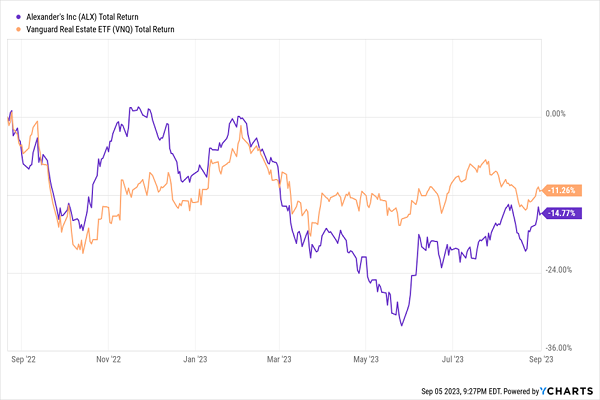

Last August, I warned investors about a handful of office REITs, including Alexander’s (ALX, 9.4% yield), which is actually managed by Vornado Realty Trust (VNO) and owns five properties in the greater NYC metropolitan area. ALX has since waffled between breakeven and deep in the red since then, and it’s currently sitting on 15% losses—even after factoring in its nearly double-digit dividend.

Alexander’s: Not So Great

No. 1 with a bullet is the safety of Alexander’s dividend. Through the first six months of 2023, ALX generated $7.18 in funds from operations (FFO), but it paid out $9.00. That’s not a slight issue with dividend coverage—it’s a massive one that could end up seeing Alexander’s face the same fate as Vornado (one of New York’s biggest office landlords), which earlier this year suspended dividends through the rest of 2023.

But I’d steer clear of ALX in both directions. While it doesn’t feel like a safe buy right now, you could get punished for betting against it, too. Return-to-office initiatives are gaining steam, and while some form of hybrid work will probably remain the norm forever (and thus office REITs will never reclaim their old glory), the entire industry could see at least a temporary tailwind.

LTC Properties (LTC, 7.1% yield) is a national REIT that’s roughly 50/50 split between senior housing and skilled nursing properties. The worst of COVID is long behind it, but even this year, LTC has had to shell out deferrals and abatements to troubled tenants.

The pros sure don’t like LTC, which has zero Buys, four Holds and two Sells. But the dividend appears to be safe here, and long-term, there’s no denying the importance and stickiness of these kinds of properties. I don’t see much sparking the stock in the immediate-term, but extremely patient investors might give LTC a closer look.

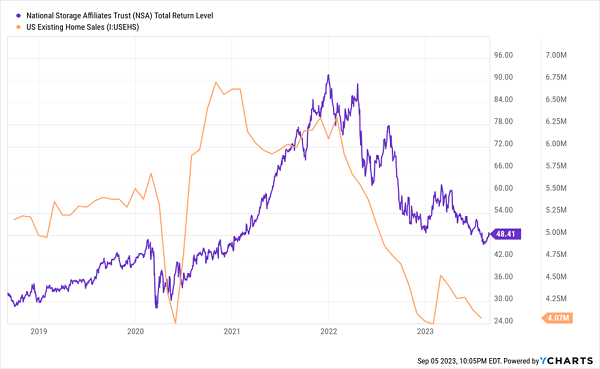

National Storage Affiliates (NSA, 6.6% yield) is a self-storage REIT with more than 1,100 self-storage properties in 42 states and Puerto Rico. We actually held this name long ago, but sold it (for a 40%-plus gain) amid a glut of supply and slack demand for these mini-warehouses.

NSA shares actually exploded post-COVID, but virtually all of those gains have evaporated right alongside activity in the housing market.

As Went America’s Housing Boom, So Went NSA

NSA is an interesting self-storage REIT in that it’s more of a collective—its PRO (participating regional operators) program brings in private self-storage operators. It brings in more units through strategic joint ventures and third-party acquisitions.

The pros don’t see much to like about NSA, which has zero Buys versus nine Holds and three Sells. But there’s little wrong with NSA itself. It’s operated competently, and its dividend is well-covered at about 85% of estimated 2023 FFO. It’s merely dealing with a crappy environment for all self-storage names—a mix of extremely high home prices, high interest rates and the potential for a recession all bode poorly for its short-term prospects.

Eventually, that should pass.

BDCs

Business development companies (BDCs) have a reputation for super-sized yields, and two hated stocks live up to that in spades.

I’ve long knocked around Prospect Capital (PSEC, 12.0% yield)—a monthly payer whose performance has never quite lived up to its payout potential.

Prospect, for the record, is a big fish that has funded more than 400 investments across roughly two decades of publicly traded life. At the moment, it has $7.7 billion invested in 127 companies across 37 industries.

PSEC only has one Sell call on it, but it’s the only analyst call there is—BDCs aren’t exactly a popular feeding ground for analysts in the first place, but most of Wall Street has abandoned coverage after years of dreadful performance.

I guess if they can’t say anything nice, they’ve chosen not to say anything at all.

To PSEC’s credit, non-accruals are virtually nonexistent, and dividend coverage has been improving over the past few quarters. So investors don’t have an immediate concern about Prospect Capital putting its payout on the chopping block like it has in the past. But if you’re going to bet on BDCs, you probably want to stick with best-in-class operators ahead of what could be a difficult operating environment (read: recession) for the small businesses they invest in—and PSEC is simply not one of those.

Goldman Sachs BDC (GSBD, 12.6% yield) is a BDC that can “draw upon the vast resources of Goldman Sachs to assist in the evaluation of potential investment opportunities.” It typically invests between $25 million and $75 million in companies with EBITDA of between $5 million and $75 million annually. At the moment, Goldman sees fit to hold 135 portfolio companies across 36 industries.

Despite its pedigree, GSBD hasn’t provided much of a premium as far as performance is concerned. It provides pockets of outperformance and underperformance, though its more recent performance has really put it behind the 8-ball.

GSBD Doesn’t Really Live Up to the Brand, Does It?

The pros are either on the sidelines (five Holds) or against GSBD (one Sell). I tend to agree here.

The company has some notable problems, including a debt-to-equity ratio of 1.2 that has persistently remained above company targets all year. Also, another couple of companies were placed on non-accrual in Q2, raising non-accruals as a percentage of amortized cost to 1.8% from 1.6% in Q1.

You can seemingly rely on the dividend, which sits at about 80% of adjusted net investment income over the past year. But the dividend is really the only worthwhile aspect of GSBD—price performance is deeply negative since inception.

A Once-in-50-Year Retirement Storm Is Hitting Us NOW (Here’s Our Gameplan)

I love contrarian plays—stocks that investors and analysts alike have soured on.

But now, more than they have in a very long time, fundamentals matter. Because we’re in the midst of a rare, once-in-every-50-years retirement storm that requires us to laser-focus on quality—or risk cracking our nest eggs wide open.

The last time we saw anything like this was the late 1970s! But if you were investing back then, you’ll also remember that right afterward, stocks took off in a raging bull market that led straight into the early 2000s.

Sure, history never repeats exactly, but it does rhyme, which is why I see better days ahead. I’ve explained my rationale in a Special Investor Bulletin you can read right here.

But what about right now? How do we protect our dividends until the skies clear?

We’re not powerless. Far from it.

Our goal right now is to safeguard our cash and set ourselves up for gains (and outsized dividends) on the other side of this mess.

When you read my Special Investor Bulletin, I’ll show you how to access three special reports that both lay out the high yielders best positioned to hand us sturdy dividends and upside as we roll through this bear market—and reveal the 12 stocks you MUST sell now before these dividend pretenders yank the rug out from underneath you.

Recent Comments