Stick with me for some “next level” dividend thinking. We have a potential opportunity right now to buy five payers yielding up to 14.9% as the economy heads into recession.

Wait, what? Why would we want to buy stocks as the economy slows?

Well, we don’t want to own any names. We’ll pass on sky-high AI darling NVIDIA Corp (NVDA). Give us cheap REITs (real estate investment trusts) because they are likely to rise as rates fall.

Yes, that’s what happens in a recession. Investors flood into fixed income. Interest rates fall, and REITs—which tend to move opposite rates—rise.

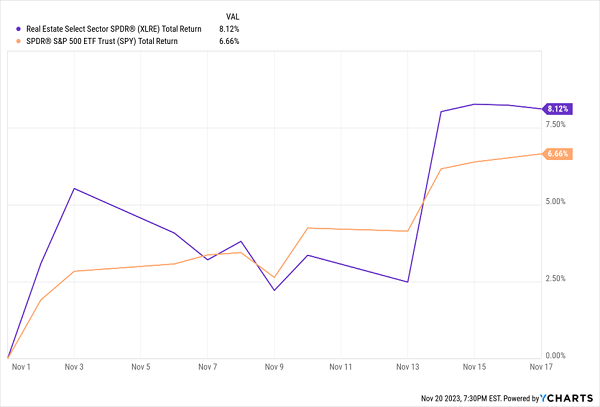

These landlords are already getting up off the mat after a rough two years in which rates rose relentlessly. It was a November to remember for the sector, with the sector benchmark elevating 8.1%:

REITs Finally Rose in November

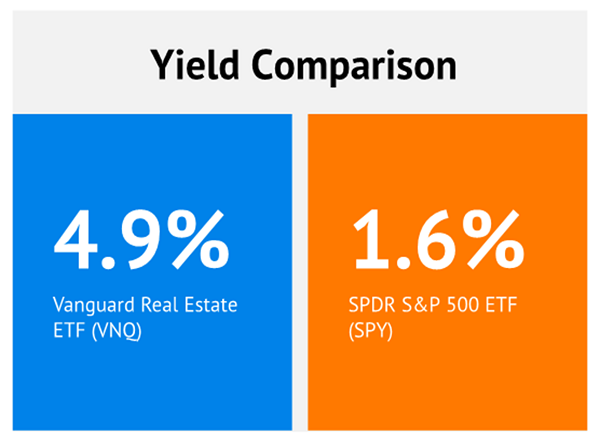

I called this REIT rally a couple of months ago and, well, it arrived ahead of schedule and in full force. Yet these stocks aren’t expensive by any means thanks to a two-year bear market. In fact they pay a lot more the stock-market average:

But be careful. The bucket is full of landlords that are going to have trouble collecting the rent in a recession. We want to avoid the office space peddlers and retail owners.

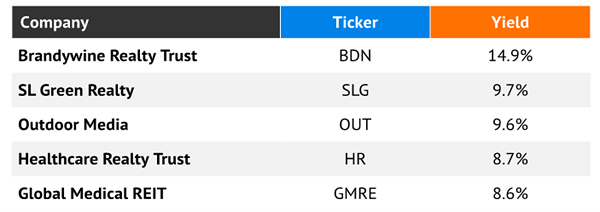

Let’s pick on a five-pack of REITs paying a terrific 10.3% today. Even after their nifty November, these dividends remain generous:

Outfront Media (OUT, 9.6% yield) is one of the more niche real estate plays you’ll find—it dabbles in ads.

More specifically, it dabbles in the places where advertisers want to place their ads. That is, billboards, transit stations and vehicles, and “mobile assets”—effectively, mobile ad campaigns tethered to, say, a customer’s store visit or presence in a specific area.

Outfront, like other REITs, has been hindered by rising interest rates, but its pain is somewhat more elevated due to weakness in transit. Specifically, post-COVID, ridership in metro systems like the MTA and WMATA has rebounded somewhat, but is still nowhere pre-COVID figures. Continued recovery, including back-to-office policies, should help OUT slowly but surely.

Until then, it remains steeply depressed. Even with a recent bounce in shares, Outfront’s stock trades at just 7 times estimates for adjusted funds from operations (AFFO), and it yields close to 10%. It’s a pretty safe dividend, at just 72% of AFFO.

Despite room for payout growth, it’s hard to tell whether that distribution will grow anytime in the near future. OUT management suspended its 38-cent-per-share quarterly dividend amid COVID, then brought it back at just 10 cents in 2021 before tripling it to 30 cents in early 2022. The dividend has remained pat since then.

SL Green Realty (SLG, 9.7% yield) is billed as “New York City’s largest office landlord.” It holds interest in 59 buildings totaling 32.5 million square feet, including 28.8 million square feet of Manhattan buildings. The business is overwhelmingly office-property in nature, at 92% of net operating income (NOI), though it also has trace retail and residential exposure.

SLG is not just a high yielder, but a monthly yielder—a practice it started in 2020. What it didn’t do in 2020, is cut its dividend like many, many other retail REITs.

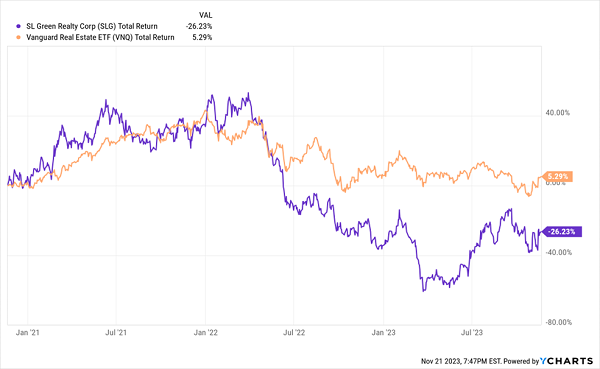

Sadly, it looks like SL Green was just late to the game. It pared its payout by about 13% at the end of 2022—and while that actually provided a tailwind, as SLG cut the dividend to improve liquidity and pay off more debt, that tailwind was brief.

SLG Shares Had More Bottom to Discover

SLG has bounced back somewhat amid more aggressive moves by American corporations to drag their employees back into the office. But fundamentally, it’s still coming up short—the company recently announced it probably would come short of the 92%-plus occupancy target it set for 2023 last year.

If there’s a sunny side to SL Green right now, it’s the value proposition. Shares yield nearly 10% at current levels, and they trade lean, at less than 6 times next year’s FFO estimates.

Brandywine Realty Trust (BDN, 14.9% yield)—which has an odd geographical footprint that includes Philadelphia, the greater Washington, D.C., area, and Austin, Texas—deals in office buildings, too, but that’s less than a quarter of its property mix. Residential makes up the largest chunk, at 42%, followed by life science at 27%; the remaining 9% is scattered across other property types.

Brandywine gets very little love from the analyst set—earlier this year, I highlighted it as one of the most hated stocks on Wall Street, and the pros have only slightly warmed up on the name since then. Interest rates have hit hard, sure, but so has lower occupancy. It probably won’t get much better in 2024, either, with estimates coming in below 2023 projections.

BDN has been among the worst REITs of 2023, losing roughly a third of its value. Not helping matters was a somewhat unexpected dividend cut. While Brandywine’s payout coverage was clearly tight, management was convinced earlier this year that it could keep financing its dividend at current levels—a stance they abandoned in September when they cut the distribution by 21% to shore up liquidity.

If there’s any reason to like Brandywine now (in addition to the hope of stable to lower interest rates), it’s a dirt-cheap valuation. Not only does BDN still yield 15% even after its payout reduction, but it trades at less than 4 times next year’s FFO estimates.

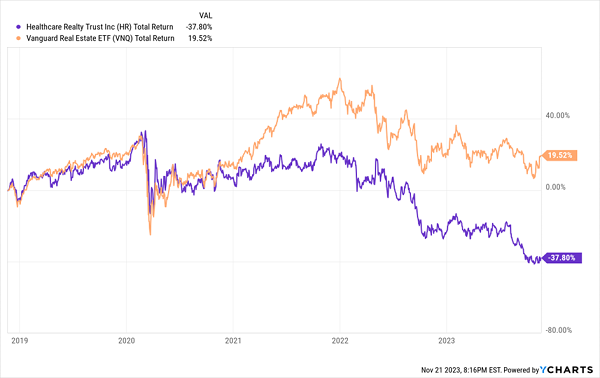

Healthcare Realty Trust (HR, 8.7% yield) owns and operates medical outpatient buildings, typically located around hospital campuses. It owns more than 700 properties totaling over 40 million square feet, most of which are concentrated in 15 growth markets—much larger than it used to be, by virtue of its recently closed merger with Healthcare Trust of America.

You might think that medical offices would be an, ahem, healthy business, but HR is one of the rare REITs that was gashed by COVID—and has just kept on bleeding ever since.

No Recovery for HR

HR’s struggles are myriad. Past its own difficulties with rising interest rates, COVID depressed elective and non-emergency procedures, which are critical to Healthcare Realty’s tenants. Also, very few (read: 6%) of HR’s leases have inflation-based escalators, which has severely cramped the REIT’s ability to roll through rocketing consumer prices.

Healthcare Realty is predicting a significant ramp-up in occupancy (from 85.1% currently to 87% in 2H24). But you could probably find better recovery opportunities to wait for. While HR does deliver a delicious yield of nearly 9%, you’re not getting a screaming value here—shares trade at roughly 11 times next year’s AFFO estimates.

Global Medical REIT (GMRE, 8.6% yield) is an owner of off-campus medical office and post-acute, in-patient medical facilities. It currently owns 185 buildings representing 4.7 million leasable square feet to 268 tenants.

While GMRE has performed much better than HR since the start of 2020—the former is roughly breakeven and on par with the sector, the latter has lost nearly half its value—it has come in roller-coaster fashion. It bottomed out in late 2022 as one of its tenants, Pipeline Health System, entered Chapter 11 bankruptcy protection.

It has mildly rebounded since then, but I’m more encouraged by some of the moves it has made since then. For one, it has locked in much of its financing at roughly 4% interest rates for years into the future. It has also managed to divest properties at surprisingly low cap rates given the current rate environment.

Shares still have a little value left, at about 10 times AFFO. A noteworthy red flag here, though, is dividend coverage. Its 21-cent-per-share dividend is a little more than 2023 AFFO projections. That pressure should ease—GMRE is expected to grow AFFO in each of the next two years. But any hurdles to its growth case could put its dividend squarely in skeptics’ crosshairs.

I’m Going to Retire on Dividends Alone—And You Can, Too

The “4% rule” is dead.

Don’t believe me. Believe William Bengen, the MIT grad who developed the 4% rule nearly three decades ago!

Bengen isn’t exactly on Easy Street these days. In fact, nine years into retirement he conceded to the Wall Street Journal that he’s “not comfortable.” (In fact, he said he’s cutting back on restaurants!)

My advice to you, and Billy for that matter, is to ditch that 50/50 blend of stocks and bonds and get creative—just like we’re doing in my massive-yielding “No Withdrawal” portfolio.

We don’t limit ourselves to a bland mix of conventional stocks and bonds. We look for opportunities in a wide variety of investments that are under-covered and overlooked—despite massive yields on stocks and funds of 8%, 9%, even 10%-plus. In fact, the top 10 payers in our live portfolio are yielding 11.8%!

That’s $118,000 in yearly dividend income on a million-dollar nest egg!

With that much income, you won’t have to touch a nickel in your retirement account. Just sit back, relax, and routinely keep your eye on the mailbox for when your fat dividend checks arrive.

Don’t let your retirement plan fall short as soon as you’ve crossed the finish line. Click here to learn more about my No Withdrawal portfolio!

Recent Comments