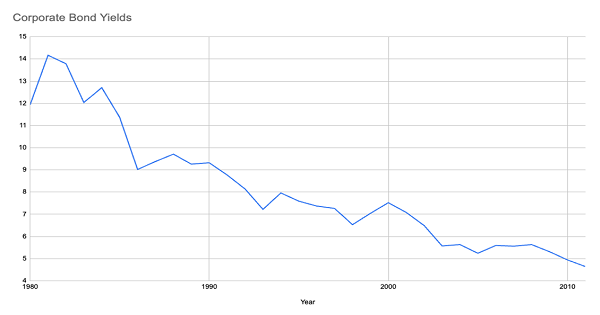

It’s back to the 1980s in the corporate-bond world—with yields through the roof. (I’m talking safe 9.9%+ payouts when we buy bonds through high-yielding funds like the one we’ll delve into below.)

If you were investing back then, you may recall that bond yields soared well into double-digit territory before falling back to earth:

Source: Economic Report of the President (2012), Government Printing Office

In other words, if you bought a corporate-bond fund in 1981, you’d have gotten a 14.2% return every year for the bonds’ duration, which in some cases was a decade. And you’d have gotten that return in cash.

Okay, so maybe I’m exaggerating a little bit here: yields aren’t quite that high today, but they are still pretty great for income-seekers like us. And better still, we have a lot more time to lock them in than folks did 40 years ago.

Yields Peak—and Plateau

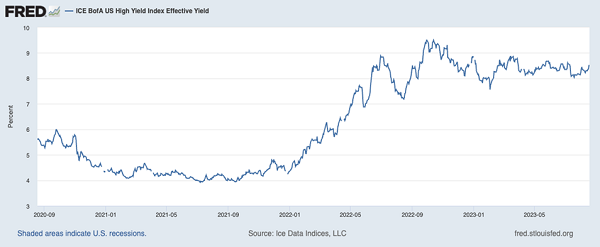

Because of the Fed’s higher interest rates, we’ve seen yields skyrocket to their current level of 8.5%. And unlike in the 1980s, those yields are sticking around. So the same principle applies: get the right bonds, hold them for a long time and you’re getting 8.5% in cash as a passive income stream until they mature.

And since bondholders are made whole at the end of the bond holding period, your invested capital is paid in full, too. But before we go further, let’s take a quick side trip to talk about the elephant in the room: bond-default risk.

To be sure, this is a real risk, but it is often misunderstood. To explain, let’s cut through the noise and look at how many defaults there really are: in 2022, the corporate-bond market saw 32 defaults. To put that in context, the corporate-bond market is massive, issuing over $1 trillion a year.

With so many bonds out there, it’s no surprise that defaults aren’t really as big of a deal as people make them out to be, especially if you buy a bond-focused closed-end fund (CEF) instead of an individual bond. That way we’re “outsourcing” our bond picks to a pro who knows how to steer clear of companies like the 32 that defaulted last year.

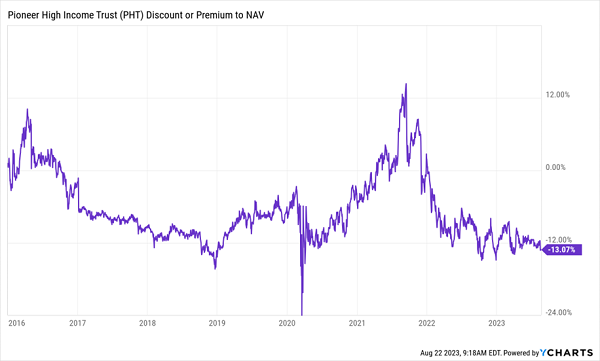

Consider, for example, a CEF called the Pioneer High Income Fund (PHT), which yields 9.9% and sports a 13% discount to net asset value (NAV, or the value of the bonds in its portfolio). These discounts only exist with CEFs, and PHT’s has been growing:

PHT Is Cheap—and Getting Cheaper

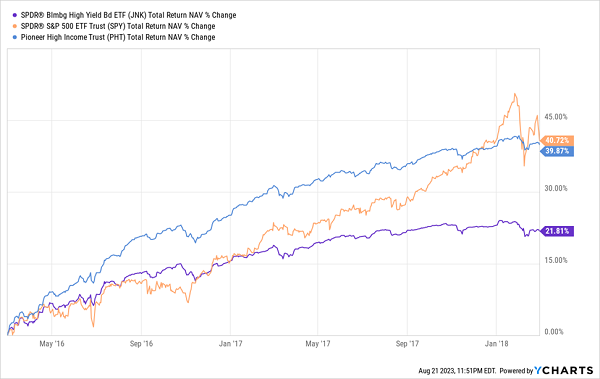

PHT has seen its discount slowly widen since the start of 2016, the last time bond yields peaked because the Fed was raising interest rates. This doesn’t make sense, given PHT’s strong performance since then, returning 57%, compared to a 37% return for the benchmark SPDR Bloomberg High Yield Bond ETF (JNK).

And if we zero in on the fund’s performance in the first two years of the Fed’s last rate-hike cycle, we see that it trounced JNK and nearly matched the performance of the S&P 500—a big move for a bond fund!

PHT Soared in the Last Rising-Rate Period

What’s more, all of PHT’s return came in the form of a 9.9% annualized yield during that two-year period. Bear in mind also that PHT had a brief window back then to buy bonds when yields were exceptionally high; yields peaked at 10% for a few days and fell back down to 6.5% in half a year.

In other words, there were only so many bonds PHT could buy in that brief window to boost its dividend. Today, though, corporate bonds have hovered at an average 8.2% yield for over a year.

More Time to Buy Big Yielders

That means PHT has had a lot of time already to buy bigger yields to sustain payouts, and its managers have even more time, since the Fed isn’t looking to cut rates anytime soon.

In 2016, savvy traders anticipated this opportunity and priced PHT up to a big premium as rates rose. But the opposite is happening today: corporate-bond yields have stayed higher for longer, and PHT’s discount has gotten bigger.

This makes no sense. PHT now has an easy time getting higher-yielding bonds to sustain its 9.9% dividend yield. And because it trades at a 13.1% discount to NAV, it only needs to earn an 8.6% return on its portfolio to sustain payouts (as the yield that really matters in terms of sustainability is calculated based on the fund’s NAV, not the discounted market price).

With the average yield on corporate bonds at 8.5%. It’s gotten very easy for PHT to maintain its dividend, and instead of pricing this fund at a premium, its discount is getting wider!

Markets are supposed to be efficient, but the truth is, they aren’t always, especially in the small world of CEFs. These are the mispricings we live to take advantage of in CEF Insider, and if you buy a bond fund like PHT today, you’ll do so before the discounts on these CEFs disappear, pulling their prices higher as they do.

My Top 2 Bond CEFs Are Cheap and Yield 9.5%+ (With Dividends Paid Monthly)

My top 2 bond CEFs to buy now sport huge 9.5% and 10.7% payouts, respectively, and they both pay dividends monthly!

They’re in a Special Report I’ve assembled that gives you a unique “mini-portfolio” of CEFs yielding 9.1% on average. In addition to these two stout bond-holding “battleship funds,” you also get details on two more CEFs holding the best blue chip stocks, including Visa (V), Coca-Cola (KO) and Amazon (AMZN).

Taken together, this quartet gives you an instantly diversified bond-stock setup that’s perfect for the “rate-topping” market we’re in now.

Plus, all 4 of these income plays are cheap today—so much so that I’m calling for 20%+ price upside from them in the next year.

Recent Comments