Let’s talk income investments that are usually reserved for rich folks: deal-making private-equity (PE) funds!

Usually there’s a sizable fee to get into PE. Unless you know the secret knock at the back-door entrance, which is more our style anyway.

I’m talking about yields from 7% all the way up to 11%. With a cover charge as low as $15!

These business development companies (BDCs) exist thanks to a perfectly legal loophole that lets anyone with an IRA or brokerage account tap into not just one or two private-market companies, but dozens at a time. Instead of shelling out hundreds of thousands of dollars to hit a PE fund’s minimum buy-in, this access typically starts at about $15 to $20 per share.

And best of all? These PE-esque stocks routinely deliver high-single and even double-digit yields. In fact, the trio of BDCs I’m about to break down pay out between 7.7% and 11.1% at current prices.

BDCs are rare birds. The industry represents just a meager sliver of the market. Currently, we have only a few dozen BDCs that trade on the public markets, and even the largest among them are pretty puny compared to the financial media’s favorite blue-chip topics.

Granted, it’s a tough business! Business development companies provide small- and midsized companies with much-needed financing—financing that was so difficult to come by, decades ago, that Congress legislated BDCs into existence for just that purpose.

Congress built BDCs much like they built real estate investment trusts (REITs). They provided them with ample tax advantages—under the condition that they pay out at least 90% of their taxable income as dividends.

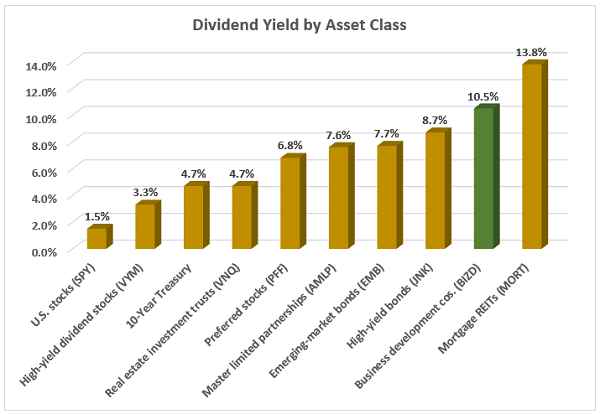

And if you thought REIT dividends were big, well:

BDCs Are Near the Top of the Payout Pile

That said, double-digit yields aren’t a “gimme” investment. Those big, regular checks sometimes come complete with big risks—so much so with BDCs that I refuse to own them through diversified funds.

The only way to buy BDCs is to pick the best and discard the rest.

Let me show you. Three BDCs yielding 7.7% to 11.1% have recently popped up on my radar—and they illustrate why some people loathe them, while others love them.

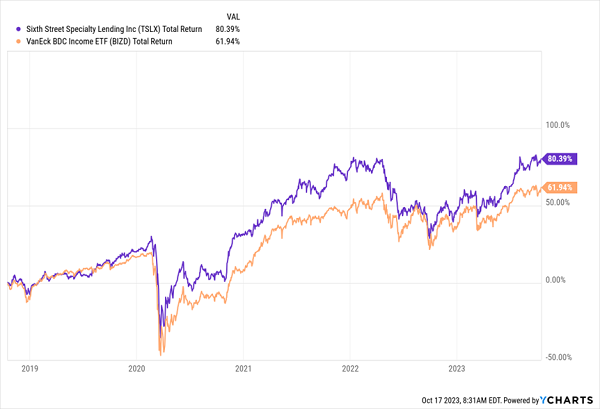

Sixth Street Specialty Lending (TSLX)

Dividend Yield: 10.2%

I want to start with Sixth Street Specialty Lending (TSLX)—a BDC that I frequently have my eye on because of its sterling dividend stewardship.

Sixth Street will do investments of all kinds—senior secured loans, mezzanine debt, non-control structured equity, common equity—in middle-market companies. A quick look at its typical deal:

- Transaction size: $15 million-$350 million

- Company size: $50 million-$1 billion (Enterprise Value)

- EBITDA: $10 million-$250 million

That capital can go toward all sorts of goals, whether that’s organic growth, acquisitions, restructuring, or several other uses.

The resulting portfolio of 94 companies is pretty eclectic. You have growth names like human resources support services firm PrimePay and integration and automation specialist Boomi, to pharma-royalty plays like BioHaven and Nektar, to even challenged retailers like Neiman Marcus and Aeropostale.

TSLX, whose investments are largely floating-rate in nature, was positioned well for a post-COVID recovery, as it could benefit from rising short-term rates.

Sixth Street Has Been a Standout in the BDC Biz

That strength isn’t as prominent as we near a potential peak in rates, but TSLX remains well-managed—both from a portfolio perspective, and from an income-management perspective. Rather than many BDCs that overextend themselves to pay out massive dividends, TSLX pays a core dividend, then distributes 50% of net investment income (NII) in excess of that core dividend as supplemental payouts. Of Sixth Street’s 10.2% annualized forward-looking yield, about 9 percentage points are from the core—the rest is from the supplementals.

The trouble with TSLX is its valuation. It’s perpetually overpriced and is one of the five most expensive BDCs by price to NAV right now, currently trading at a whopping 21% premium. That’s a little too dear.

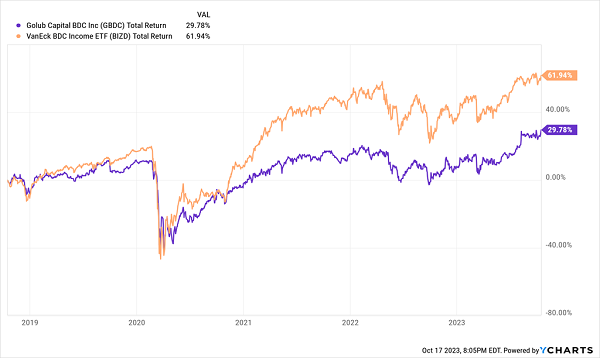

Golub Capital BDC (GBDC)

Dividend Yield: 11.1%

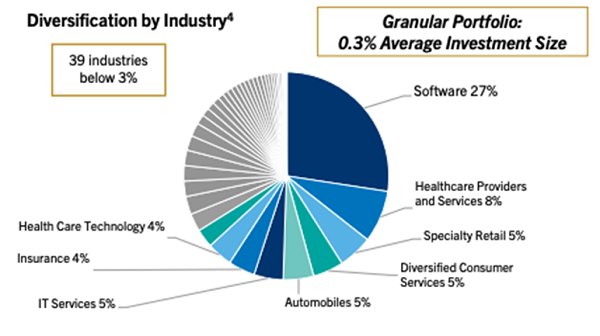

Golub Capital (GBDC) provides a number of financing solutions (largely debt and minority equity investments) primarily to companies backed by private equity sponsors.

Golub Capital is a well-diversified BDC, spanning dozens of industries. It’s lopsided in a few, such as software (27%), but all other industries—including healthcare providers and services, specialty retail, automobiles and more—are in single digits.

Source: Golub Capital BDC Investor Presentation, Quarter Ended 9/30/23

The vast majority of its loans are first lien: 85% “one-stop” loans, and another 9% traditional senior debt. Another 5% are equity, with a 1% splash of junior debt. And of that debt, 100% is floating-rate—again, helpful during rising-rate environments, but perhaps not as ideal should rates turn tail.

That’s a legitimate worry given that GBDC has underperformed for quite some time.

Even a Floating-Rate Edge Hasn’t Mattered

So, what could help GBDC close the gap?

Golub Capital has maintained strong credit quality across the portfolio for some time. However, a few recent moves have me a little more optimistic.

For one, GBDC recently raised its dividend by 12% to 37 cents per quarter—the latest in a short string of hikes. But GBDC is also instituting a supplemental dividend program similar to TSLX, where 50% of quarterly NII above the dividend will go toward top-up payments. (GBDC’s current annualized forward yield breakdown is 10 percentage points from the regular dividend, 1.1 points from the special at current levels.)

Also, in August, Golub announced a “shareholder-aligned” permanent fee reduction that will see GBDC pay its investment adviser 1.0% annually, down from 1.375% annually. The company estimates the move will raise adjusted NII by 10 cents per share each year. (For comparison’s sake, analysts expect the company to make 47 cents per share in the current quarter.)

This could bode well for GBDC shares, which trade at a whisper of a discount to their NAV.

Main Street Capital (MAIN)

Dividend Yield: 7.7%

Main Street Capital (MAIN) is arguably the “blue chip” of the BDC space.

This $3.3 billion business development company provides debt and equity capital solutions to lower-middle-market companies, and debt financing (primarily floating-rate first lien senior secured debt) to middle-market firms.

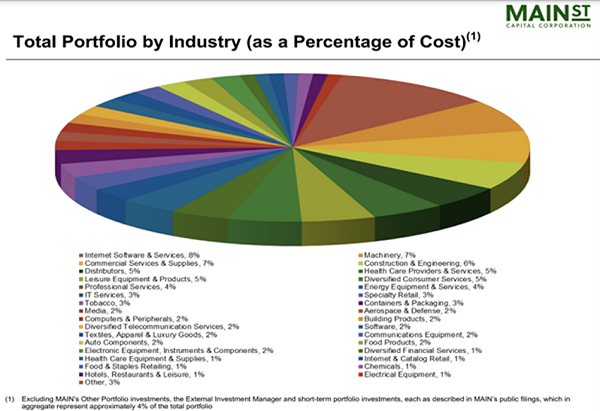

MAIN’s typical target company generates annual revenues of between $10 million and $150 million, and roughly $3 million to $20 million in EBITDA. Currently, its portfolio is made up of 195 companies, with the largest one representing just 4.0% of total investment income. And MAIN is the most diversified of the three BDCs covered here:

Source: Main Street Capital Q2 2023 investor presentation

Included in these companies is MSC Adviser—the company’s external investment advisor, which has been steadily contributing more to the BDC’s results over the past few years.

Main Street is a monthly dividend payer, but it also puts special distributions to use as income allows. It has only paid one in 2023—but at 27.5 cents per share, that’s another 70 basis points on top of a 7% base yield.

While MAIN is a best-in-class operator, it’s worth pointing out that as of its most recent quarter, it had 10 investments on non-accrual. However, that was down from 12 in the quarter prior, and those 10 only represented about 2% of cost.

No, the real complaint about MAIN is a common one—one that frequently keeps me at arm’s length. Main Street is perpetually overvalued, which has kept the stock’s performance subdued in recent years.

MAIN’s High Price Has Caught Up With It

At current prices, MAIN shares are trading at a whopping 45% premium to NAV!

Give Me 4 Minutes, I’ll 4X Your Retirement Income

While MAIN and the other business development companies boast sky-high yields, they’re low on value, and their floating-rate-heavy businesses make them wait-and-see stocks—nothing we can invest in with any conviction right now.

That’s not a problem with the stocks in my “Perfect Income” portfolio, which are safe harbors in any storm.

The perfect dividend retirement stocks have several things in common:

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Recent Comments