To paraphrase the great Jerry Maguire:

Show me the money. Monthly!

I don’t know about you, but my bills come every 30 days. So, I demand the same from my dividends.

Monthly dividend payers are a “must have” in retirement. After all, who has the time to track down a quarterly payment? Afternoons are for craft cocktails, not accounting.

(My buddy makes a dangerously tasty absinthe old fashioned. Would wait until after sundown on that one.)

Speaking of bitters, that’s life as a quarterly dividend receiver (sorry, couldn’t resist). Monthly payouts are magical, and not just for passive income. These income vehicles also hold three core advantages against all other stocks and funds that pay less frequently:

- Better overall returns thanks to compounding: If all else (performance and yield) is equal, a monthly dividend stock, with dividends reinvested, will always return just a little more over time than stocks that pay quarterly, semiannually or annually because you can put your cash to work sooner, which means it can compound faster.

- Generally higher yields. There’s no rule saying that monthly dividend payers have to have high yields, or that high yielders have to pay monthly. But weirdly, there’s definitely some correlation. Monthly payers tend to be found in clusters among the market’s highest-yield investments: BDCs, mREITs, CEFs. Among all dividend stocks, high-single- and double-digit yields are relatively rare. Among monthly payers? Not so much.

- The perfect match for retirement expenses. Have you ever heard of a “dividend calendar”? Your financial advisor might have suggested you build one. It’s when you buy certain stocks based on when they pay their quarterly dividends—that way, you have a relatively steady stream of income throughout retirement. The problem, of course, is what happens to that stream when one of those stocks cuts its payout or you simply want to cut bait. Suddenly, those payouts become pretty lumpy—a big problem when your bills still come in at the same amount the same time each month. Monthly dividend stocks, on the other hand, allow you to build a smooth, predictable source of income that’s practically like a salary in retirement—a pace of pay that perfectly matches your monthly obligations:

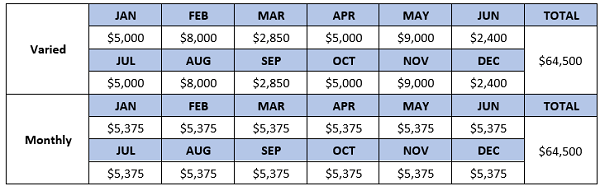

Just consider these two high-yielding portfolios—one with a range of payout schedules, and one built from sturdy monthly payers:

It’s not even a contest, is it?

Now, we can’t just go out and pick any monthly dividend payer and hope for the best. Research still matters. We still want value pricing, and most importantly, we want dividends that can last—after all, what good is a giant yield (monthly or otherwise) if the checks suddenly stop coming in the mail?

Today, I’m going to show you five monthly dividends averaging a juicy 11.4%—a wild six times more than the broader market. Let’s see which ones make the cut.

EPR Properties (EPR)

Dividend Yield: 7.9%

Let’s start out with something fun.

EPR Properties (EPR) is one of the most entertaining real estate investment trusts (REITs) you’ll find. Its nearly 360 locations, leased out to more than 200 tenants across 44 states and Canada, include AMC (AMC) theaters, Topgolf driving ranges, ski resorts, waterparks, even museums.

It’s one of the biggest names in the “experience economy”—a growing trend I’ve written about for years in which people have shied away from things and stuff, and gravitated toward building memories.

Now, while the trend is EPR’s friend, the stock isn’t without its problems. The COVID pandemic was sheer misery for EPR, choking its theater-heavy business and forcing the REIT to temporarily suspend its monthly dividend in 2020. It resumed payments in 2021, albeit 35% lower at 25 cents per share, though it has bumped that payout a little higher since then, to the current 27.5 cents.

Those woes aren’t over, either. Regal Cinemas parent Cineworld filed for Chapter 11 bankruptcy protection in early September, which was met with a wave of profit-estimate downgrades from analysts assuming this will be met with rent reductions.

Still, I tend to agree with our own senior investment analyst, Jeff Reeves, about the continued appeal of EPR as people increasingly scratch a longstanding itch to get back outside and experience the world. I would just suggest retirement investors be realistic about what they’re getting here: an extremely cyclical monthly dividend payer that’s reliant on economic growth—great in boom times, but one that’ll require patience during busts.

A nearly 8% yield, paid monthly, does provide a lot of cushion, though.

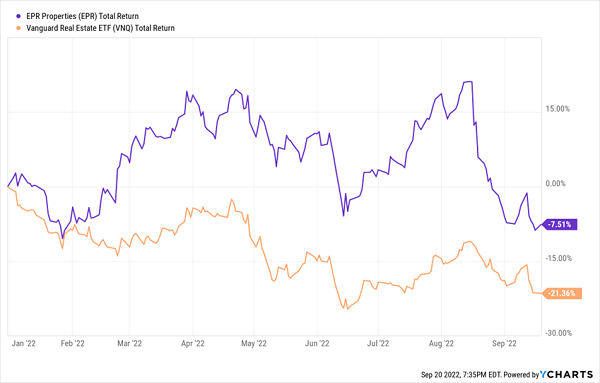

EPR: Outdoing the Market in 2022, But More Volatile, Too

Templeton Global Income Fund (GIM)

Dividend Yield: 8.5%

If water slides and golf games are a little too much excitement for you, consider the yawner of an 8%-plus yield that is Templeton Global Income Fund (GIM).

I joked earlier this year that the safest bond fund for 2022 is my mattress—I joked, but I wasn’t wrong. Stashing cash under my memory foam is killing just about every bond fund, and Templeton Global Income is no exception. Though, in GIM’s defense, it’s at least making a short-term argument for how active management and high yields can give CEFs an edge over plain-Jane index ETFs, down just 7% in 2022 versus 11% for a major global bond ETF.

So, what’s under the hood?

Templeton Global Income Fund invests in U.S. and international debt with a particular focus on high-income. That said, there are some notable differences between GIM and its benchmark.

For one, while “global” debt funds often feature a roughly 50/50 U.S./international split, Templeton’s CEF only has 14% of assets invested across all of North America. Asia is tops at 46%, with another 23% in Latin America/Caribbean, 9% in Europe and the rest sprinkled across the world.

Also, credit quality is drastically lower than your average global bond fund—just 44% of GIM’s holdings are A-rated or better vs. 100% for the benchmark. Another nearly 30% is in BBB (still investment-grade) bonds, and the remaining quarter or so is in junk debt. But, that’s far better portfolio credit quality than you’ll see in your average high-yield fund, and a slightly better yield, to boot.

It sounds nice in theory, but this in-between portfolio hasn’t delivered over the long term, despite its generous monthly dividend. And even if you were to bet on management turning things around, now’s not the moment in time—a skinflint 0.7% discount to net asset value (NAV) is perilously lower than its nearly 10% average discount over the past five years. That’s a serious hurdle to overcome.

Templeton Global Hasn’t Set the World on Fire

Gladstone Investment Corporation (GAIN)

Dividend Yield: 8.9%*

Next up is the biggest family name in high yield: Gladstone.

Gladstone Investment Corporation (GAIN) is just one of several public investment vehicles bearing the Gladstone name. There’s also Gladstone Commercial (GOOD), Gladstone Capital Corporation (GLAD) and Gladstone Land Corporation (LAND). As a group, they invest in (and buy) lower middle market companies, and deal in commercial and farmland real estate.

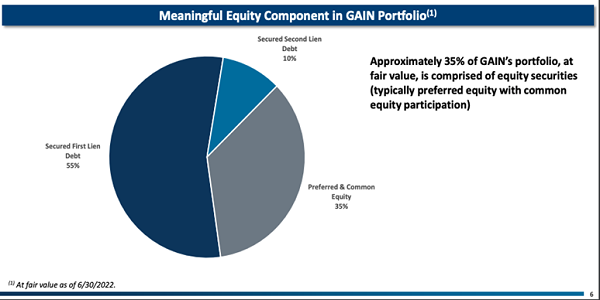

As for GAIN itself: This publicly traded business development company (BDC) provides both equity and debt capital in transactions, though it leans more toward the latter.

GAIN tends to invest up to $70 million, and focuses on companies with $3 million-$20 million in EBITDA, experienced management teams, predictable and stable cash flow, and minimal market or technology risk. Its portfolio is a mish-mash of companies ranging from golf car distributor Country Club Enterprises to school supply and teaching materials firm Educators Resource, to Mason West—a provider of engineered seismic restraint and vibration isolation products. (In other words, it helps with earthquake-proofing.)

While Gladstone Investment has had a difficult 2022, it’s hard not to love its overall structure in this environment: It targets to have 90% of loans at variable rates or variable rates with a floor mechanism—and currently 100% of its loans are at variable rates with a floor mechanism. Why does that matter? Variable-rate loans provide a lot more room for fatter profits when interest rates go up, and interest rates are going up.

Dividend coverage is a little tight. Regular payouts over the past 12 months have come to roughly 90% of net interest income (NII). Despite this, Gladstone continues to squeeze every last drop of dividends from its earnings, delivering three special dividends in that time—bringing its yield from 6.4% on just the monthlies to nearly 9% in total.

Armour Residential (ARR)

Dividend Yield: 18.3%

My kids know there are two house rules for 2022:

We don’t talk about Bruno, and we don’t buy mortgage REITs.

Rules have exceptions, of course, and I’m willing to at least investigate a little when a yield starts floating around the 20% mark.

Armour Residential (ARR) primarily invests in mortgage-backed securities (MBSs) issued or guaranteed by U.S. government-sponsored entities: think Fannie Mae, Freddie Mac or Ginnie Mae. Most of these “agency” securities are primarily fixed-rate loans (red flag), though some are hybrid or variable-rate. And, on occasion, ARR will invest in Treasuries, interest-only securities and even money-market instruments.

Armour has a couple of things going for it now. It’s in the midst of a favorable agency market. And it maintained its monthly dividend at 10 cents per share, saying that core EPS should be more than enough to cover the payout through the rest of the year.

… but, that latter point seems like an awfully low bar. Why is this so noteworthy?

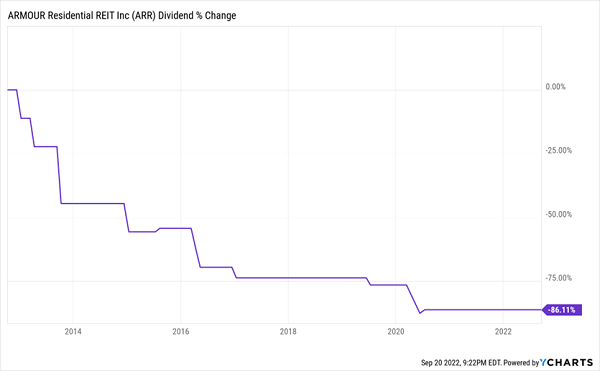

This Isn’t Armour’s Stock Price. This Is Its Dividend Over Time.

Could Armour management finally turn things around? Absolutely. But this is a horrid dividend track record that should give income investors zero confidence in what has historically been a siren’s song of a payout. That makes ARR the very definition of a “show me” stock.

For now? No, no, no.

Virtus Total Return Fund (ZTR)

Dividend Yield: 13.4%

Virtus Total Return Fund (ZTR) is effectively a “portfolio-in-a-can”—a fund that basically provides an entire investment portfolio, all by its lonesome.

The technical term here is “balanced,” with ZTR targeting a 60/40 blend of equities and fixed income.

As far as stocks go, the fund will invest globally in infrastructure owners and operators in communications, utilities, energy, real estate and industrials/transportation. Utilities are more than 40% of the fund right now, with another 30% or so in industrials.

The fixed-income portion of the portfolio is high-yield-focused, and management is happy to rotate in and out of sectors to wring value from the bond market. Right now, investors are getting a great blend of debt, with double-digit exposure to high-yield corporates, high-quality corporates, bank loans, non-agency residential MBSs, asset-backed securities (ABSs) and Treasuries.

And management, to their credit, is doing its job.

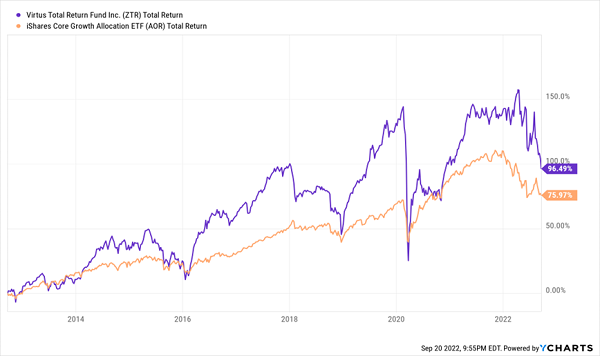

ZTR Is Crushing an Indexed Balanced Competitor

Better still is that ZTR is trading at a 10% discount to NAV right now that’s a huge value compared to its more modest 2% long-term average.

My only warning? My oh my, beware those swings.

It’s one thing to take a couple of moonshots with a little bit of money in a well-diversified portfolio. But you don’t want your retirement to hinge on a fund whose chart looks like a Six Flags attraction.

The Ultimate Playbook for Retirement Riches: 7%+ Yields, Delivered EVERY MONTH

When you retire, you need peace of mind.

You need portfolio stability.

And most importantly, you need to know beyond a shadow of a doubt that a sizable dividend check is hitting your mailbox each and every month—no exceptions.

That means you need the “A” squad: diversified, reliable payers of mouth-watering yet dependable income that don’t knuckle under every time the economy throws a fit.

Fortunately, you can find these rare monthly dividend blue chips in my “7% Monthly Payer Portfolio.”

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate massive yields, while also fostering the potential to generate aggressive price performance.

These dividends aren’t just good. They’re not just great, either. They’re life-changing sums of income.

It’s simple math: Even if you have just a $500,000 nest egg—which is less than half of what most financial gurus suggest you need to retire—putting it to work in this powerful portfolio now could kick-start a $35,000 annual income stream.

That’s nearly $3,000 a month in regular income checks!

Even better? The market’s recent antics have provided us with a rare gift, pulling all of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments