Worried the economy is teetering on the brink? I don’t blame you.

Rather than running for the hills, let’s focus on recession-resistant dividend stocks. Big payout growers. We’re talking 25% to 56% dividend growth (yes, that’s no typo).

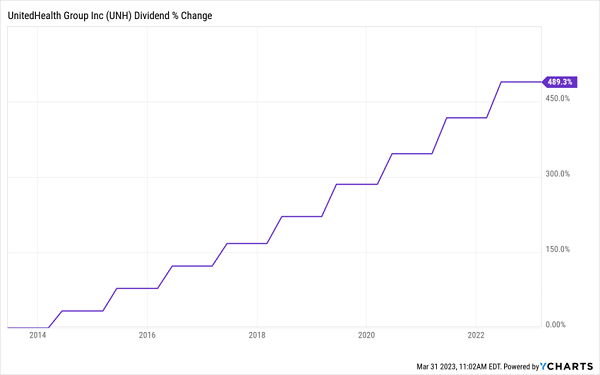

The safest dividend is the one growing the fastest. Take UnitedHealth Group (UNH), the largest health insurance carrier in the US. Its business is beautifully recession resistant. As a result, UNH is one of the most consistent growth stocks out there. Mark it down for 10%+ gains, per year, every year.

Gains in what? Every metric that matters. UNH’s sales soared 13% year-over-year.… Read more

Recent Comments