I hate to see folks trying to time this banking mess with regular stocks like JPMorgan Chase & Co. (JPM). Especially when they can easily swap their big-bank stocks for “preferred” dividends yielding 8% and up!

That’s a far sight better than the magic trick mainstream investors are attempting, as they try to dodge into big banks like JPM at just the right moment.

JPM Looks for a Bottom

Worse, JPM only yields 3% today. And you and I both know that markets can thrash around for weeks looking for a bottom.

That’s why, instead of squinting at price charts, we’re calmly picking up some sweet “backdoor” dividends from these very same banks, but with a yield that’s 173% bigger.

We’re doing it through preferred shares, which are part stock, part bond and all dividends. And because banks issue most preferreds, they’re the contrarian’s choice for profiting from this mess.

Cool thing is, you likely won’t even have to switch investments to buy them. Own JPM “common” shares but want to double your dividend? No problem. Trade them for JPM’s Series Y preferreds and you’ve got a nice 6.125% payout rolling in.

Voila.

Plus, preferred shareholders are typically paid before “regular” stock and bond holders. That’s a nice plus in a bank panic–stricken economy like this one. (Not that we think JPM, which has been around in one form or another almost as long as America itself, is going anywhere!)

Trouble is, even folks who know about preferreds often blow their opportunity right off the bat by buying them through an ETF like the iShares Preferred & Income Securities ETF (PFF).

Sure, you’ll get a 6% payout … but you’ll also “bake in” ho-hum performance. That’s because personal connections between fund managers and preferred-stock issuers matter when it comes to getting the best new preferreds. As a result, actively managed funds almost always top “robotic” ETFs here.

This is why we go one floor up from the ETF crowd and join the closed-end fund (CEF) party. CEFs boast even bigger yields than PFF, and most pay monthly.

Plus, CEFs, unlike ETFs, tend to have fixed share counts for their entire lives, so they can trade at different levels than their net asset values (NAV, or value of their underlying portfolios)—and usually at a discount.

An 8.2%-Yielder With “Discount-Driven” Upside

These discounts are the key to our gains, as we’ll see with our “backdoor” bank play: the Flaherty & Crumrine Preferred Securities Income Fund (FFC).

This one is as tilted toward the finance sector as they come: about 56% of its portfolio comes from banks, with another 22% from insurance companies.

That’s a nice mix, as insurers invest their float—or the premiums customers pay—in safe fixed-income securities. But they don’t have the same liquidity issues some banks can run across if customers decide to withdraw all at once.

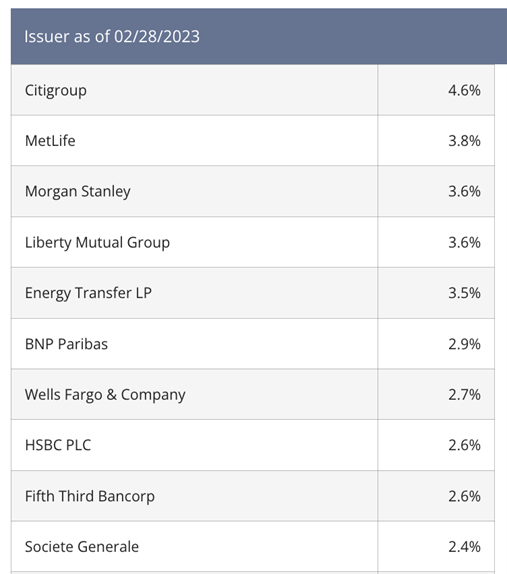

FFC hedges us from that risk in another way, too, with preferreds from big players like Citigroup (C), Wells Fargo & Co. (WFC) and Morgan Stanley (MS) making up the bulk of the bank issues in its top-10 holdings:

Source: Flaherty & Crumrine

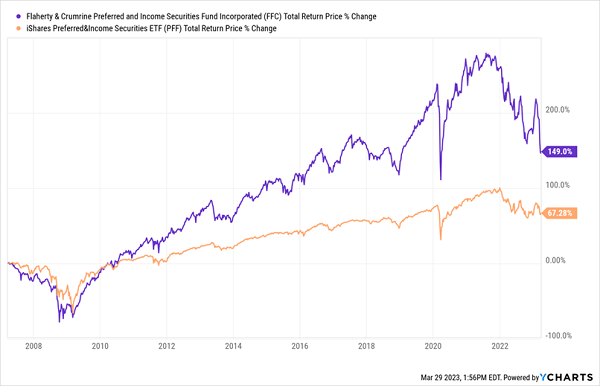

A benchmark beater? You bet. FFC has more than doubled PFF since the ETF launched in ’07 (FFC itself is more than 20 years old, so it’s got lots of history):

FFC Blows Past Its Benchmark

Now let’s talk payouts: as I write this, FFC yields 8.2%, much more than PFF. The fund has reduced its monthly payout over the last year, from $0.124 a share to $0.093 today, but that’s to be expected after the across-the-board tire fire that all assets (including preferreds) suffered.

Plus those cuts come with a bright silver lining: they’ve freed management to go after bargain-priced preferreds, setting us up for gains. And I don’t know about you, but I’m more than happy to give up a bit of income for upside—especially when we’re still getting an 8.2% payout!

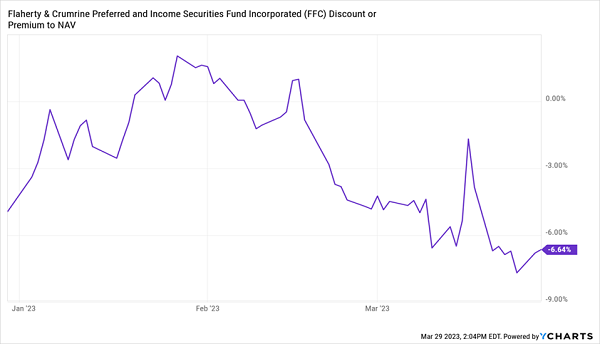

In fact, we can expect some of that upside from the closing discount: thanks to the bank panic, FFC’s discount is now 6.6%, well below its five-year average of 2.25% and miles below the premiums it was booking just six weeks ago.

A Buy-the-Dip Opportunity We Don’t Have to Time

And while we can expect this banking drama to play out for months, with potentially more downside to come, our CEF discounts do help us mitigate that risk while we collect our rich payouts.

The capper is that Flaherty & Crumrine knows the preferred game and is right at home bargain-hunting skittish markets like this one: the company has been in CEFs (and preferreds) since its founding in 1983. And FFC’s manager, Bradford Stone, has been with the firm since FFC rolled off the line 20 years ago.

This Breakthrough Portfolio Could Let You Retire on $500K

CEFs like FFC are the key to what we all (perhaps secretly!) know we should be aiming for: a retirement on dividends alone. Think about it for a moment: going “dividends only” is the only way to clock out without having to worry about selling stocks into a downturn like the 2022 disaster.

But preferred stocks aren’t enough on their own—we need a complete bargain-priced CEF portfolio diversified across the economy, holding top-quality bonds, real estate investment trusts (REITs), blue chip stocks and, yes, preferreds.

That way we get an extra layer of safety so we can enjoy our CEFs’ 8%+ yields in peace. And thanks to those same high CEF yields, we could put our “dividends only” retirement plan in motion with as little as $500K.

I’ve put everything you need to know in 2 Special Reports I’d like to share with you now. Click here and I’ll explain my “dividends-only” retirement plan and show you how to download those 2 reports—including the names of specific stocks and funds (with yields up to 11%!) you need to make it happen.

Recent Comments