Let’s work this market pullback to grab ourselves a sweet 21% “double discount” on our favorite stocks. We’ll also get a dividend from blue chip firms that don’t even pay one!

The key is an off-the-radar closed-end fund (CEF) holding some of the biggest names on the market and trading at a totally undeserved 17% below its true value. And this one pays a rock-steady 3.1% dividend, too—double what the typical S&P 500 stock yields!

Before we put a name and ticker to this fund, let’s talk about the first part of the 21% double discount we’re going to tap today.

Double Discount Part 1: Mr. Market’s “Flash” 4%-Off Deal

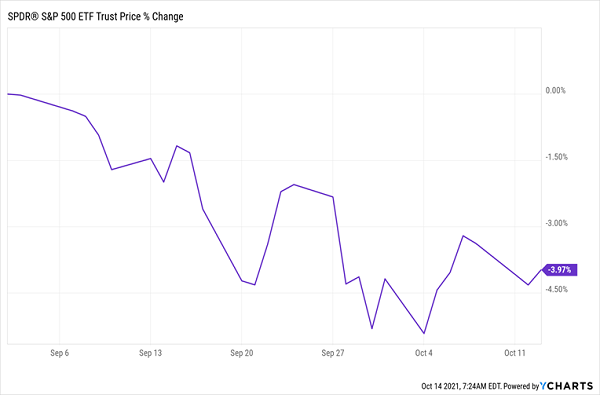

The first part of our discount is the pullback we’ve seen in the S&P 500 since early September: from the highs it hit back then, it’s slid about 4% as of this writing:

Stocks Slide—and Give Us Part 1 of Our Double Discount

I know many folks are concerned about this slide, but history is not on the worrywarts’ side here. Every dip we’ve seen in the last year has been a buying opportunity—and this one is shaping up the same way:

Imagine Buying These Dips (the Last One Is Our Chance)

The several dips we’ve seen in the last year have been chances to buy at a “flash” discount to profit from long-term strength in the economy. And with America’s GDP forecast to grow 5.6% in 2021 and a still-strong 4% in 2022, there’s still a lot of growth on the way. This latest dip has nicely set us up to cash in on bearish investors’ wrongheaded take on that fact.

What’s more, the issues affecting the global economy (stemming mainly from supply-chain bottlenecks) pale in comparison to what we faced during last year’s dips, when vaccines were a distant fantasy. Yet the market bounced each time.

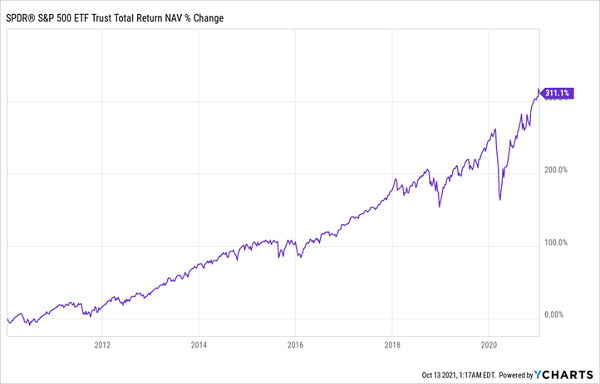

Finally, consider that the market’s big move up since the crash of March 2020 isn’t that far out of line with history. Look at the purple line below—sure, it’s arced higher, but the latest jump pretty much continues the pre-crisis trend, and those earlier gains came when growth was much lower than it is today.

Latest Gain Is Right on Trend

In the 10 years before the COVID-19 crash, stocks were up 13.4% annualized, and this latest gain has raised that figure just a bit more, to 13.7% annualized over the last 11 years. In other words, the market’s recent run higher has been a return to normal, not a bubble in the making.

Double Discount Part 2: A Buffett-Friendly Fund for 17% Off

Now let’s tack on the other 17% of our 21%-off deal with that CEF I touched on earlier. It’s called the Boulder Growth & Income Fund (BIF), and it holds US large caps (and favorites of one Warren E. Buffett) while paying us that 3.1% yield.

I say it’s a back-door way to get us a dividend on some non-dividend payers because a major holding is Berkshire Hathaway (BRK.A) itself. Buffett has said Berkshire would never pay a dividend as long as he’s in charge, as he prefers instead to reinvest in the company. But BIF lets us collect a dividend from Berkshire anyway, as its managers hand us some of its price gains from Berkshire (and the rest of BIF’s portfolio) as dividends.

BIF’s other holdings are similarly long-term focused large firms, such as JPMorgan Chase (JPM), Yum Brands (YUM) and Cisco Systems (CSCO), to name a few. BIF is also diversified across the economy, with its largest single sector being financial services, at 12.6% of the portfolio. Banks are nicely positioned for further gains, thanks to the rising yield on the 10-year Treasury note, benchmark for interest rates on loans and lines of credit.

The 17%-off deal on BIF comes from its discount to net asset value (NAV, or the value of its underlying portfolio). These discounts only exist in CEFs and stem from the fact that CEFs can’t issue new shares to new investors after their IPOs. With their share counts more or less fixed, their shares tend to swing above and below the per-share value of their portfolios—and most CEFs trade at discounts!

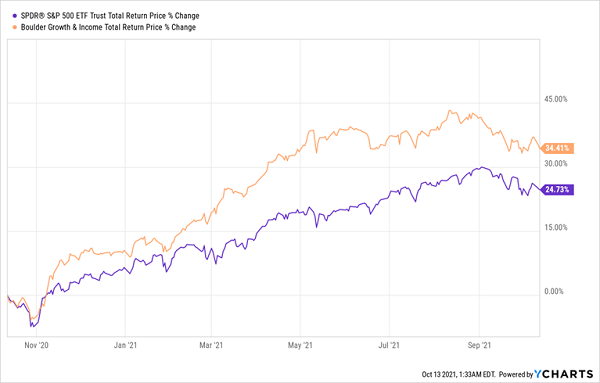

And don’t think this discount means you’re getting an inferior fund: BIF has handily beaten the market over the last year.

Investors Miss Out on BIF

Yet despite all this, BIF trades for 83 cents on the dollar. In other words, you’re getting Berkshire, JPMorgan, Berkshire, Cisco and the rest for less than you would if you bought these stocks individually.

When investors back up the truck and buy BIF, you can expect that 17% discount to shrink, increasing the value of your BIF shares in addition to the 4% gain you’d see as the market moves back to its September high.

Why Settle for a 3.1% Dividend When You Can Have a Safe 7.1% (With 20% Upside)?

BIF’s 3.1% dividend is big as regular stocks and ETFs go … but it’s actually tiny compared to what other CEFs pay. As I write this, CEFs yield 6.8%, on average, and many yield much more. And you don’t have to sacrifice upside to get these dividends, either.

That’s why I’m urging all investors to pick up my 5 top CEFs to buy today. These 5 low-key funds, which span the investment universe, from biotech stocks to AI plays, blue chips and corporate bonds, yield an outsized 7.1%, on average. Plus, my latest forecasts have them pegged for 20%+ price upside in the next 12 months, due to their unusual discounts to NAV.

Add your yield to your forecast price gains and you’re looking at a 27%+ total return here, by this time next year! Every $100K invested turns into $127K.

I’m ready to share everything I have on these 5 powerhouse funds with you now. Click here and I’ll give you their names, tickers, current yields, a full analysis of their managers and my complete research on each one.

Recent Comments