Goldman Sachs says the Fed will start cutting its bond purchases next month—and that sets up some of our favorite dividend-payers for a quick 61% profit surge. (I’ll reveal the tickers we need to reap this “taper bonanza” in a moment.)

Wait. Why are we taking Goldman’s word here?

Because “Government Sachs” has the deepest DC connections of any bank: former Treasury Secretaries Henry Paulson and Steven Mnuchin are Goldman grads, among many other government bigwigs. When it comes to what’s happening at the Fed, I’d take Goldman’s opinion over that of Jay Powell himself!

A Boon for Dividend Investors

To get at how we’ll flip the taper into big dividends, let’s connect it to a figure we all watch closely: the yield on the 10-year Treasury note.

Treasury yields are based on supply and demand. Supply (bond issuance) is huge, but so is demand, with the Fed stepping in for $80 billion per month. When this big buyer cuts back, we’ll see the yield on the 10-year rise to attract other buyers.

It’s already happening. At the beginning of 2021, the 10-year paid just 1%. It has since soared to 1.55%. That may not sound like much, but it’s a 55% increase.

As Powell throttles back, I expect Treasury yields to pop to between 2% and 3% in the first and second quarters of next year. The midpoint of that range is up 61% from now—fueling big profits in the sectors (and stocks) we’ll delve into next.

“61% Profit Play” No. 1: Regional Banks

Banks profit from the spread between the 10-year rate (benchmark for the loans they make to consumers) and the Fed’s overnight rate (at which banks lend to one another). The latter, of course, is set by the Fed and will likely stay at zero at least until mid-2022, going by the latest read of the Fed futures market.

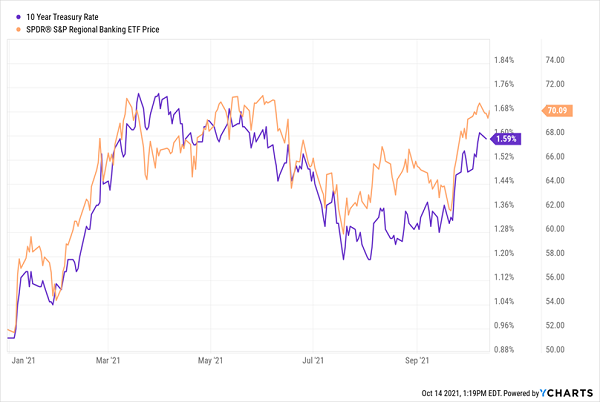

No corner of the banking world is more correlated to Treasury yields than regional banks. You can see that by the performance of the SPDR S&P Regional Banking ETF (KRE) below.

Treasuries Up, Small Banks Up

That brings us to our first “61% profit play,” KeyCorp. (KEY), with 1,000 branches in Ohio and New York. KEY starts us with a 3.3% yield, then doubles down with payout growth of 517% over the last decade. In other words, if you bought KeyCorp 10 years ago, you’d be yielding a hefty 9.4% now!

With the bank’s payout occupying just 35% of net income, it’s got plenty of room for further growth, and that’s before rate hikes further inflate its loan income. KEY’s bargain P/E ratio of 9.9 adds more upside.

“61% Profit Play” No. 2: Insurance Stocks

Insurers always play second fiddle to banks in investors’ minds, which is reflected in the SPDR S&P Insurance ETF (KIE), which badly lags the Financial Sector SPDR ETF (XLF) this year.

Insurers Trail, Our Opportunity Arrives

That’s too bad for them, because insurers are every bit as solid a rising-rate play as banks. They collect premiums from their customers and invest them in safe fixed-income securities until they have to pay them out (if they ever do!). So it follows that they’ll see higher profits as Treasury yields rise.

That’s part one of our opportunity. Part two comes when we target insurers trading for less than book value (or what their assets would be worth if they were sold off today). Buying stocks trading “below book” means we get their businesses for free!

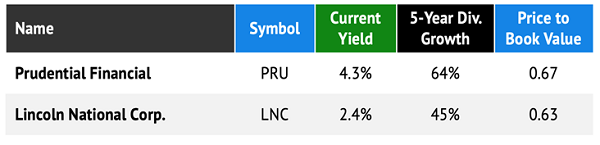

Right now, two leap out as stunning bargains: Prudential Financial (PRU) and Lincoln National (LNC):

Prudential: “Get a Piece of the Rock” for Nothing

You may remember Prudential Financial (PRU) for its 1970s slogan “Get a piece of the rock.” Today, that best describes PRU’s dividend: it’s the rare stock with a high current yield, at 4.2%, and fast dividend growth, too.

Despite PRU’s strong position as rates rise (and COVID-19 recedes, reducing life-insurance claims), we still have an opportunity because the stock “breaks” every valuation measure, trading at just 6-times earnings and 67% of book value.

Management knows a great deal when it sees one—it’s repurchased 10% of PRU’s stock in the last five years. Now is a good time to follow their lead.

Lincoln National: 2.3% Dividend Today, 9.1% Tomorrow

Life insurer Lincoln National (LNC) sports a lower yield than PRU, at 2.4%, but that’s just the start. Over the last decade, LNC’s payout has skyrocketed 425%, boosting the yield on a buy made then to 9.1% today.

Continued fast payout growth is likely as rising rates, fast economic growth and a greater focus on health post-COVID-19 drive policy origination—and profits. Silly valuations of 62% of book value and 9-times earnings add more upside.

Bonus Buy: A 7.5% Yield Treasuries Will Never Outshine

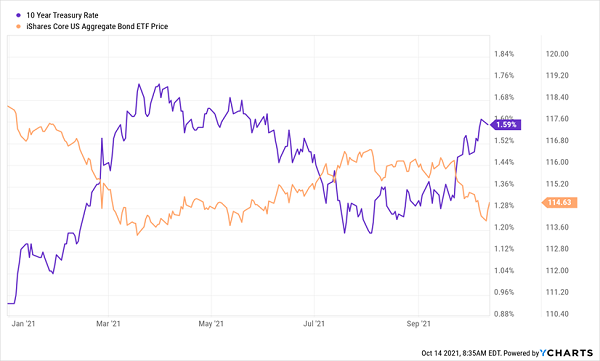

As rates rise, corporate bonds will get hurt because investment-grade issues will see rising competition from even safer Treasuries. You can see this happening as the iShares Core US Aggregate Bond ETF (AGG), unlike regional banks, moves in opposition to the yield on the 10-year:

10-Year Rises, Investment-Grade Paper Fades

The “Bond God” Laughs Off Rising Rates

This, by the way, is not bad news for corporate-bond-holding closed-end funds (CEFs), including the six in the portfolio of my Contrarian Income Report service (average yield: 7.8%).

Even if Treasury yields rise as high as 3%, they’ll never compete with a 7.4% yield like the one paid by the DoubleLine Income Solutions Fund (DSL). DSL holds 95% of its portfolio in bonds rated below BBB, which is the investment-grade cutoff. That’s where the best deals, and the highest coupon rates, live.

DSL also holds shorter-duration bonds, with half the portfolio maturing in three years or less. That makes it less rate-sensitive than funds holding longer-term bonds, which lose their appeal as new bonds are issued at higher rates.

Discount “Comps” Our Fees

The topper is that we can buy DSL, run by the “Bond God” himself, Jeffrey Gundlach, at a 2% discount to net asset value (NAV, or the value of the bonds in its portfolio).

Like stocks trading below book, these discounts give us a nice freebie: in this case, it’s Gundlach’s management expertise: as DSL’s discount mostly covers DSL’s 2.28% fee for interest (it employs a reasonable amount of leverage) and management, so we’re basically getting Gundlach’s expertise for free.

That’s a particularly sweet deal, given that Gundlach has already given us a 75% total return since we added DSL to our portfolio in 2016.

How We’ll Play Rising Rates for 7%+ Dividends—Paid Monthly

Big dividends like these—either “upfront,” like DSL’s 7.4% yield or built up over time through dividend growth (like KeyCorp’s astonishing 517% in payout hikes, resulting in a 9.4% payout today) are the keys to funding the retirement you want.

To those I’d add one other thing: dividends that come your way monthly.

That way, you’re getting payouts on a schedule that matches up with your bills. And if you’re reinvesting your dividends, even better—monthly payouts let you put your money to work faster, instead of having to wait a full quarter for your next dividend payout to roll in.

To help you build your monthly dividend stream, I’ve put together my “7% Monthly Payer Portfolio.” As the name states, it pays you 7%+ dividends that roll your way every single month. So a $500K investment would pay you a reliable $2,917, month in and month out.

Plus this unique portfolio is diversified across the economy, giving you the best corporate bonds, blue-chip stocks, real estate investment trusts, preferred stocks and even chameleon-like convertible bonds, which can transform from bonds to stocks to deliver maximum upside.

I’m ready to share the details on this retirement-changing portfolio with you now. Click here and I’ll give you a complete guided tour, revealing the names, tickers, current yields and other vital stats on every investment inside.

Recent Comments