It’s no secret that corporate bonds are booming. But what might come as a surprise to some folks is that we’re not too late to get in. Through a group of well-run closed-end funds (CEFs), we can still tap big corporate-bond yields at a discount.

Even perennially gloomy Business Insider (notorious for its overdone calls for an inflation/recession-driven crash in 2022) acknowledges the terrific environment for bonds right now. Recently, BI had to admit not only that “Corporate bonds are the safest they’ve been in years,” but that this is one of the best bond markets we’ve ever seen.

The demand for bonds has caused “inflows into US corporate bond funds to hit record levels,” BI notes, while the Financial Times states that investors “are shifting to a large extent from less risky products” and into corporate-bond funds.

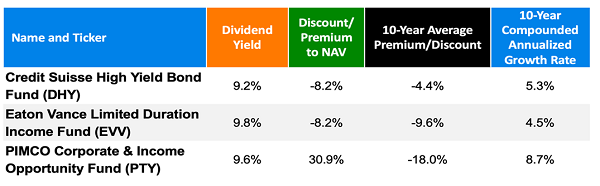

It’s easy to see why. Check out the yields on the following three corporate bond–focused CEFs:

These are just three of many bond CEFs with yields above 9%, and those yields are better covered by these three funds’ investments than they’ve been in a long time. Here’s why.

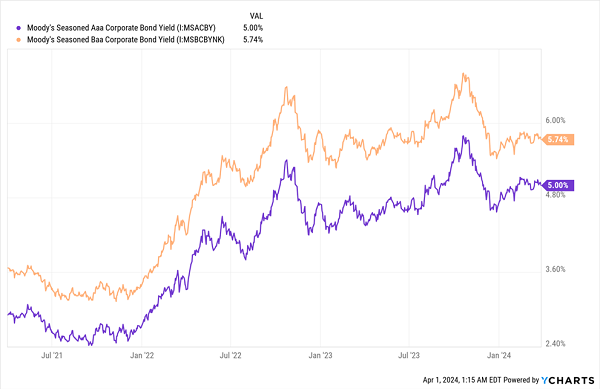

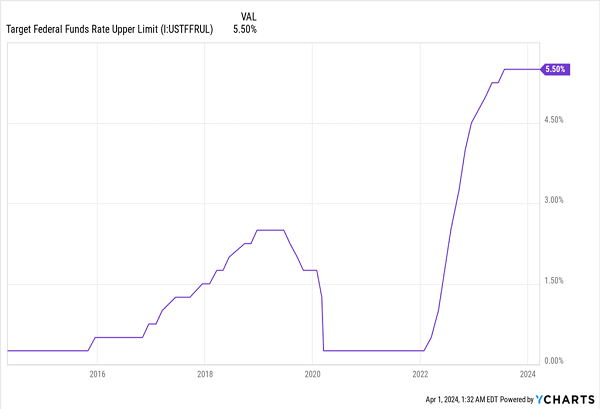

Corporate-Bond Yields Surge

Since the Fed started hiking rates, bond yields—shown here by the average yields on bonds rated Aaa and Baa by Moody’s—have soared. Bond yields usually go up when the risk of default rises, but defaults are still tame this time around.

Currently, private credit has a 0.3% default rate, and investment-grade corporate bonds have been around 0.5%. Low-rated corporate bonds are defaulting at a higher rate, around 4.2%, including the lowest-quality junk bonds, so a savvy bond-fund manager should be able to avoid those and produce a high-yielding portfolio with relative ease.

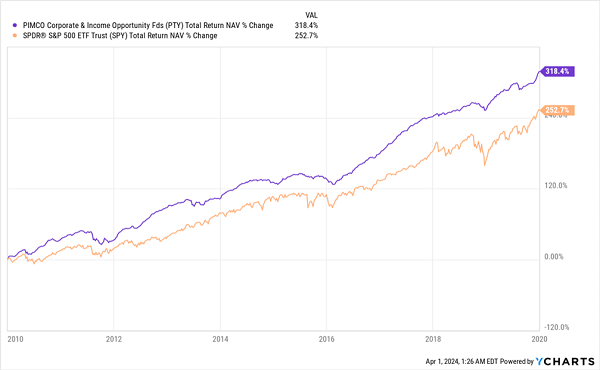

And on the ground, we’ve seen exactly that scenario play out. Consider PTY, which is listed above. During the 2010s, when interest rates were much lower than today, the fund’s net asset value (NAV, or the value of its underlying portfolio) soared. PTY’s portfolio (in purple below) even outran the S&P 500 (shown by the benchmark index fund, in orange below), due to management’s ability to select winners and avoid losers.

PTY’s Long-Term Success in a Low-Yield Environment

Not only did PTY beat stocks, but it maintained its generous payouts, too, which now yield that rich 9.6% we saw in the table earlier.

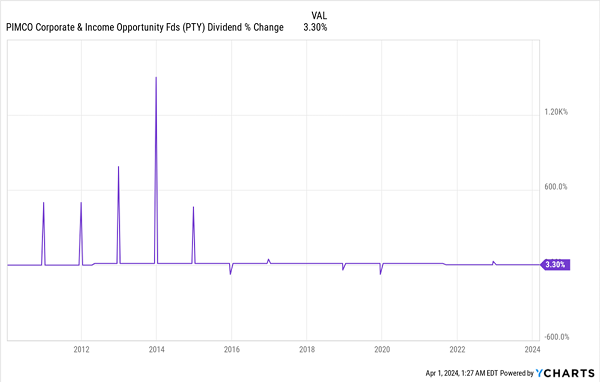

PTY’s Reliable Dividend, With “Bonus” One-Time Payouts

PTY did so well in the last decade that it even paid special dividends (the spikes and dips you see in the chart above), despite low rates! Now that yields are a lot higher and defaults haven’t risen significantly, PTY will have an easier time maintaining its current payout than it has in a decade.

Now, I have to be honest—PTY was able to do that because of a very aggressive trading strategy that other bond funds could not replicate. As a result, their performance was nowhere near as good. Both DHY and EVV are in that category, which is why their long-term returns couldn’t match PTY’s performance.

But remember what’s happened to interest rates.

Higher Rates = Easier Dividend Coverage for Everyone

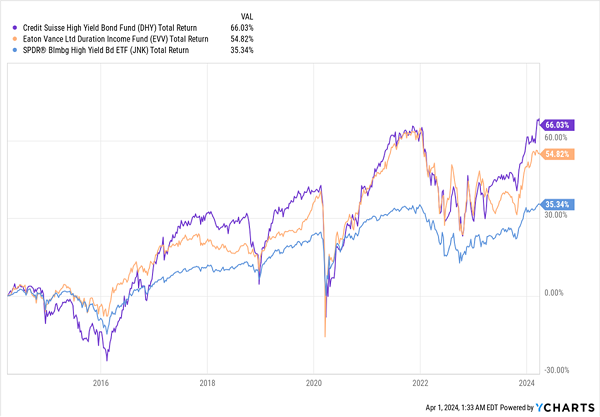

Unlike PTY, which trades aggressively, EVV and DHY have mandates that limit such aggression, so these funds tend to hold their bonds longer. The secret to their success is avoiding defaults. That’s helped DHY (in purple below) and EVV (in orange) outperform the broader corporate-bond index.

EVV and DHY Outrun the Broader Bond Market

Still, their long-term performance has been much lower than that of PTY, not only due to their longer holding periods but because they were limited by corporate bonds’ low yields pre-pandemic. That’s no longer the case, which is why funds have more reliable dividends than they’ve had for over a decade.

That leads us to these funds’ current pricing.

As we saw in the table at the top, while PTY is priced at a massive premium (30.9% as of this writing), DHY and EVV both sport 8.2% discounts, making them more interesting right now. PTY’s strong long-term returns were built in a different environment and aren’t too helpful to us now, looking into the future. With higher-yielding bonds on the market, and with these funds’ focus on holding high-yielding issues for longer than PTY, they are better positioned to lock in today’s high yields.

Plus, DHY and EVV have discounts that make their payouts more sustainable. DHY pays out 9.2%, but thanks to the magic of CEF discounts, management needs to earn just 8.5% on a NAV basis to maintain that payout, while EVV’s 9.8% yield becomes 9%, again thanks to its discount.

These sound like unbelievable returns, but they’re sustainable in a market where bond yields have soared and interest rates, as Jerome Powell recently hinted, are set to fall.

Lower rates (and bond yields) will boost DHY and EVV’s portfolio values, while their yields are locked in. That, in turn, might help both funds see the kinds of premiums PTY enjoys. If you buy in now, you’re likely to get in before other investors, giving you the potential to sell these funds later, at those higher prices.

5 More Big-Yielding CEFs to Ride the Bond Boom (and the Next Big Megatrends)

EVV and DHY demonstrate an often-overlooked benefit of CEFs: They let us get in on big swings in the market (in this case, the corporate-bond market) at big discounts. And because we’re getting a large slice of our income in dividend cash, CEFs add an extra layer of safety, too.

Yet few investors take the time to look into CEFs, falling for the siren song of low-fee (and pathetic-yielding) ETFs instead.

That’s why I refer to CEFs as a “hidden market.” But they likely won’t stay off the radar for long. As rates head lower, more folks will go hunting for higher income. And CEFs, with their high yields and big discounts, will attract their share of these investors.

So by moving into these funds now—starting with my top 5 CEF buys (current average yield: 8.6%!), we’ll be there well ahead of them.

Click here and I’ll explain why CEFs really are a “hidden” market the financial industry not only downplays, but actively steers investors away from! It’s a shame, but it’s driving this amazing dividend opportunity for us. By clicking the above link, you’ll also get the opportunity to download a FREE Special Report naming my top-5 CEFs to buy now. Don’t miss out.

Recent Comments