Look, I’m as ready for this selloff to end as you are. And when stocks drop—sending dividend yields skyward—I so badly want to back up the truck.

As value-focused dividend investors, buying dips is what we live to do. Sitting in cash is agonizing to me, as I’m sure it is to you, too.

But it just isn’t time yet. Which is why I’ve recommended just one stock this year in my Contrarian Income Report service, while urging my readers to stockpile cash. And after last Thursday’s dumpster fire, we’re sure glad we did!

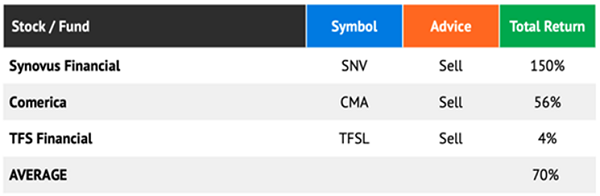

We’ve also lightened up our portfolio over these last few months, including taking some nice profits on three bank stocks we sold in May:

There was nothing wrong with these three: they were just benefiting from the Fed’s injection of cash into the markets, and the gap between the 10-year Treasury (at which they lend to clients) and the Fed’s policy rate (at which they lend to each other).

Now that Powell has overdone things and is letting the Fed rate rise, banks’ profit margins are being squeezed, so it was time to bid adieu. And we took some nice profits off the table by doing so.

Putting the Safety of Your Income (and Nest Egg) First

This is exactly the way we trade our dividends in Contrarian Income Report. And it’s why I won’t be a prisoner to the old-school investment-newsletter model that says I need to churn out a new pick every month. If I think doing so would put your money at risk—as I feel it would today—I’ll do what I have been doing: urging readers to stockpile cash and build their shopping lists.

When the time comes to deploy that cash, we’ll be ready. I’ll tell you exactly when that moment comes in Contrarian Income Report.

Closed-End Funds Are at the Top of Our List

One of the best things we’ll be very interested in buying when the smoke clears is high-yielding closed-end funds (CEFs). These vehicles are ideal because they often trade on the open market at different levels (and usually discounts!) than the per-share value of their portfolios, or net asset values (NAVs) in CEF-speak.

CEFs are cheap now, but I expect them to be even cheaper in a couple months. Then, when their “discount windows” slam shut (or revert to more normal levels), they’ll catapult our CEF prices higher. That will be a very nice payoff for our patience today, on top of the 7%+ dividends CEFs regularly pay.

CEF Discounts: Close the Window

Let’s start to look toward those brighter days now, by starting our CEF shopping list. Here are three to put near the top:

“Shopping list” CEF No. 1: A Megatrend-Powered 6.3% Dividend

When it comes to CEF investing, we demand one more thing, beyond discounts and dividends: megatrends! And there’s simply no more predictable megatrend than the aging of the US population. Sure, it’s been totally overshadowed by COVID, but it’s still there—and it’s accelerating.

According to a recent Reuters report, about 16.5% of the US population, or roughly 54 million people, are over 65. By 2040—just 18 years from now—that number will jump to 74 million, a 37% increase.

That’s going to lead straight to higher healthcare spending, and our first “shopping list” pick is nicely positioned to profit: the BlackRock Health Sciences Fund (BME), which yields 6.3% and sports a 2% premium to NAV that I expect to be taken out in the next few weeks, setting up a nice discount for us. BME also helps ease back our risk by sticking with big pharma stocks like Johnson & Johnson (JNJ), Pfizer (PFE) and Abbvie (ABBV).

Finally, this fund not only pays a high yield but is growing its payout, too, with a 6.5% increase announced last October. With the favorable trends we’ve got setting up for healthcare in the coming years, more hikes are likely on the way.

“Shopping List” CEF No. 2: A 10% Dividend From the Rise of “Rental Nation”

Sure, housing demand is softening, but with 30-year mortgage rates now around 6%, buying a home is still pricey. That’s causing many folks to change their house hunt to an apartment hunt.

Heck, there are now bidding wars for apartments—in Philadelphia, for example, renters are offering $500 or more a month above the advertised rent, according to recent reports.

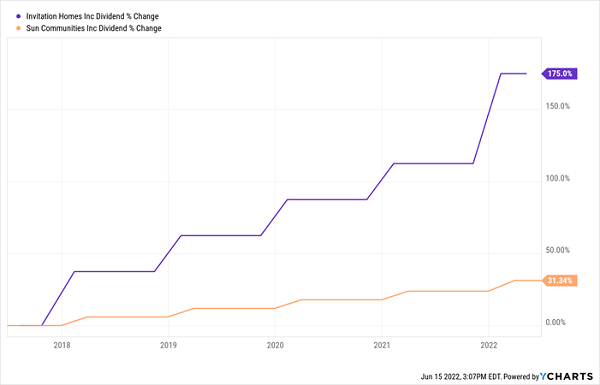

A CEF that’s well-suited to this trend is the CBRE Global Real Estate Income Fund (IGR), which devotes 16% of its portfolio to residential REITs, its second-biggest allotment. Sun Communities (SUI), which has mobile and manufactured-home parks across the south, is among its top-10 holdings, as is Invitation Homes (INVH), which holds single-family homes in the west and Florida.

Both stocks have been rolling out healthy dividend hikes, including relatively large increases late last year:

IGR’s Top Residential Holdings Drop Steady Payout Raises

We love IGR’s diversification, too: its top-10 holdings include other REITs offering in-demand properties, like cell-tower REIT Crown Castle International (CCI) and self-storage firms ExtraSpace Storage (EXD) and CubeSmart (CUBE).

IGR’s management team is doing a great job of handing the rising rent checks its portfolio companies are collecting over to us: it’s not often that you hear of a 10% dividend that’s growing (especially these days), but that’s exactly what’s happening with IGR:

IGR’s (Monthly) Dividend Yields 10% and Is Growing Quickly

Source: CEF Connect

IGR is a textbook case of why we’re holding off on buying now: despite the market carnage, it trades at a 0.85% premium. As is the case with our first pick, I expect that premium to be taken out in the coming weeks, setting up a discount opportunity (and a potentially even higher yield).

“Shopping List” CEF No. 3: A 93-Year-Old Fund That’s Seen Everything

Tri-Continental (TY) isn’t going to break records for its dividend: it yields 4.6%, low by CEF standards. But given the choice between TY and an index fund, I’ll take TY every time.

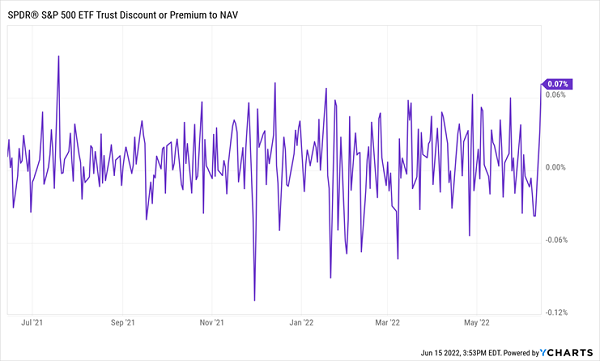

I’m making that comparison, by the way, because TY owns the same stuff as the benchmark SPDR S&P 500 ETF Trust (SPY), including Apple (AAPL), Pfizer (PFE), Exxon Mobil (XOM) and Dow Inc. (DOW). It cobbles together this blue-chip stock portfolio for a dividend that’s triple the 1.5% SPY pays.

Plus you get a deep discount, which clocks in at 12.4%, below the 8.3% TY has averaged in the past year, and I suspect we’re going to get an opportunity to buy for even less. I don’t know about you, but I’d rather get S&P 500 exposure with more of my return in dividend cash and at a discount! Which, by the way, is something ETFs like SPY never offer:

SPY Is Never Cheap

Finally, we’ll get a ton of institutional memory with this one: TY was launched in 1929, just before the Great Depression, so it’s dealt with everything the economy can throw at it, including rising rates. That may be why, unlike most other CEFs, TY uses almost no leverage—just 3% of the portfolio at last check.

A Once-in-50-Year Retirement Storm Is Hitting Us NOW (Here’s Our Gameplan)

I know how heartbreaking it is to check your account and see a smaller and smaller balance week after week.

This truly is a once-in-50-year event, with the oil shock of the late ’70s being the last time we saw a time like this. But if you were investing back then, you’ll also remember that right afterward, stocks took off in a raging bull market that led straight into the early 2000s.

Of course, history never repeats exactly, but it does rhyme, which is why I see better days ahead. I’ve explained my rationale in a Special Investor Bulletin you can read right here.

But what about right now? How do we protect our dividends until the skies clear? We’re not powerless. Far from it.

Beyond building our shopping lists with CEFs like the three we just discussed, we can still act to safeguard our cash and set ourselves up for gains (and dividends) on the other side of this mess. When you read my Special Investor Bulletin, I’ll show you how to access 3 Special Reports that reveal the 12 stocks you MUST sell now (these dividend pretenders are down for the count!) and lay out the high yielders I see as best positioned to hand us sturdy dividends (and upside) as we roll through this bear market.

Recent Comments