AI bubble? Bear market rally? I don’t care because I see five dividends between 10.1% and 13.5%.

Now that’s rarified air for yields! A benefit of a manic market such as this, where we have fear alongside insanity at the same time.

The five double-digit dividends we’re about to discuss aren’t tied to individual stocks, either. These payouts are dished by diversified funds with dozens or hundreds of holdings. All have experienced managers at the helm.

They just happen to be cheap because CEFland is still on sale after a rough run in 2022. Which is where we contrarians pick up the case.

The ABCs of Big Dividends: C-E-F!

Closed-end funds (CEFs) are a perfect place for us to find outsized yields.

Exchange-traded funds (ETFs), their more popular cousins, are pretty mindless. Most of them are index funds that blindly follow a benchmark, for better or for worse. And many of those benchmarks can be beholden to a single stock—which means just one company can make a massive dent in these supposedly diversified portfolios, and there’s nothing anyone can do about it.

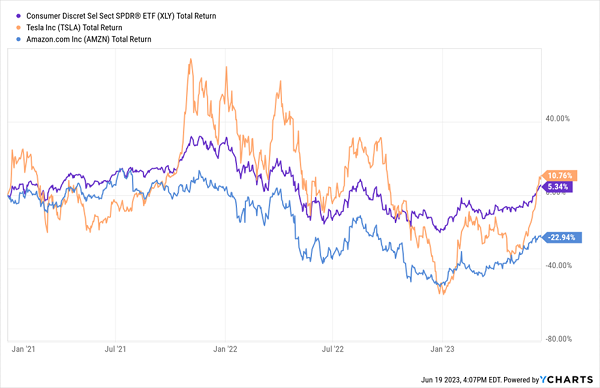

Consider the Consumer Discretionary Select Sector SPDR Fund (XLY). While it’s technically made up of more than 50 names, just two—Amazon (AMZN) and Tesla (TSLA)—account for more than 40% of the fund’s performance!

Is There Any Doubt What Moves XLY?

That’s great when they’re hot. But when they become wildly overpriced and overbought, XLY can’t shave some of its holdings to take profits and buy cheaper sector stocks. It has to stay the course and deal with their corrections, too.

Closed-end funds don’t have that problem—active managers can cull overheated stocks and spy values to their heart’s content. And there’s more to love than that.

CEFs also:

- Trade at steep discounts to their own net asset value (NAV): ETFs almost always trade very close to their net asset value thanks to a mechanism called “creation and redemption” where new units are being born and destroyed all the time. But while CEFs also trade on exchanges, they don’t have this mechanism—instead, from inception, they trade with a fixed set of shares. That allows CEF prices to move out of sync with their NAVs—sometimes they’re more expensive (and we want to avoid buying them when they’re too rich!), but sometimes they’re cheaper. It’s not uncommon to buy a dollar’s worth of stocks for 90 cents or less through a CEF!

- Use leverage. Mutual funds and ETFs have a straightforward task: Invest the money shareholders give them. If a mutual fund has $1 billion in assets, it will invest up to $1 billion in stocks, bonds or whatever it is directed to hold. But CEFs can do more. Closed-end funds may utilize debt leverage, buying more than what they could with cash assets alone. A manager of a $1 billion CEF may, for instance, use 20% debt leverage to invest $1.2 billion across his various selections. There’s two sides to this sword—it can amplify price returns and yields alike, but losses can cut much deeper.

- Use other trading strategies. It’s not uncommon for CEFs to use options strategies, such as trading covered calls, to generate even more income than the holdings alone could bring in.

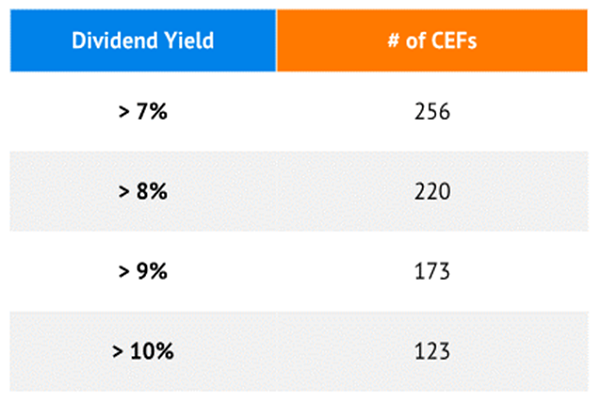

This translates into super-yields across the space. No, really. You can find literally hundreds of CEFs that have high-single-digit yields at a minimum.

You Can’t Swing a Stick at CEFs Without Hitting 7%-Plus Yields

Note: U.S.-listed CEFs

Source: CEFConnect

But because super-high yields are the norm, a CEF needs more than big income to stand out.

For instance, right now, five funds are on my radar that not only yield up to 13.5%—or in real-world numbers, $135,000 annually on a million-dollar portfolio—but also trade at a double-digit discount to NAV right now!

Three Funds Focused on Future Trends

I want to start by revisiting three equity CEFs I explored a few months ago:

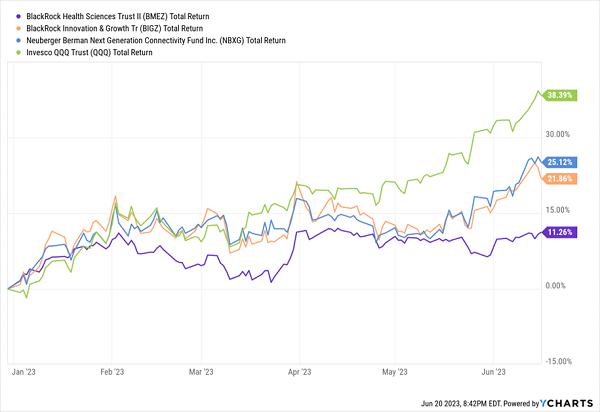

- BlackRock Health Sciences Trust II (BMEZ, 10.7% distribution rate): This healthcare-minded CEF, started in 2020, holds a number of biotechnology and health-science firms—companies such as biopharma Vertex Pharmaceuticals (VRTX), glucose monitoring specialist Dexcom (DXCM) ResMed (RMD) and med-tech outfit Stryker (SYK). Penumbra (PEN). It currently trades at a 15% discount to NAV that’s wider than its three-year average discount of 10%. Nice.

- BlackRock Innovation and Growth Trust (BIGZ, 10.7% distribution rate): BIGZ buys mostly mid- and small-cap companies that are, in the fund provider’s own words, are “innovative.” Unsurprisingly, BIGZ is high on tech-sector companies, but it also has tech-esque and other innovative players in healthcare, industrial, consumer and other sectors. Top holdings at the moment include advanced materials manufacturer Entegris (ENTG), Taser maker Axon Enterprise (AXON) and trading platform operator Tradeweb Markets (TW). This is a younger fund that went public in March 2021, so it only has a short 1-year average discount to NAV to compare against—18%, which is deeper than its current discount of 16%.

- Neuberger Berman Next Generation Connectivity Fund (NBXG, 11.8% distribution rate): This is another young fund that went live in 2021. And as the name suggests, it deals in next-generation mobile network connectivity and technology (think: 5G). Top holdings include chipmakers Nvidia (NVDA) and Analog Devices (ADI), as well as Amphenol (APH), which deals in cables, sensors, antennas, and fiber-optic connectors. NBXG has a deep discount to NAV of more than 18%, roughly in line with its one-year average.

All three funds have a few things in common: They all pay monthly dividends. They have high discounts to NAV. They use little to no leverage—but they can use options to generate income.

And as I pointed out in February, their young lives had been largely marked with difficult times for tech and tech-esque stocks, so their tattered track records and underperformance against vanilla indexes like the Invesco QQQ Trust (QQQ) weren’t much of a surprise.

But what they’ve done since then gives me pause.

They’re Lagging on the Way Up, Too

A good fund can still underperform on the way down or on the way up—but it can’t do both. And while it’s still early innings for these managers, it’s troubling that all three are trailing badly even after factoring in their massive yields.

I said before that we’d have more opportunity to buy all three CEFs at big discounts, and we do. But right now, I’m not sure we still want to.

A Steady Fixed-Income Eddie?

It’s possible the Federal Reserve is done raising interest rates—but it could just be on pause for a minute. Given that kind of uncertainty is still in the air, you wouldn’t be blamed for trying to generate some income while dampening your interest-rate risk.

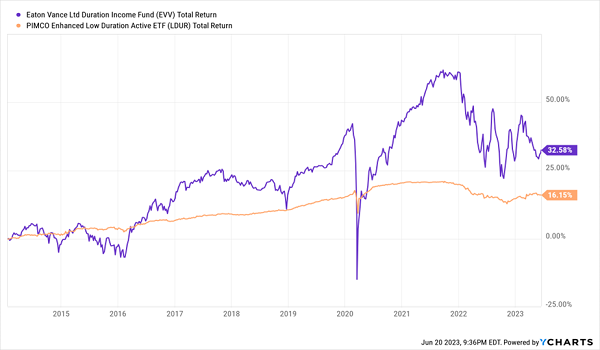

One way to do that: shorter-duration portfolios like the Eaton Vance Limited Duration Income Fund (EVV, 10.1% distribution rate). EVV tries to straddle an interesting fence of generating high income while maintaining a low average duration of between zero and five years. It does so by investing in things like senior loans (35%), junk bonds (29%), U.S. government and agency mortgage-backed securities (23%) and other fixed-income issues.

Credit quality is dicey—only about a quarter is investment-grade (though that quarter is AAA in nature)—but the adjusted duration is a mere 3.3 years. And that portfolio delivers a monthly distribution that yields in the double digits right now.

How does that translate to performance?

Positive—But With a BIG Asterisk

EVV is built much, much differently than the PIMCO Enhanced Low Duration Active ETF (LDUR) that I’ve compared it to. It uses more than 30% in debt leverage, and it’s willing to invest much more aggressively in lower-quality credit to seek out performance and yield.

EVV should outperform LDUR over time.

My hang-up: You’re not really shedding any volatility this way. EVV has been whipped around just as badly as many regular-duration fixed-income CEFs I’ve monitored. LDUR might get left behind in the dust, but at least its lower-duration portfolio is delivering less risk—compared not just to a high-leverage CEF, but to boring bond indexes, too.

A Trip Around the World

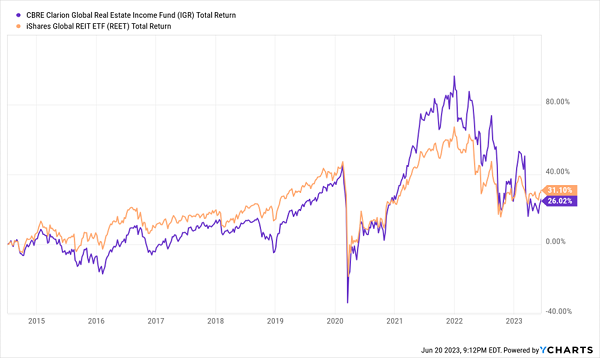

You won’t be surprised when I tell you that a CEF investing in real estate investment trusts (REITs) is poking its head out of the bargain bin. REITs have been dead money for a while—the worst sector since the start of the 2022 bear market, in fact, still down about 25% from those heights.

The CBRE Global Real Estate Income Fund (IGR, 13.5% distribution rate) sticks out for a number of reasons—its mammoth 13%-plus yield, for one, and an 11% discount to NAV that’s a hair above normal, for another.

But also, IGR provides a rare opportunity to play domestic and international real estate.

Most REIT funds focus primarily on U.S. REITs, which hold a multinational or two but rarely any overseas specialists. However, while CBRE’s global real estate fund still has 60% of its portfolio invested in American real estate stocks, 35% is exposed to Japan, Europe, Hong Kong, Australia, Singapore, and Canada. (The remaining 5% or so is U.S. REIT preferreds.)

Also juicing IGR’s yield is hefty leverage of 29% at the moment—and that leverage shows up in performance.

International Travel = More Turbulence With IGR

True, IGR lags a bland index fund over the long term, so management really hasn’t given investors a reason to favor it (and its higher fees) as a true foundational income holding.

8%-Yielding Blue Chips That Pay EVERY MONTH

But there’s something to be said for IGR’s ability to race ahead when REITs are in favor, as well as its generous and frequent monthly distribution. I’d at least keep an eye on its discount to NAV—if it widens compared to historical norms, it might be swing-trade fodder for real estate bulls.

We need sturdier performers for our retirement accounts, however.

Monthly income is nice, and high monthly income is even better—but what good are those payments if roller-coaster volatility pushes us to panic-sell our shares?

If we want to retire comfortably, we have to be comfortable with our retirement holdings. And for that, you need to target dividend-rich blue chips like the picks I hold in my “8% Monthly Payer Portfolio.”

The point of my “8% Monthly Payer Portfolio” isn’t just earning high levels of yield—it’s earning high levels of yields by leveraging steady-Eddie holdings that won’t have you waking up in cold sweats every few nights.

You don’t need to be anxious about bleeding your nest egg dry, either. The income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Do the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments