As income investors react to the new tax plan, it’s a good bet that some are overreacting to certain aspects of it. They always do.

There’s confusion between high yielding fixed income, and pure junk. There’s also a flood of tax-advantaged paper about to hit the market, creating bargains for smart buyers.

The result? Yields up to 10%, with some price upside to boot!

Bargain #1: “Smart” High-Yield Bond Funds for 7.5%+

If you hold high-yield (often called junk) bonds, you may have noticed they’ve sold off as the Republicans’ tax talk became serious. They’ve taken down other assets, too – some for good reason, some not.

Today, “highly indebted companies” can deduct their interest payments (which makes it a good deal to have debt). The current tax proposal would limit this tax break, potentially throwing some cold water on the high-yield bond market (and the “junky” companies that depend on it).

Since the tax talk started, many closed-end funds (CEFs) have seen their prices drop excessively when compared with their net asset value (NAV). Let’s take the largest high-yield CEF, BlackRock’s Corporate High Yield Fund (HYT). Its NAV is down just 0.9%, but the fund’s price has dropped more than three-times as much:

An Excessive Price Drop

Meanwhile the SPDR Bloomberg Barclays High Yield Bond ETF’s (JNK) price drop has been much more “fair,” falling in line with its NAV:

A Double Standard

Fittingly JNK has seen its “dumbly selected” assets drop faster than HYT’s handpicked bunch. (Which is why I don’t have to remind you about the value of an active bond manager, as we discussed last week).

HYT’s positions are largely free of the corporate bonds that might be hurt by the tax plan. But few investors bother to check actual holdings these days.

That’s a big advantage for us. HYT pays 7.5% and trades at a 9.5% “free money” discount to its NAV. That’s roughly its low water mark of the year.

And HYT isn’t alone. There are other high paying funds I like even more that are paying 8%, 9% and even 10% – with upside to boot. We’ll discuss those in a minute. First, let’s prepare for a potential flood that should be bought.

Bargain #2: Municipal Bonds for 5.7% to 10%

Our resident “CEF Professor” Michael Foster is whipping up a brilliant rundown on municipal “muni” bonds and the tax plan for his subscribers tomorrow. We’ll also be cross-publishing his piece on our Contrarian Outlook website in the morning, so you can check our website for Michael’s analysis if you’re not yet a subscriber of his.

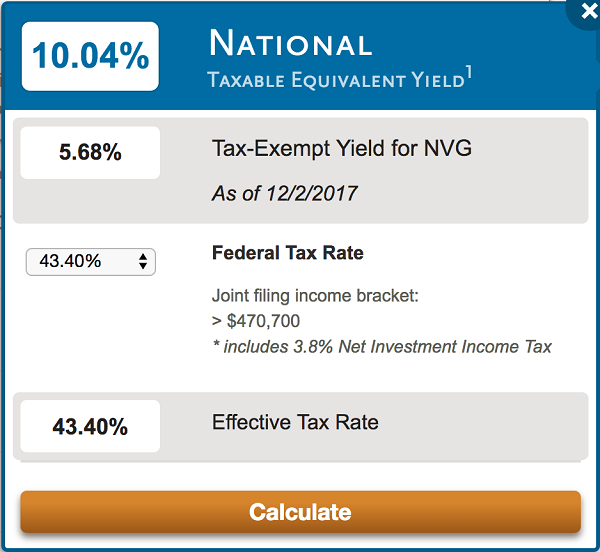

This time last year, I called the ensuing rally in munis. My Contrarian Income Report subscribers enjoyed 13.7% total returns from our Nuveen AMT-Free Muni Credit Fund (NVG) – and many of my “high bracket” readers did even better thanks to these tax-advantaged returns.

A “Boring” 13.7% (or Better) From Safe Munis

How’d some readers earn even more? Remember, most muni bonds are Federal tax-exempt. Which means a 5.7% paying fund like the NVG actually pays top-bracket earners a 10% tax equivalent yield!

A 10% Tax Equivalent Yield

For a secure investment, muni bond prices sure can swing wildly. Which is exactly why, from time to time, they provide us with such stellar buying opportunities.

In a sane world they would always trade at modest yield premiums to Treasuries. But I prefer to buy them now, when they are paying 7% to 8% more (in taxable terms) than T-Bills. A generous premium.

Plus, it could be the perfect time to go holiday shopping for more tax advantaged munis. Barron’s reports that states and localities may issue as many as $17 billion in bonds in the weeks ahead as they race to issue debt that will no longer be allowed under the current tax plan.

A flooded muni market will be bad for sellers, but good for buyers like us. As usual, it will pay to choose a fund run by a savvy muni bond manager. Firms like Nuveen and PIMCO should have a field day as they’re able to buy plenty of muni bonds at bargain prices – and bank higher yields.

My Favorite 8% Tax Plan Plays (With Upside, Too)

The beauty of these “tax plan favored” secure high yields is that, even if we don’t buy at the exact bottom, we can “ride out” any price fluctuations. By living off dividend income alone, we never have to sell anything – which means we can buy right and sit tight until the market corrects itself.

Many investors try to do this with a portfolio of dividend aristocrats. Problem is, 3% payers won’t quite get it done. Unless you’re already incredibly wealthy, you probably need high-single-digit yields to make dividend investing worthwhile.

That’s why I recommend a full “no withdrawal” portfolio of secure 8% payers. There are actually safe funds and stocks that pay this much. They don’t get a lot of coverage in the mainstream financial media because most investors are distracted by big blue chip names.

Popularity comes at a price. You just can’t live off dividend income alone if you’re only banking 2% or 3% per year.

The solution? Stealth plays like closed-end funds, preferred shares, muni bonds and recession-proof REITs. You can build a safe, diversified portfolio from these types of issues that pays 8% – which means you’ll never have to lose sleep over price gyrations again.

Want to learn more – and buy a few high paying shares? Click here and I’ll share everything about my “no withdrawal” strategy, including the names and tickers of the stocks and funds that you can buy for secure 8% yields.

Recent Comments