Don’t be cheap when you buy bonds this holiday season (or ever, for that matter). Bargain shoppers, sadly, tend to be the most at-risk of outliving their fixed income portfolios!

But it’s easy for you and me to double up “regular” bond returns simply by swapping out popularity for quality.

Let’s walk through some of the most popular fixed-income plays today – and replace each with something that yields more (with superior price upside to boot).

The obsession with fees is understandable. Most investors are conditioned by their experience with stock-based mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

But it’s costly to be cheap in the bond market. Do you really want any company’s debt? Or any city’s munis?

Of course not. That’s why we want an industry expert sifting through the available deals for us. And if that person has access to the best deals, all the better. (The bond market is not as democratic and accessible as the stock market, after all).

Let’s first consider preferred shares, which are issued by firms to raise capital. The company will pay regular dividends on these shares – and as their name suggests, preferreds do receive their payouts before common shares.

Investors typically get paid more, and even have a priority claim on the company’s earnings and assets in case something bad happens, like bankruptcy. An especially good deal in times like these, when common stock prices are high.

The iShares US Preferred Stock ETF (PFF) is the most popular vehicle for preferred share investing. It charges a 0.47% in fees – which is rich for an ETF, but cheaper than a professional money manager (who would usually be required to buy these types of securities.)

PFF owns preferreds issued by the likes of Wells Fargo (WFC), HSBC (HSBC) and Allergan (AGN) today. It yields 5.8% today and commands $18 billion in assets.

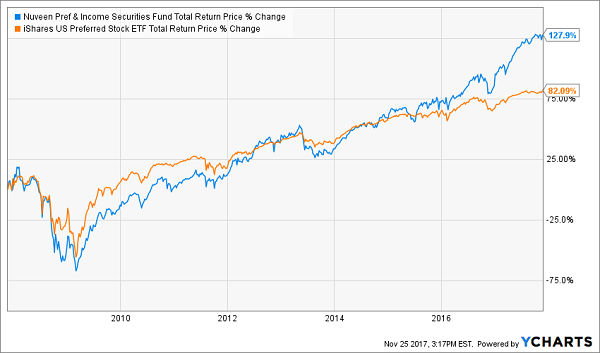

Meanwhile its most popular counterpart in the closed-end fund (CEF) world is Nuveen’s Preferred & Income Securities Fund (JPS). Its 1.19% management fee and lower profile result in a smaller fund – just $2 billion in management.

But in this winner-take-all economy – where entire industries (like retail) are quickly becoming obsolete – it pays to have a professional at the steering wheel. Fees dished to JPS have been well spent over the past decade, as the fund has trounced more popular PFF with 128% total returns (net of fees) versus just 82%:

It Pays to Pay for Preferred Expertise

JPS still pays 7.2% today.

And how about boring old municipal bonds? Expertise matters here, too.

Nuveen’s AMT-Free Quality Muni Fund (NEA) has outpaced iShares National Muni Bond ETF (MUB) counterpart 81% to 48% over the past decade. NEA’s savvy management along with its access to better muni deals (with Nuveen receiving the inside track on many issuances) easily make up for its fee premium (0.87% to 0.25%).

There’s Alpha in Munis, Too

(A new study quoted by Barron’s over the weekend also concluded that muni-bond CEFs outperformed their ETF counterparts by a wide margin since 1990).

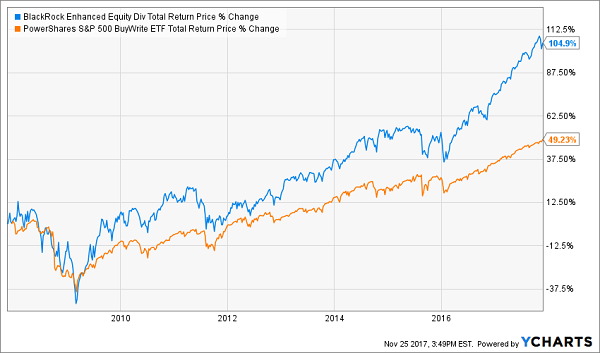

The alpha extends to bond proxies as well. Let’s compare the leading “buy-write” fund in each world (a strategy that creates income from stocks by buying them and writing covered calls on those positions). Instead of buying the S&P 500 for its 2% yield, you could purchase a buy-write fund like BlackRock’s Enhanced Equity Dividend Trust (BDJ) for yields up to 6.2%

If you’re tempted by the lower fees offered by Powershares’ S&P 500 BuyWrite ETF (PBP), your “deal” might cost you half of your potential profits:

The Right Way to Buy-Write

Now let’s correct two common misconceptions in fixed income:

- CEF yields are always quoted net of fees. Which means we shouldn’t judge expenses in a vacuum. Instead, we should consider the net dividend and the potential total return.

- If we buy smartly, we can even get the management fees comped.

I’ll show you how to achieve “VIP status” shortly. First, let’s recap what to buy instead of ETFs (and mutual funds, too) for meaningful fixed income with upside to boot.

How to Hire the Best Bond Manager

A top money manager will usually cost you 2% annually (plus 20% of profits). And it’d take a million bucks or two to get his or her attention.

Closed-end funds, however, give you a way to invest with the best bond firms (like Nuveen and PIMCO) and best managers (like PIMCO’s Dan Ivascyn and DoubleLine’s Jeffrey Gundlach).

These experts and their rolodexes tend to be more expensive than the “dumb” ETFs, of course. But if you know what you’re doing, you can get that fee waived – and ride their high yield gravy trains for free.

How to Get Your Management Fee “Comped”

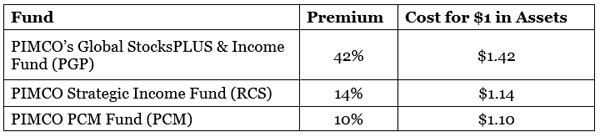

Most investors pay a premium to invest with PIMCO. Here are three funds in total fetching up to $1.42 on the dollar thanks to the name next to the ticker:

Big PIMCO Premiums Today

I get why investors pay the premiums – but I won’t pay it myself.

Instead, I always demand a discount. This is unique to CEFs – thanks to their fixed number of shares, they can (and often do) trade at discounts to their net asset value (NAV) as well.

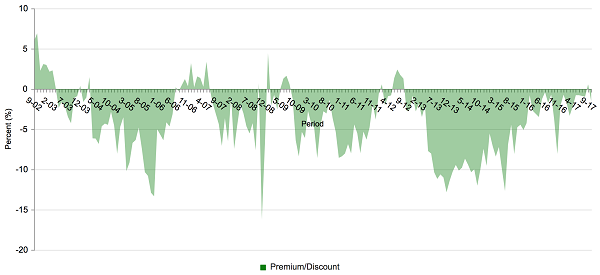

Let’s consider JPS again (our preferred fund). It trades for a modest 0.8% discount to its NAV today, which means investors who purchase it today are getting two-thirds of their fees “comped.”

But patient investors – with a contrarian mindset – are likely to do even better. Historically, JPS has traded at steeper discounts:

Premium (+) vs Discount (-) Since Inception

A bigger discount means we have some additional upside (as the discount window closes) and our yield is higher than it would be if the fund traded for fair value (because income is earned per NAV unit – so the less we pay for it, the better).

Investors who smartly bought JPS when its discount was high (in other words, when the orange line below was low) successfully “bought the dips” and enjoyed upside in addition to their 7%+ yields:

The Bigger the Discount, the Bigger the Bargain

JPS isn’t a particularly compelling play today. I’d rather wait for the next panic! Instead, I prefer these three heavily discounted (and high quality) funds as best buys today.

My 3 Favorite CEFs for 8% Yields (and 10%+ Upside)

I put together a special report called the “Dividend Superstars: 8%+ Yields with 10%+ Upside” that highlights my three favorite bond plays today. All three are run by top notch managers, including:

- A 6.1% payer with all the inside connections in the world. It’s trading at an absurd 9% discount to NAV,

- The brainchild of one of the top fund managers on the planet paying 8.6%,

- And an 8.4% payer that’s aggressively closing its own discount window with a repurchase program (which means its price will soon head higher).

In the report I’ll share the ticker symbol, my buy-up-to price and in-depth backstory on each fund. I’d love to send you this report for free. Please click here to claim your copy of my special 8%+ yields report today.

Recent Comments