These shareholder-spoiling stocks regularly double or triple their investors’ money. They’re a bit underappreciated, but not often on sale – unless you buy them this time of year.

And on cue, right now they’re as cheap as they’ve been in 12 months.

If insurance is a great business, then reinsurance is a fantastic one. (Reinsurance is insurance purchased by insurance companies to manage their own risk exposure.)

Insurance itself, when done responsibly, is a cash cow. Firms collect payments up front from their customers but may not have to pay it out in claims for a long time, if ever. The companies then invest that money – called “float” – and pocket the income they earn.

If they priced risk properly up front, they make more on premiums than they have to pay out in claims. Plus, they get to keep the profits they made on the capital they borrowed for free!

Reinsurance is especially tricky, because claims can come in bunches. Hurricane Harvey’s total financial damages will be $100 billion or more. Texas auto insurers have already fielded 100,000 claims, and one prominent trade association believes that number could climb as high as 500,000.

This will be a huge hit to auto insurers’ bottom lines. And many investors have assumed that the industry’s backstop – the reinsurers – will absorb many of these losses as well.

But reinsurers usually emerge from hurricane season relatively unscathed. And they tend to outperform the S&P 500 every September (along with most other months on the calendar, too).

Take these two leading stocks in the space – they usually to selloff in late summer, and rebound quickly:

An Almost-Annual Buying Opportunity

And these are price gains only (before dividends). The smartest reinsurers pay plenty of dividends because they are extremely capital efficient. In fact favorite firms in the sector regularly return most or all of their net income back to their shareholders every year by:

- Paying generous dividends,

- Regularly raising these payouts, and

- Constantly repurchasing their shares.

This “triple-threat” represents one of the easiest ways to triple your money every ten years. If you bought a basket of reinsurers on the eve of the financial crisis, you did just fine:

What Crisis? The Best Reinsurers Triple Your Money

How to Triple Your Money in Ten Years

Let’s look more closely at Everest Re (RE), which dates all the way back to 1973. It has a distribution network and relationships with insurers on five continents. The company, as mentioned, is on the hook to pay claims when catastrophes strike. This makes geographic diversification key, because disasters tend to be local affairs.

Paradoxically, disasters can also create business opportunities. For example, the recent Fort McMurray wildfire in Canada caused the largest insured loss in Canadian history. It drove reinsurance rates up substantially – which Everest used to deploy more insurance capacity at these higher prices.

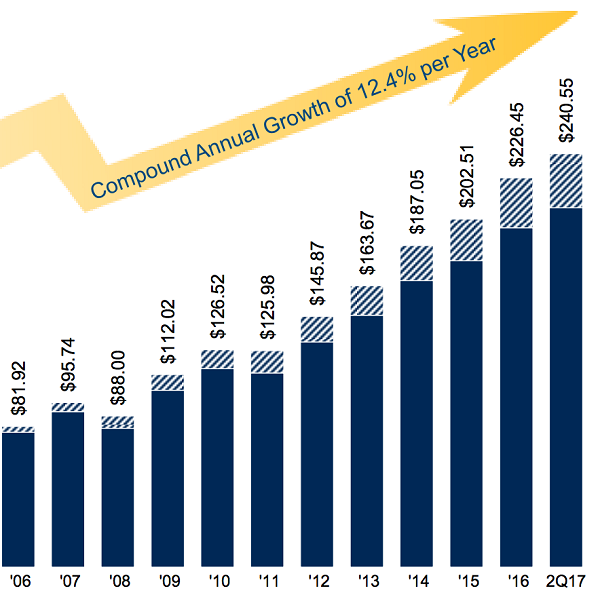

Reinsurers can quickly compound their profits. Everest, for example, has grown its book value per share by 12.4% per year since its IPO two decades ago:

The Magic of Reinsurance Compounding (12.4% per Year)

As Warren Buffett does with Berkshire Hathaway, Everest emphasizes its growth in book value (plus dividends) to gauge value creation for shareholders. This reflects the amount of money its assets would fetch today if the firm were liquidated – a relatively accurate measure because its balance sheet consists of bonds and other securities with active markets for them.

Everest’s 12.4% compounding of book value plus dividends since its IPO demonstrates an excellent multi-decade track record. As does its impressive “combined ratio” which shows how efficient its operations are.

Combined Ratio = (Incurred Losses + Expenses) / Earned Premiums

A ratio below 100% indicates an underwriting profit – which means the business is profitable thanks to savvy underwriting alone. From there, the income generated from investing the float is gravy – potentially a lot of gravy, but not required to run the business.

Everest has always been good at making money by simply writing policies. Since its 1996 IPO, its combined ratio has been 96.6% over the subsequent two decades – which means the firm earns $0.034 for every $1 it receives in premiums.

Three-plus cents on the dollar may not sound like much, but this is additional free money the firm can invest for extra profits. It’s why insurance (and especially reinsurance) is an even better business than banking – these companies not only get paid by their customers to invest their money and pocket the profits, but if they’re good at writing policies, they don’t even have to give all the original cash back.

More Money Than It Needs

Everest simply has more money than it knows what to do with – which means shareholders usually receive the lion’s share of profits.

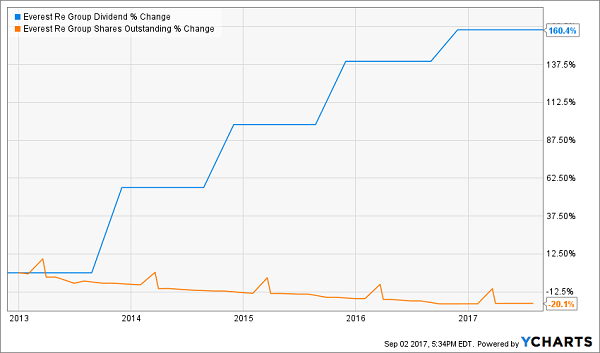

Shares pay a modest 2% today, but with a conservative 17% payout ratio (the percentage of earnings being paid out as dividends) there is more upside for a dividend that’s already increased by 160% in the last five years.

In fact, that leaves an additional 83% of earnings still looking for a pocket to land in. Which means the cash that isn’t set aside for the next dividend hike will most likely be used on continued share repurchases. Over the last five years, management has bought back 20% of shares outstanding – one-fifth of the company!

Share Count Down, Dividend (Way) Up

This is a beautifully virtuous cycle for shareholders. As Everest buys back its own cheap shares, it saves money on future dividend payments (by having fewer shares to pay). Which helps management hike the payout per share more than it otherwise would with a static number of shares.

And remember, while everyone seeks out current yields, dividend hikes are highly underrated as a driver of stock prices. The sooner a firm doubles its dividend, the sooner its shares will double in price. And you’ll get more payout for your buck when you buy on pullbacks – like the current almost-annual sale in reinsurers.

A 3-Step Process for 12%+ Returns per Year, Forever

That’s’ why the very best dividend stocks to buy never show high yields because their prices keep rising in line with the increasing payments.

Most people never realize any of this.

But those of us who DO stand to profit handsomely and almost automatically!

It’s a simple three-step process:

Step 1. You invest a set amount of money into one of these “hidden yield” stocks and immediately start getting regular returns on the order of 3%, 4%, or maybe more.

That alone is better than you can get from just about any other conservative investment right now.

Step 2. Over time, your dividend payments go up so you’re eventually earning 8%, 9%, or 10% a year on your original investment.

That should not only keep pace with inflation or rising interest rates, it should stay ahead of them.

Step 3. As your income is rising, other investors are also bidding up the price of your shares to keep pace with the increasing yields.

This combination of rising dividends and capital appreciation is what gives you the potential to earn 12% or more on average with almost no effort or active investing at all.

I’ve scoured thousands of stocks out there right now, looking for the very best companies that have both rising dividends and strong buyback programs in place … the kind of stocks that could easily spin off annual total returns of 12%, 17%, even 25% or more … doubling your money in very short order.

Right now, at this very moment, there are 7 in particular that I think you should consider buying.

They stand to do well no matter what the broad market does … regardless of what happens in Washington … and irrespective of interest rate trends.

Recent Comments