Do yourself a favor and shut out all the “experts” who say it’s impossible to retire on dividends alone. They’re just plain wrong! Because even today, with stocks soaring (and dividend yields in the tank), you absolutely can build a portfolio yielding a solid 7%+.

We’re going to do it now, and we’re going to do it easily—with just three funds. These funds—part of a unique asset class called closed-end funds (CEFs)— pay 7.6% between them, and the biggest yielder of the bunch throws off a huge 8.7% payout!

And they’re just the start.

A 7.6% dividend yield is enough to pay you $38,000 a year on just $500K invested, and you wouldn’t have to draw a single penny of your principal to get that cash stream. Best of all, September is the perfect month to move your nest egg into a portfolio of CEFs like the ones we’ll dive into today, as I’ll explain shortly.

(We’re not the only ones spotlighting high-yield plays like these, by the way. A recent article in Investor’s Business Daily also recommended high-yield CEFs as strong sources for retirement income, and I was happy to be quoted in it.)

Before we get to names and tickers, let’s look at why a “dividends-only” strategy really is your only safe retirement option.

Why Wall Street’s Recommended Retirement “Plan” Is a Mess

Ask any advisor and they’ll likely tell you that a 7.6% dividend is either impossible to find or, if you do find one, too vulnerable to being cut. (This unimaginative response stems from the fact that a majority of these folks have never heard of CEFs.)

Instead, they’ll likely steer you to the so-called “4% rule,” which states that you should sell down 4% of your portfolio for every year you’re retired. You’ve no doubt heard of this scheme; its simplicity is seductive. But stop and think about it for a second: have you ever heard of anyone who’s used it successfully?

Probably not.

That’s because, while in many years withdrawing 4% works all right, inevitably you’ll be faced with a chart like this:

The 4% Rule’s Disastrous Flaw

You’re withdrawing money at exactly the wrong time! The dividend on Caterpillar Inc. (CAT) is fine, but you need to sell shares for additional income. Remember the benefits of dollar-cost averaging that you likely used to build up your savings? This is the same phenomenon but in reverse!

With a 4% withdrawal portfolio, you sell more shares when prices are low and fewer when prices are high. It’s a recipe for running out of money.

So, for your own safety, I implore you to ignore the 4% rule and take a hard look at our dividends-only strategy, which turns on CEFs.

CEFs are similar to mutual funds, but with two key differences:

- They pay huge dividends: As I write this, CEFs throw off 6% payouts, on average, and many pay a lot more. When you start with an average payout of 6%, it’s easy to “cherry-pick” CEFs paying 7% or more.

- They often trade for less than they’re actually worth. Unlike ETFs and mutual funds, CEFs boast a “one-click” indicator that tells us when they’re cheap and when they’re pricey. Called the discount to NAV (or net asset value), it’s unique to CEFs and visible on any fund screener worth its salt.

September Could Be Prime Time for Yield Hunting

Here’s another reason why this strategy makes a lot of sense now: we could be in for a pullback in September, which would inflate dividend yields on CEFs and other dividend investments.

We know this from history: according to a recent Barron’s article, September is the worst month for stocks—if you go back nearly a century, to 1928, Septembers have pushed the S&P 500 to a loss of 0.99%, on average. That’s a big gap from the second-worst month, May, at a 0.11% loss.

If this month follows suit, CEF discounts could widen, and their dividend yields could see a nice bounce, too. Here are three examples of CEFs that would be good fits with a no-withdrawal strategy, either now or after a September storm:

“No-Withdrawal” CEF No. 1: A 6.3% Dividend for 94 Cents on the Dollar

Our first example is the BlackRock Enhanced International Dividend Trust (BGY), which holds 86% of its portfolio beyond America’s shores and trades at a 6.4% discount to NAV, so we’re paying 94 cents on the dollar for its holdings.

The portfolio is a laundry list of household-name (in their home markets) stocks like AstraZeneca PLC (AZN), Prudential PLC (PUK), spirit maker Diageo PLC (DEO) and Canadian telecom Telus Corp. (TU).

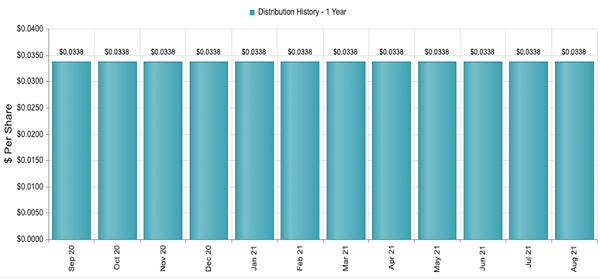

BGY also boasts a 6.3% dividend and, yes, pays monthly. Its payout also held firm throughout the 2020 mess, giving its investors a reliable cash lifeline. That’s exactly the kind of battle-tested dividend we want for our no-withdrawal strategy.

BGY’s Rock-Steady Payout

Source: CEF Connect

Now let’s move on to …

No-Withdrawal CEF No. 2: A Rare 7.9% Dividend Paid Monthly

If you don’t want to buy three CEFs to get your 7% dividend, you could get away with just the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund (ETW). It gives you a 7.9% dividend and plenty of diversification: with 55% of its portfolio in the US and the rest overseas, ETW combines American megacorps like Apple (AAPL) and Microsoft (MSFT) with European mainstays like Nestle SA and drug maker Roche Holding AG.

The fund also writes call options on its portfolio, a smart strategy that lets it collect cash premiums in exchange for the option to sell its stocks to the payer of those premiums at a later date. It’s a proven way to generate extra cash that supports ETW’s huge 7.9% dividend. And with the fund trading at a 0.2% premium to NAV—essentially par—you can be sure you’re not overpaying.

No-Withdrawal CEF No. 3: A Value-Focused CEF Yielding 8.7%

Finally, there’s the Gabelli Equity Trust (GAB), run by value-investing guru (and popular commentator) Mario Gabelli. This one offers the biggest dividend of the bunch: a monster 8.7% yield! (Though unlike our first two picks, you’ll have to wait every three months for your payout, rather than getting dividends monthly.)

Gabelli’s eye for value has paid off for investors: coming out of the 2020 crash, his fund has dominated the S&P 500, going by its total NAV return (or the performance of its portfolio alone, including dividends it collects on its holdings).

Gabelli Buys the Crash—and Cashes In

GAB is the most US-focused fund of our three examples, with 80% of its portfolio invested at home. Mastercard (MA), Berkshire Hathaway (BRK.A) and Texas Instruments (TXN) are examples of all-American large caps among its biggest holdings.

The fund does trade at a premium—3% as of this writing, but that’s below its 5.6% average over the last year and well below its 52-week high of 15%, so it’s still a bargain, even though we’re technically paying a bit more than the portfolio’s value.

Plenty More Big CEF Dividends Where These Came From

Taken together, we’ve got a 7.6% average dividend from these three funds, plus a nice geographic balance, too. And two of them—ETW and BGY—send cash your way every month. And these are just three examples of the huge “no-withdrawal-friendly” dividends available in CEF-land.

Yours Now: My Top CEF (and non-CEF) Buys for a “No-Withdrawal Retirement”

In fact, these three funds aren’t even among my favorite ways to retire on dividends alone. For those, I urge you to check out my “7% No-Withdrawal Portfolio.”

This potent portfolio diversifies you across the economy, holding stocks and funds that do exactly what the name says: pay you 7% dividends, on average. And you can draw even higher payouts by cherry-picking the highest payers of the bunch: some investments in this portfolio pay north of 9%!

Plus these stocks and funds are ALL trading for less than their true worth now—which, I know I don’t have to tell you, is a rarity these days. Their attractive valuations set us up for some nice “bonus” upside to go along with our massive dividend payouts.

The time to invest in these stout “no-withdrawal” plays is now, and I can’t wait to show them to you. Go here and I’ll give you a guided tour of my “7% No-Withdrawal Portfolio,” revealing the names and tickers of every investment inside it along the way.

Recent Comments