Plenty of investors will tell you that the higher an investment’s dividend yield, the greater the risk you’ll suffer a big dividend cut, especially in a market downturn.

To that I have one response: these folks have never invested in closed-end funds (CEFs)!

The portfolio of our CEF Insider service is a case in point. It yields a healthy 6.6% on average—five times more than the income-starved S&P 500 crowd gets—and the payouts on our funds have held up beautifully throughout this crisis.

Like the Eaton Vance Tax-Advantaged Global Dividend Fund (ETG), which we bought in January 2020, when it yielded a handsome 6.7%. Throughout the pandemic, that payout held strong: overall, ETG handed investors a 27% total return from those pre-crisis days, with most of that in dividends, thanks to its blockbuster yield.

But not all CEFs are winners like ETG—some bleed away your cash with outsized fees, underperformance and worse—so we do need to be careful. Here are three tips you can use to zero in on CEF winners and sidestep the land mines.

CEF Safety Tip No. 1: Know When to Change Course

Let’s start off by looking back to the early 2010s. Back then, you may have heard the argument that high-yielding master limited partnerships (MLPs) that operate pipelines can’t lose because they charge a per-barrel fee to ship oil and are thus immune to falling oil prices.

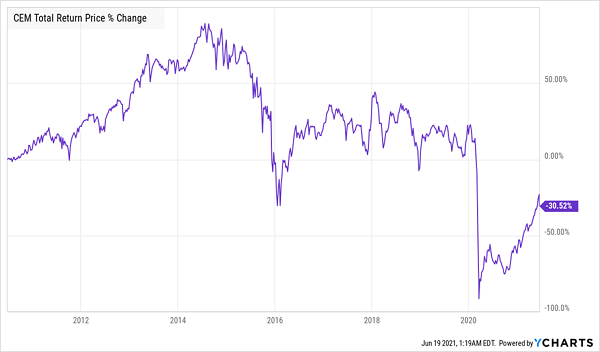

One way to play that angle would’ve been through a CEF like the ClearBridge MLP and Midstream Fund (CEM), which pays 6.5% today.

However, like oil prices, CEM is highly volatile, and investors who didn’t move on when the “MLPs don’t care about oil prices” argument fell flat in 2014, after oil collapsed, sat through years of volatility before a worse crash in 2020, from which CEM hasn’t yet recovered.

CEM’s Rough Decade

To be sure, buying CEM at bottoms, or when oil is out of favor, is a good way to grab some short-term gains, but this strategy isn’t for the faint of heart. You’ll need to have steady nerves and be ready to sell quickly on any market pullback. In other words, this isn’t a fund to buy and tuck away forever.

CEF Safety Tip No. 2: If a Fund’s Strategy Can’t Be Easily Explained, Dump It

Eagle Point Credit Company (ECC), payer of a 7.1% dividend, is eager to tell investors that its portfolio is hard to understand. And they’re right; it is. ECC invests in equity collateralized loan obligations (CLOs), the riskier end of a group of exotic derivatives that can’t be easily explained in a thousand words, let alone a sentence.

Further, ECC borrows aggressively and charges high fees (they vary, but they’ve exceeded 10% of assets in the past), in addition to holding a portfolio that’s highly sensitive to market disruptions.

ECC Gives Investors Heartburn

While ECC shareholders saw their investment plummet over 60% in value in the darkest days of the pandemic, a mix of Federal Reserve bailouts and income-hungry investors have helped the fund recover to pre-pandemic levels—even if it’s still far underperforming the S&P 500. In the next crisis, ECC may not be so lucky.

CEF Safety Tip No. 3: Embrace Leverage—to a Point

Now that we’ve talked about what to avoid when picking CEFs, let’s look at something to look for. This one may surprise you: leverage.

To be sure, a cause of big dips like the ones you see above is a fund that simply borrows too much money, which magnifies its losses in a plunging market.

Many investors respond to this by avoiding leverage altogether, but that’s a missed opportunity. Imagine refusing to buy a car or a house without taking out a loan! Leverage, when used prudently, can magnify returns, especially in a period of record-low borrowing costs like the one we have today. The key is to avoid too much leverage.

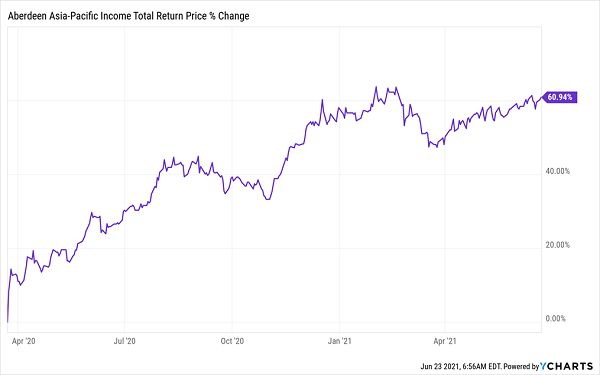

But how much is too much? Studies show that, in most downturns in the past, 20% to 25% leverage has been perfectly safe, as the Aberdeen Asia-Pacific Income Fund (FAX), a holding of our companion Contrarian Income Report service, proves.

As I write this, FAX boasts a 25.6% leverage ratio and has shown that a modest amount of borrowing can augment returns without being a downturn risk (FAX easily bounced back from the dot-com crash, the 2008/’09 housing market crash, the 2013 taper tantrum, and the COVID-19 crash).

Leverage Propels FAX Back From the March 2020 Mess

The fund’s leverage-assisted gains also help secure its 7.6% dividend, which gives its shareholders a high, secure income stream they can use however they like.

5 “Lifetime Profit” CEFs Yielding Up to 8.2% (With Massive Gains Ahead)

FAX is just the start of the high-yield bargains you’ll find in CEF-land. I’m also urging investors to pounce on 5 other CEFs dropping huge dividends now: the highest yielder of this cash-rich bunch throws off a jaw-dropping (especially these days) 8.2% dividend!

And these funds are cheap, too—so much so that I’m calling for 20%+ price gains from each of them in the next 12 months. When you throw in the big dividends you get from these 5 picks, you’re looking at a quick 27%+ total return here! And you get a ton of diversification, too, which helps keep your nest egg safe in a crash.

The time to buy these funds is now, before their ridiculous discounts vanish. Click right here to get a free investor report giving you the full story on these 5 high-yielding CEF picks, including their names, tickers, complete dividend histories and everything else you need to know.

Recent Comments