ETFs, mutual funds—and, yes, high-yielding closed-end funds (CEFs)—all have one surprising new year’s resolution this year: cutting their management fees.

But unlike my resolution to stop eating donuts and work out three times a week, this is a resolution that managers of these funds will likely keep—setting their funds up for higher returns as a result.

Why? Because their feet are being held to the fire.

Activists Push for Big Fee Cuts

Truth is, there’s a quiet shift happening in the world of fund management, with more people clamoring for lower fees on all kinds of funds, including CEFs like those we recommend in my CEF Insider service, whose portfolio yields 9.0% today.

There are three driving forces behind this trend.

The first comes from activist investors like Boaz Weinstein, who believe certain CEFs have underperformed due to too little market discipline and have started clamoring for lower fees to shrink these CEFs’ discounts to net asset value (NAV, or the value of the assets in their portfolios).

Lower fees would indeed attract more investors and add to the momentum of already-shrinking CEF discounts. Already, these discounts have narrowed from their all-time low of 11.5% on average in November to a more reasonable 9.7% today. But that’s still far from the long-term average discount of 5.6%.

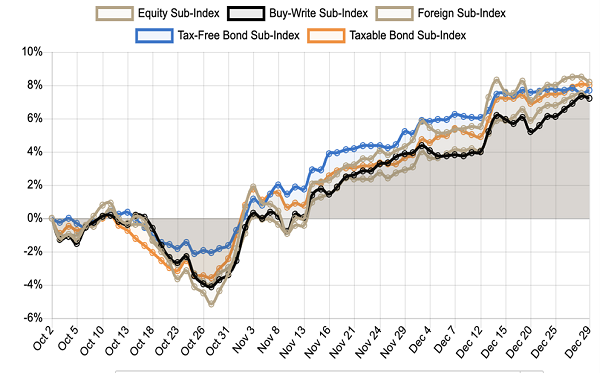

You can see those closing discounts already starting to drive CEF returns higher across all CEF subsectors tracked by CEF Insider:

CEF Recovery Just Beginning

Source: CEF Insider

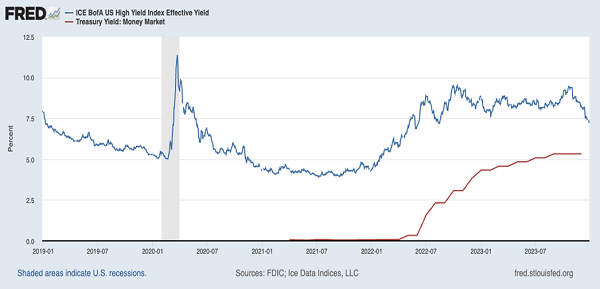

Next up is the fact that higher interest rates generally make bond CEFs more appealing. But that said, there’s still $6 trillion sitting in money-market funds today that could go into bond funds instead, according to Bloomberg and BlackRock.

The reason why that hasn’t happened yet is a sharp rise in rates paid out on money-market funds, as you can see in the red line below.

Income From “Safe” Money-Market Funds Closes the Gap on Bonds

The blue line, meanwhile, is the average yield on high-yield corporate bonds. The smaller gap between the two means corporate-bond CEFs need to offer more incentives to attract investors. And lowering fees is one obvious lever they can pull here.

It’s already happening: BlackRock recently waived part of its management fee on its iShares Broad USD High Yield Corporate Bond ETF (USHY) in response to higher price competition from other firms that started last summer. More fund managers will likely follow suit rather than risking seeing investors’ funds flee to cheaper alternatives.

Either way, this situation works to investors’ benefit.

There’s a third reason why funds are likely to get more appealing that doesn’t have to do with fees to fund managers, but instead “fees” (taxes, in other words) paid to the federal government.

I’m talking specifically about capital gains tax, which can be high for high-income earners and thus are something these funds, which are in the market of attracting wealthy individuals, try to avoid. Fortunately, ETFs are increasingly using (perfectly legal) accounting moves where they swap shares of companies for shares of ETFs and back again to minimize tax payable. That, in turn, is lowering taxes for everyone.

A 20%-Discounted CEF Set to Gain as Fund Fees Fall

With lower fees likely, and CEF discounts likely to close as a result, now is a good time to buy a CEF with an unusually deep discount, then “ride along” as that discount returns to normal (with an assist from lower fund fees!), propelling the fund’s market price higher.

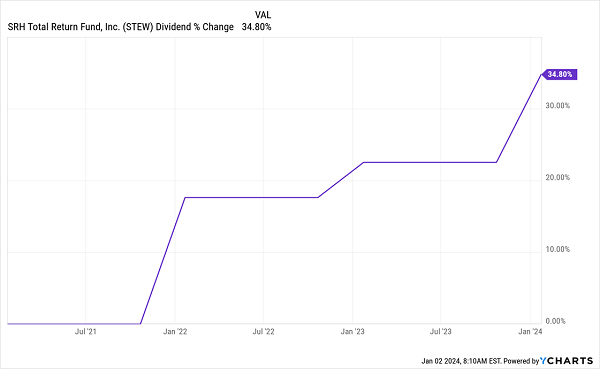

Take, for instance, the SRH Total Return Fund (STEW), a value investing–focused CEF with a $1.7-billion portfolio of sturdy large caps like Berkshire Hathaway (BRK.A), JPMorgan Chase & Co. (JPM), Yum Brands (YUM) and Cisco Systems (CSCO).

The profits from these stocks support STEW’s dividend, which yields 4%. That’s admittedly a bit low for a CEF, but STEW makes up for it with a payout that’s been climbing swiftly in recent years:

STEW’s Dividend Arcs Higher

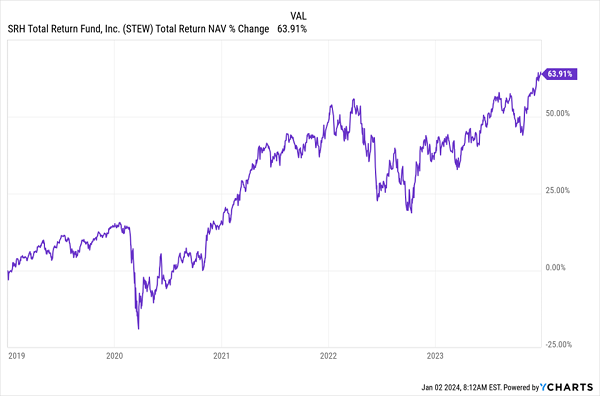

And if we do see another pullback in 2024, that’s just another reason to buy more: STEW survived the last two bear markets and came out stronger. And the fund kept growing payouts the whole time.

STEW Keeps Growing Investors’ Wealth

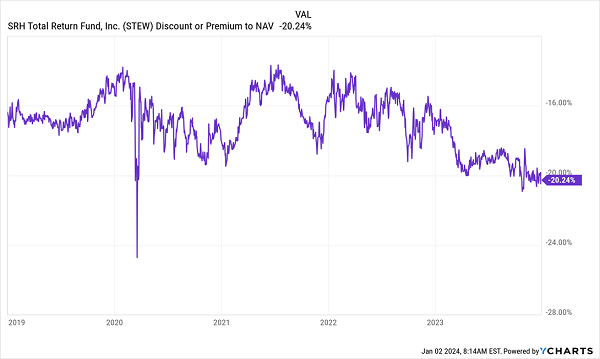

Up till now, STEW’s rising market price and dividend growth have been overlooked, resulting in one of the fund’s largest discounts in the last five years. In fact, STEW is now roughly as cheap as it was in the darkest days of COVID-19.

STEW’s Deep Discount Is Overdone

This points to an opportunity to buy STEW while it’s still oversold and sell at a profit when the market comes to its senses. An equally appealing option: buy at this historically deep discount, then hold for the long term and collect the growing payouts.

Let’s “Tack on” a Monthly Dividend (Yielding 9.2%) to Go With Our Gains

Plenty of CEFs not only pay high—and growing—dividends, they also shovel payments out the door every single month.

Many of these stout monthly payers are cheap now—and like STEW are primed for gains as discounts return to normal levels. My top 5 monthly paying CEFs, for example, yield 9.2% now and sport deep discounts, setting them up for strong gains in the next 12 months.

Click here and I’ll tell you more about all 5 of them and give you the opportunity to download a FREE Special Report revealing their names, tickers, yields and more. Don’t miss the chance to get onboard now, before the fee-slashing trend catches on and starts pushing CEF discounts closed—and prices upward.

Recent Comments