It blows me away that folks still think high interest rates will be around forever. Truth is, rates are already starting to fall!

But no one’s really paying attention (yet!). Which leaves us a brief window to lock in some sweet 8%+ dividends from one of our favorite utility-focused funds. This bargain-priced buy soars when rates drop.

Look Beyond the Headlines for the Real Rate Story

Remember January, when all the talk was about how rates would be cut six times this year?

Poof. Those hopes were history before winter—such as it was—ended.

Nowadays, futures traders have almost completely thrown in the towel—they’re calling for just two rate cuts between now and January.

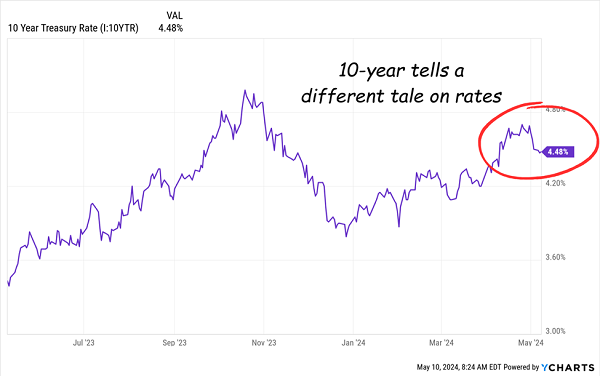

Here’s what everyone’s missing, though: Despite the hype, interest rates—here I’m talking about the “long” end of the yield curve, as dictated by the yield on the 10-year Treasury note—are still well below last October’s high. And they’re falling:

A few days ago, I wrote that rates weren’t spiking but were instead putting in a “lower high” and were likely to roll over.

This is exactly what’s happening.

Look, we can argue over whether the 10-year leads the Fed or vice versa. But the overall trend is toward lower rates as the labor market slows. There’s evidence for that, too: Last Thursday, the Labor Department said weekly jobless claims hit 231,000, up 22,000 from the previous week and well above expectations.

What’s more, Jay Powell, despite his tough talk on keeping rates high, wants nothing to do with another financial crisis, a la March 2023.

So he’s been quietly pumping liquidity into the market through “Quiet QE,” which we delved into a few days ago.

To sum up, here’s what we’ve got on our bingo card:

- Fearful mainstream investors.

- A nervous—and “quietly” dovish—Fed.

- A slowing job market.

- Rates topping, and rolling over—and still well below their October 2023 highs.

Add that all up and you get a sweet buying opportunity, especially in assets that trade inversely to rates.

Utilities Are a Sweet Contrarian Pickup Here

Utilities are near the top of that list.

They’re in the sweet spot because as rates fall, folks who’ve been parked in Treasuries will look elsewhere for yield. And they’ll find utilities, famous for their stable payouts, very attractive—just as they have every time rates have fallen throughout history.

These companies’ rising profits will sweeten the deal: As rates fall, these firms’ borrowing costs will, too.

That, in turn, will give them the leeway to invest in new generation and distribution capacity as electricity demand surges. And make no mistake, despite a slowdown in EV-sales growth, the energy transition is on. According to the Energy Information Administration, global electricity demand will jump 30% to 76% from 2022 levels by 2050.

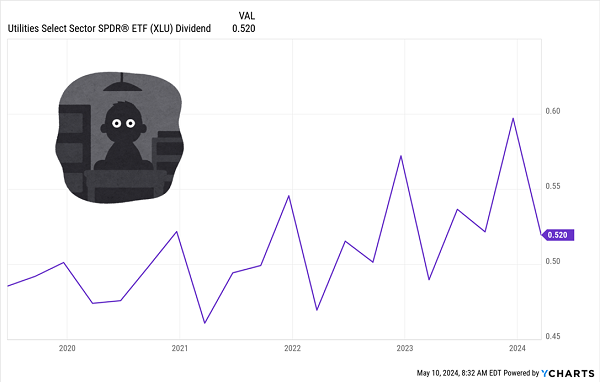

Trouble is, when most folks target a sector like utilities, they limit their returns right off the hop by picking up a fund like the Utilities Select Sector SPDR ETF (XLU).

It sounds like a great setup: XLU is a “one-stop shop” that tracks 31 key utility names, like NextEra Energy (NEE), Southern Co. (SO) and Duke Energy (DUK). Trouble is, we’re only getting a 3% current yield here—and it flickers more than a dusty old lightbulb.

XLU Suffers a “Dividend Brownout” …

That’s a lot of inconsistency to put up with for a 3% yield! It’s why we’re going to flip the switch over to a steady power stream (with a gaudy 8.1% yield) instead:

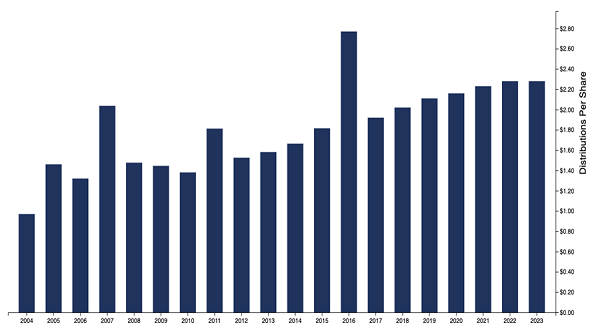

… While UTG’s 8.1% Dividend Powers Up, Year After Year

Source: CEF Connect

That’s the dividend chart of a closed-end fund (CEF) called the Reaves Utility Income Fund (UTG), whose portfolio holds major US utilities like Alliant Energy (LNT) and Entergy (ETR), plus a dash of international exposure through Deutsche Telekom AG (DTE).

Here’s something the chart above doesn’t show you: UTG pays dividends monthly. Right now, for example, investors are pulling in 19 cents a share every month, or $2.28 a year. That, of course, works out to around 8.1% of the fund’s $28 share price.

Here’s another reason why most folks pick an ETF like XLU over UTG: If you look up UTG on your favorite free stock screener, like Yahoo! or Google Finance, you’ll likely see a chart like this:

Price-Based Screeners Make UTG Look Like a Dud …

Source: Google Finance

This chart, from Google Finance, shows UTG’s performance since its February 24, 2004, inception to this writing. Tough to make out the share prices here (another flaw of free screeners!) but it amounts to a roughly 56% gain—in 20 years.

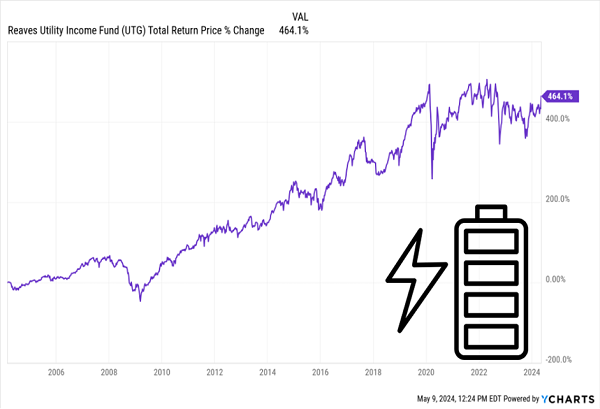

That looks pretty pathetic, But what it really reveals is a major pitfall of using free screeners with a CEF: these tools only show price returns, and CEFs, which yield around 8% on average, deliver most of their returns as dividends.

Add those payouts back in and you can see that, yes, this 20-year-old fund has more than delivered—with almost a 464% total return in that time:

… Until You Add the Payouts Back In

There’s one other plus here you won’t get with an ETF, and that’s the fact that CEFs’ share counts are more or less fixed throughout their lives. That means they can trade at levels different from their portfolio values—and often at discounts.

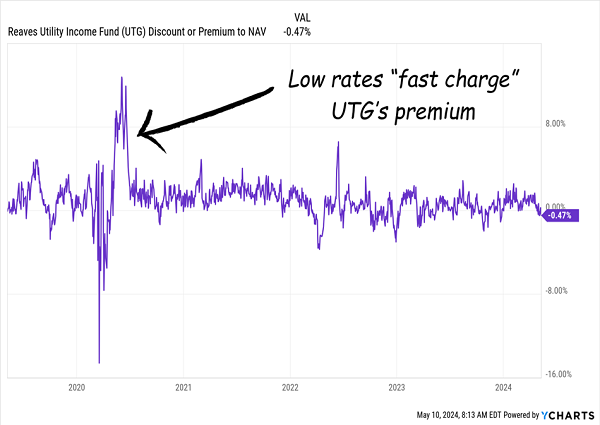

I grant that this isn’t the most compelling case for UTG on the surface. As I write, the fund trades at a mere 0.5% discount. But with UTG, as with all CEFs, it’s the discount trend that matters:

As you can see, UTG rarely trades at discounts and usually trades at big premiums in lower-rate periods. It also traded at a 13% premium, in the low (effectively zero) rate environment we saw in 2020 and 2021.

In other words, UTG trades at a fair value now, giving us a chance to get in before rates fall and its premium makes a comeback. Then we can either take profits and move on or stick around and enjoy our 8%+ yielding monthly payouts.

Buy UTG Now—Then “Tack On” These 3 Bond Funds Yielding Up to 12%

Most folks miss out on utilities because they see the sector as “boring.” But with rates rolling over and the “electrification of everything” marching ahead, that won’t be the case in the coming years.

Truth is, utilities are about to make their way onto more mainstream investors’ radar. And by getting in now, we’ll be nicely set up to go along for the ride!

They aren’t the only “boring” corner of the market due to spike higher as rates drop, either. Another one is corporate bonds, which also trade opposite the yield on the 10-year.

As I’ll show you in this exclusive investor report, it won’t take much, either, with a mere 1% drop in rates resulting in potential 15% annualized gains in corporate bonds.

As with utilities, our top bond plays are closed-end funds, due to the huge yields and discounts they provide. Right now, my top 3 corporate-bond picks yield up to 12%. And yes, they pay dividends monthly too.

The time to buy is now, before this boring sector, like utilities, starts grabbing the crowd’s attention.

Recent Comments