Remember when the Federal Reserve stopped printing money for a few months? It didn’t go well.

Yes, I’m making fun. A bit. Chairman Jay Powell did abstain from his printing press for nine full months.

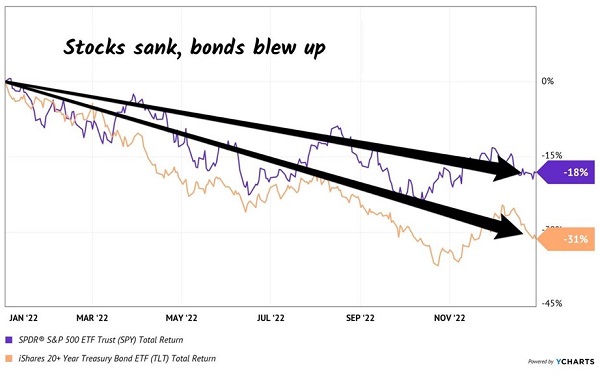

The year, as you’ll recall, was 2022. Headline inflation topped 8%. Eight! Jay, who had been blaming every supply chain from here to Shanghai for the price pressures, ran out of excuses. He held down the power button on his money printer for a hard reset.

Stocks sank 18% that calendar year. Bonds did worse—they completely blew up. A perfectly “safe” fund of US Treasuries, iShares 20+ Year Treasury Bond ETF (TLT) was anything but, shedding 31%.

The Fed’s 2022 Fling with Fiscal Tightening

Note that we were not in a recession. In fact, we still have not seen a slowdown. Which reinforces the fact that the stock market and the actual economy are two different creatures.

Bull markets feed on liquidity. Dinero. Moola. Straight cash, Homey.

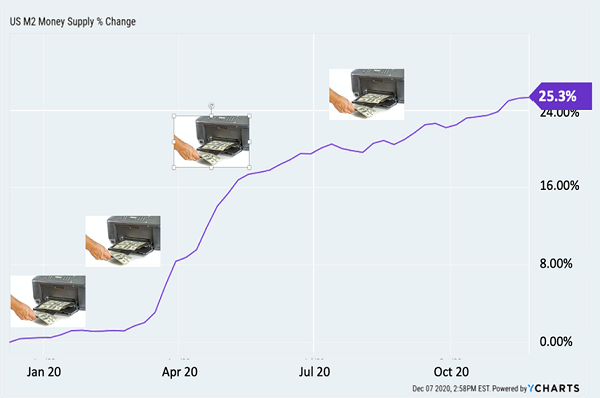

Think back to April 2020. We’re all cooped up in our houses. The fortunate ones—your income strategist included—posted up in Puerto Backyarda.

Things sure had that “end of the world” feel. N95 masks everywhere. The sound of helicopters over Backyarda as the eye in the sky kept tabs on nearby protests.

Yet the stock market didn’t mind one bit. In fact, prices were going parabolic! If the world was ending, well, the Nasdaq was shooting for the moon. Wow, did profitless tech stocks ever soar.

The catalyst? Jay’s money printer, which sent the M2 money supply soaring—up 25.3% year over year!

The 2020 Money Party

This out-of-control liquidity led to wild inflation in 2021. Which forced the Fed into austerity in 2022.

Yet Jay didn’t actually keep the money spigots tight for 12 months. He slapped the panic button after nine.

September 2022 scared the Federal Reserve and central banks in general. That’s when the UK gilt (Brit-speak for bonds) fell out of bed.

UK pension funds were levered up—used borrowed money—on “safe” gilts, in the same way that US pension funds lever up on US Treasuries. Problem is, gilts began to implode when US liquidity dried up.

The UK bond market is not nearly as big as the US Treasury market. When central banks tighten, the shallower pools of capital feel it first. So, gilt prices fell off a cliff and the jolly ol’ Bank of England rushed to support gilts the only way it knew how…

…by buying them with newly printed money!

The US Fed took note and took its foot off the financial brake pedal. Stocks and bonds figured this out quickly and bottomed immediately. (As always, nobody realized it at the time—mainstream pundits continued to call for more pain!)

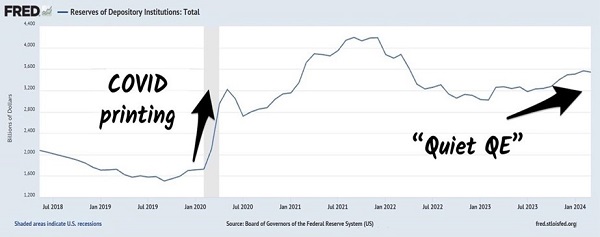

Six months later, in March 2023, regional banks began to fail fast and furiously. Higher interest rates had hurt the value of these banks’ “safe” collateral, US Treasuries. (Like all bonds, their prices drop as interest rates rise.)

A run on the banks. The pundits were right! Right?

Wrong. That panic ended the Fed’s supposed balance sheet tapering. Bank reserve levels (cash kept in case depositors want to withdraw), which had been in freefall since the start of 2022 when the Fed began tightening, stabilized.

A new bull market began as the Fed quietly began funneling money into the financial system. Quiet QE.

US Bank Reserves

The result since? Gold—the original inflation hedge—has broken out to all-time highs. Bitcoin, the new school inflation play, is bonkers. All while stocks have simply ground higher.

Throughout history, stocks pull back. And then they push higher. Which means that dips, ultimately, should be bought.

My favorite stocks to buy in this environment are dividend growers. They reward us two ways:

- High-octane divvies are powered by strong profit and, usually, top-line numbers. They keep us ahead of inflation.

- These “hockey stick” charts attract the degenerate gamblers trend followers. We contrarians buy low and wait for these guys to buy high—sending our shares even higher!

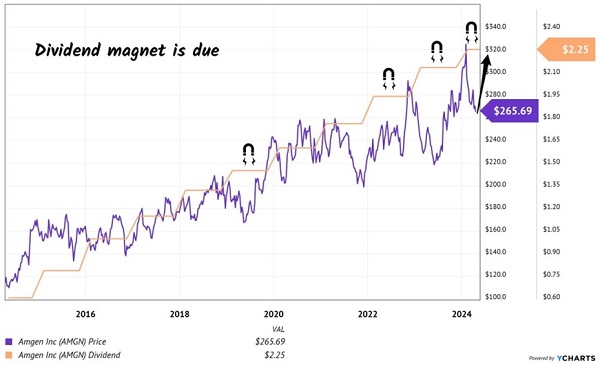

Here’s a recent example. Last month I recommended Amgen (AMGN) as a pullback play to my Hidden Yields readers. Over a long timeframe, Amgen’s price follows its payout higher like a devoted puppy dog. (Or an adolescent dog with the ability to focus more!)

My HYers and I considered the purple price line below, which always wanders and then races to catch up with the lovely and steady dividend staircase:

Amgen’s Always-Rising Payout (and Hence, Price)

We noted a bargain:

But for the moment, the tail seems to be wagging this pup. After topping on February 1, Amgen shares have pulled back nearly 19%. Nothing meaningful has changed—shares were a bit overheated then, and they are a bit undervalued now. Stock market hounds always overrun their mark.

We’re going to take advantage of this temporary mispricing.

Mr. and Ms. Market were missing key catalysts for Amgen: rare diseases. There are more than 10,000 of them identified today, but only 5% have approved medicines. As an established biotech, Amgen has the blend of research and development (R&D) and manufacturing know-how to bring these drugs to market.

Competition in rare disease treatments is low, and the addressable markets for these treatments add up. Since 2020, Amgen has boosted its rare disease product sales from $2.2 billion to $3.9 billion. This is the reason Amgen’s top line is accelerating:

Rare Disease Products Boost Sales

Now, does it matter to Amgen’s business if the Fed is tightening or printing? Not directly. But boy, does the AMGN share price appreciate the juice!

Since April Hidden Yields went to print, Amgen announced good test results for its potential weight loss drug. Jay Powell, meanwhile, verified what we knew all along—that the Fed would loosen, not tighten, from here.

The two ingredients created quite the cocktail—a quick 14% pop in Amgen’s price. And a congratulations to my HY readers who are sitting on these gains, which annualize to a terrific 274%.

Of course, Amgen is unlikely to return 274% over the next year. This blue-chip will take a breather at some point. Which is why we HYers will turn our attention back to the bargain bin, in search of temporarily discarded dividend growers.

After all, ‘tis the money printing season. Let’s not let mediocre economic numbers distract us. In fact, bad macro data can be good for stocks. Let’s not miss out.

If you missed the Amgen play, well, don’t let it happen again—subscribe to Hidden Yields here!

Seriously, we’re having a payout-grower party at HY and would love for you to join. With the Fed printing money and the economy holding up well enough, this is when the HY strategy really shines. Try HY risk-free for 60 days here.

Recent Comments