Let’s break out of today’s zero-rate wasteland and help ourselves to huge, safe payouts yielding all the way up to 8.3%. And these massive payouts are tax-free too!

And, no, we won’t be hiring a team of CPAs to pull this off—nothing so expensive and impractical. Instead, we’re going to set ourselves up with a closed-end fund (CEF) that holds municipal bonds, or “munis.” And thanks to their tax-free nature, if you’re in the top tax bracket, a muni bond paying, say, a 4% dividend could be worth 7% or more to you.

I’ll give you a specific CEF that’s worth putting on your list now in a second (its 5% stated yield could be worth an outsized 8.3% to you, if you’re in the top tax bracket). First, though, let’s break down a couple misconceptions that keep far too many investors from taking advantage of the huge, zero-tax dividends on offer here.

Debunking Muni-Bond Myths

Municipal bonds are just what the name says: bonds issued by essentially any kind of governing body, ranging from single hospitals to state governments.

Through municipal bonds, these agencies borrow money from the public, promising an interest rate in exchange for money they can use to build a new hospital, bridge or (in a lot of cases), pay out claims, pensions and other obligations.

Right now, there are an estimated $4 trillion of these bonds outstanding, and they’ve been generating steady returns, with little drama, making them a nice cornerstone for your income portfolio.

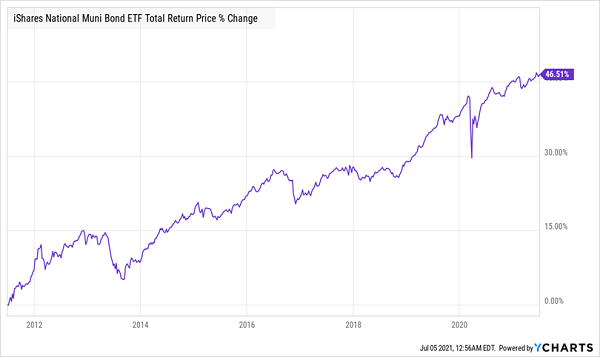

Steady Returns From Munis

With a 46.5% total return over the last decade, the muni-bond market has been a way to secure your wealth and get a reliable stream of passive income.

So why isn’t everyone in munis? One reason is an overblown fear of bankruptcies.

This is mostly a media-generated worry, because occasionally you’ll see headlines about a state or city running out of money. With a wave of baby boomers retiring, the need to pay out pensions to former state workers, and the drain on municipal accounts this causes, is a common theme that rattles nerves. Who would want to buy debt from states about to go bust?

There are two misconceptions here. The first is that, despite what many folks think, the odds of your muni-bond issuer going bankrupt are so low, they’re essentially at lightning-strike levels.

Overall, investment-grade municipal bonds have a 0.09% default rate, and A-rated bonds’ odds of default are 0.07%. In other words, you could buy a thousand of these bonds and chances are none of them would default at all. And if one did? You’ve still got 999 bonds that are paying your income stream with no worries.

Here’s another guardrail for your money: even in the unlikely event of a bankruptcy, municipal bonds go through a process where judges figure out how much money bondholders should get. In most cases, they get 80% or more of their initial investment back, and in some cases they get all of it.

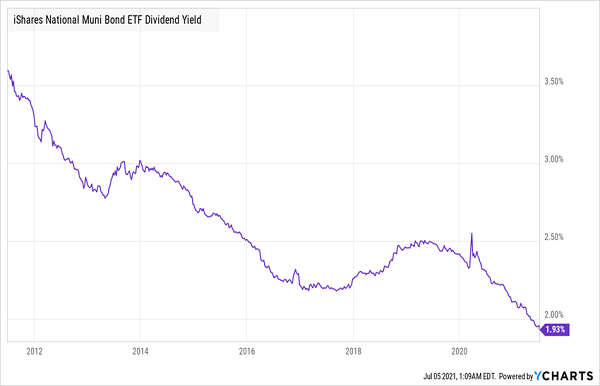

The other thing that keeps investors away from munis is that they look at the low yields on a benchmark muni-bond ETF, like the iShares Municipal Bond ETF (MUB), and dismiss them out of hand.

Low ETF Yield Doesn’t Tell the Whole Story

Even though MUB’s 1.9% yield is tax-free, that means it’s the same as just 3.1% of taxable dividends for people in the highest income bracket. As I mentioned off the top, we demand more—like 8% or more taxable (which, after taxes, is the same as 5% from tax-free munis).

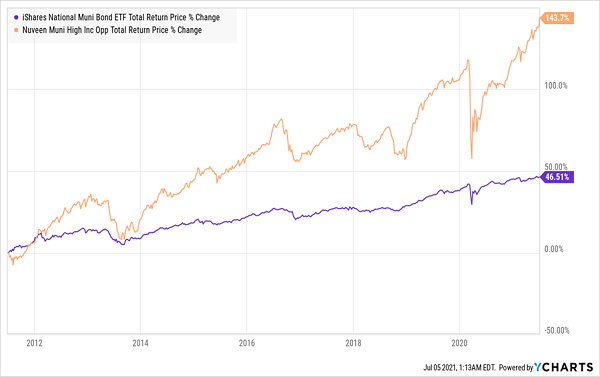

That’s why, instead of settling for MUB’s crummy yield, we’re going to look to the Nuveen Municipal High Income Opportunity Fund (NMZ), which yields 5% now, giving top-bracket investors the same income as an 8.3%-yielding stock, and with much less risk.

NMZ Crushes the Main Muni-Bond ETF

That’s why NMZ has tripled MUB’s return over the long term and shows no signs of stopping, all while paying us a monster income stream that comes with no tax bill at all.

The fund generates that income stream by holding a portfolio of municipal bonds that are rated BBB or lower. This works for us because this is where management can find higher-yield bonds at better bargains, because larger pension funds and other institutional investors are limited to investment-grade issues.

The fund’s managers are adept at working this space, which is how they’ve generated that 144% return—unheard of for a “boring” investment like munis—over the past decade. They also deftly spread the portfolio out across 687 different munis, ranging from issues by the Chicago O’Hare Airport to the state-run Kentucky Wired high-speed Internet network. This diversification further cuts NMZ’s risk.

These 7.3% Dividends (With 20% Upside) Are URGENT Buys Now

Strong as it is, NMZ didn’t make my list of the top high-yield CEFs out there today. That’s because it trades at a 5% premium to net asset value, so we’d be paying $1.05 for every dollar of assets it holds!

I see no reason to overpay when there are plenty of CEFs trading at big discounts now. So let’s keep an eye on NMZ and consider a move in when its premium flips back to a discount.

Meantime, I urge you to put any spare cash you have available into the 5 other CEFs I’ll show you right here.

These 5 terrific income plays throw off a 7.3% dividend between them, with the highest payer of the bunch handing you a gaudy 8%+ payout! Yields like that make a life-changing difference in retirement, or, if you’re not retired, give you a healthy hit of extra cash on the side.

But the real eye-catcher here is the gains on offer. As I hinted at a second ago, these 5 funds are all trading at massive discounts now—so much so that I’ve got them pegged for 20%+ price upside in the next 12 months!

So let’s say you drop a $100K investment into this 5-fund “mini-portfolio” today. Fast forward to this time next year and you’ll have collected $7,300 in dividends. Plus you could easily be looking at another $20,000 in price gains, too!

No S&P 500 stock can offer that kind of income and upside. And the time to buy is now, before these 5 funds’ bizarre discounts disappear.

Recent Comments