“America’s retirement fund” is looking awfully shaky. Income investors should consider replacing the over-owned S&P 500 index fund with these underappreciated yields up to 7.5%.

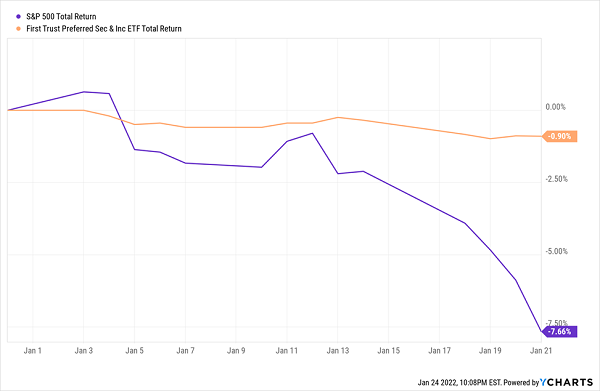

The S&P 500 has face-planted right out of 2022’s starting gate, flirting with a correction (that’s a decline of 10% or more) less than a month into the year.

If you’re retired, or thinking about retirement, these drawbacks are costly. They can erase years of hard work in a few bad trading sessions.

This is why we contrarians, who focus on cash flow, lean on “preferred” stocks, instead. These are special classes of shares issued by the same blue-chip firms in the S&P 500. But rather than pay 1% or 2% in dividends, these preferred shares yield 6% to 7% instead.

My Preferred Tactic for Retirement

Let’s use troubled Wells Fargo (WFC) as our example. The mega-bank cut its payout by a painful 80% in 2020, from 51 cents to a meager 10. It’s 20 cents now after a 2021 raise, but even then, this once-proud blue-chip dividend payer is only offering a meager 1.5% yield.

But see, that’s the dividend yield on Wells Fargo’s common shares.

What if I told you the very same company pays 5x that to certain other shareholders?

The 7.5% I’m talking about is the yield on one series of Wells Fargo “preferred stock.” These so-called stock-bond hybrids have a little bit of Column A, a little bit of Column B. They’re similar to stocks in that they trade on an exchange and they represent a little piece of ownership in the company. But they’re like bonds in that they often trade around a par value, and their “dividends” are actually closer to a bond’s fixed coupon payments.

They also have some pretty cool qualities of their own:

- “Preference”: Typically, preferred-stock dividends must be paid out before common-stock dividends, providing a little protection from being cut or suspended when the company goes through a financial rough patch.

- “Cumulative” dividends: In some cases, if a company misses a dividend payment on preferred shares, for any reason, it must pay preferred-stock owners those missed dividends before paying income to common shareholders.

- Huge yields. Most preferred funds offer several times more yield than the broader market right now. And just take Wells Fargo’s Series L preferreds, which yield a whopping 7.5%—more than 5x the S&P 500’s 1.5%! Most preferred funds will dole out between 4% and 7%.

Preferreds provide much-needed stability and high income when the wheels come off the market, like we’ve seen lately.

It’s Easier to Stay Cool With This Kind of Protection

But not all preferred funds are created equal. We can increase our profits and our payouts by looking past mainstream ETFs. Let’s skip past these pretenders for dividends up to 7.5%.

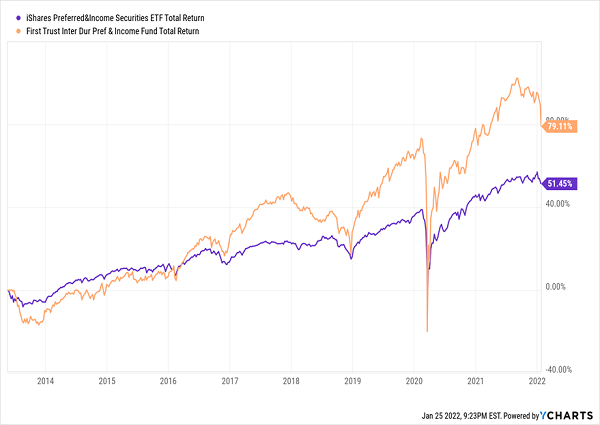

VANILLA ETF: iShares Preferred and Income Securities ETF (PFF)

Yield: 4.2%

The iShares Preferred and Income Securities ETF (PFF) is the biggest name in preferred stocks, at just under $20 billion in assets currently. Of course, part of that is simply from having been in the game so long—the fund launched all the way back in 2007. The other part is that PFF offers easy-to-understand exposure to a fairly niche asset class for a pretty reasonable price (0.46% annually). The ETF holds 500 different preferred shares, primarily of financial-sector stocks such as Bank of America (BAC) and Citigroup (C), but also industrials and utilities.

CONTRARIAN PLAY: First Trust Intermediate Duration Preferred & Income Fund (FPF)

Yield: 6.7%

The problem with PFF is that it’s a plain-Jane index fund that can only do what the computer tells it to. Conversely, what I like about CEFs is that their human managers still have autonomy, able to snap up value-priced preferreds and avoid overpriced ones while focusing on certain niches.

Take First Trust Intermediate Duration Preferred & Income Fund (FPF), which invests in preferreds with durations of between three and eight years. Thing is, while duration is pretty common when talking bonds, it’s not with preferreds—because most preferreds are perpetual and have no maturity. The idea here is to tamp down on interest-rate risk, which usually means you’re settling for lower income—but in this case you’re beating the pants off PFF because of the fund’s 30% or so in debt leverage, which allows FPF to double down on some of its bets.

The result? A little more “wiggle,” but generally far better returns over time.

A Clear Performance Advantage Over the Index

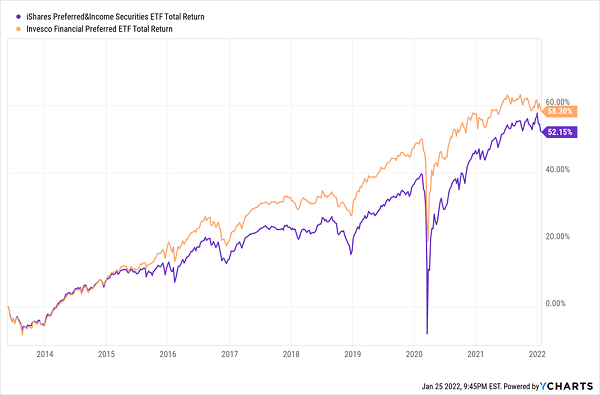

VANILLA ETF: Invesco Financial Preferred ETF (PGF)

Yield: 4.5%

So, the PFF is nothing to write home about. What about an ETF with a little flavor, such as the Invesco Financial Preferred ETF (PGF)?

Most preferred-stock funds are awash in bank stocks and insurers; typically, financials are the largest sector holding. But PGF puts that idea into overdrive, tracking an index that must invest at least 90% of assets into U.S.-based financial preferreds. This tight portfolio of just more than 100 preferred stocks is loaded with the likes of JPMorgan Chase (JPM) and PNC Financial (PNC), putting it in position to not just deliver a nice yield, but possibly modest price gains given financials’ favored-sector status in 2022.

Just don’t expect much. PGF has been a better fund than PFF over the long haul, but ultimately, they’re pretty similar animals.

An Index Fund Is an Index Fund Is an…

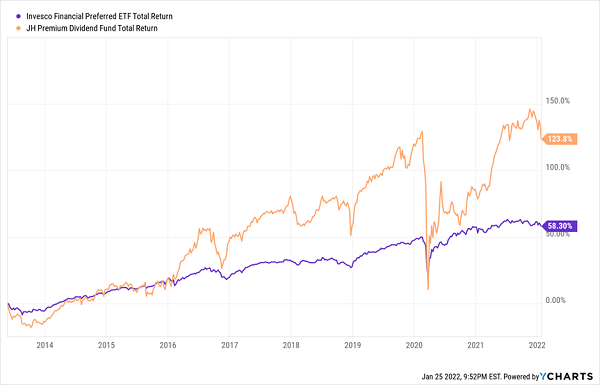

CONTRARIAN PLAY: JH Premium Dividend Fund (PDT)

Yield: 7.5%

If you really want something different, JH Premium Dividend Fund (PDT) delivers on that front—and it delivers results.

This miniature income-portfolio-in-a-can combines both preferred stocks and common dividend stocks to provide a very-high-yield solution that’s diversified and has better potential for upside appreciation than a typical preferred fund.

PDT doesn’t hold many stocks—just 105 presently—and it concentrates those bets even more thanks to 34% debt leverage. Also, the highest sector concentration isn’t financials, which are still substantial at nearly 30% of assets; it’s utilities, which between commons and preferreds make up just more than half the fund. Top holdings include NextEra Energy (NEE) and Dominion Energy (D) preferreds, as well as Williams Cos. (WMB) and Wells Fargo commons.

PDT is clearly more volatile as a result, but remember: You’re basically combining defensive blue-chip stocks with high-yield bond-esque assets.

JH Premium Dividend Fund Is a One-Stop Shop for Income

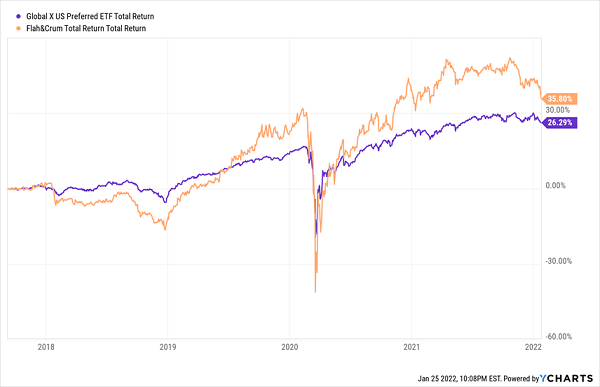

VANILLA ETF: Global X US Preferred ETF (PFFD)

Yield: 4.8%

If you want to take a relative swing for the fences, you could jump into the Global X US Preferred ETF (PFFD), a young-ish fund that got its start in 2017.

PFFD is one of the highest-yielding preferred ETFs at nearly 5% currently, and it’s pretty cheap, at 0.23% in annual fees. Credit quality is fine, with more than half the portfolio rated investment-grade, so it’s not going out over its own skis trying to produce an outsized yield.

CONTRARIAN PLAY: Flaherty & Crumrine Total Return Fund (FLC)

Yield: 7.3%

Of course, there’s nearly 5%, and then there’s over 7%, and Flaherty & Crumrine Total Return Fund (FLC) provides the latter. Even an ETF on the high end of the yield scale can’t top your average CEF, and it certainly doesn’t beat FLC—in more ways than one.

At Least, It Can’t Top FLC When It’s on a Roll

FLC is another hybrid portfolio. Flaherty & Crumrine is a preferred-stock specialist, and this closed-end fund mostly sticks to the firm’s strengths. Usually somewhere around 60%-75% of assets will be invested in preferreds, with the rest of assets dedicated to debt as well as “contingent capital securities.” Per F&C:

Contingent capital securities or ‘CoCos.’ have features similar to preferred and other income producing securities but also include ‘loss absorption’ or mandatory conversion provisions that make the securities more like equity.

A high 34% leverage ratio and slightly lower credit quality than your average preferred fund make FLC a bit of a bumpy ride. But the sheer income difference and advantages of active management in the space should mean continued outperformance for this CEF over the long run.

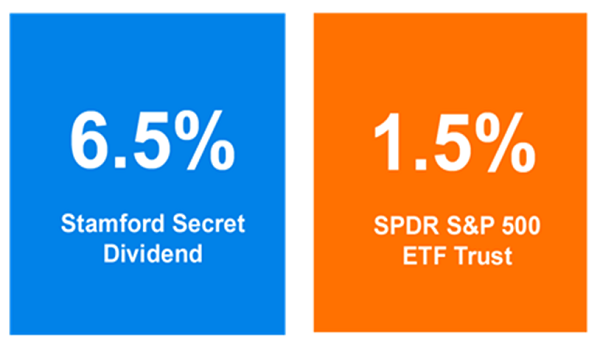

Mysterious “Stamford Secret” Dividend Plan Exposed

These three funds are sterling examples of how CEFs can generate so much more in profits than their more popular ETF cousins.

And that’s remarkable, given that they’re really just a “B” squad.

But right now, I’m far more excited about an A-plus-plus investment—a fund that we don’t often get an opportunity to buy at a discount, but that’s currently ripe for the picking.

If you’re looking for the perfect time to upgrade your retirement plan with an investment that could generate more than $32,000 annually on a mere $500,000 nest egg…well, stop waiting.

That time is now.

Recently, a 6.5%-yielding fund that I keep constant tabs on finally landed in our “Buy” zone, flashing a bright green light at investors.

This fund has a killer edge its competition can only dream of:

Its managers, an unsung duo from sleepy Stamford, Connecticut, get first crack whenever a new stock comes on the market!

You’ve always wondered what it would be like to buy Microsoft before its IPO. Or IBM. Or even Apple. Well, these guys can actually do it—in a fund that you can buy!

No wonder this low-key duo ALWAYS beat their benchmark. An “automated” ETF simply can’t keep up with these “ultimate insiders.”

Powered by this hidden advantage, their fund throws off a massive 6.5% dividend that dwarfs the payout on common stocks:

Huge “Stamford Secret” Dividend Reigns Supreme

This terrific fund is a “must own” for anyone looking for inflation-proof income, whether you’re in retirement or still building your nest egg.

I’m ready to share all the details with you now. Click here and I’ll give you everything you need to know about this amazing income play, including its name, ticker symbol, dividend history and full profiles of its high-powered management team.

Recent Comments