There’s a group of 7%+ dividends out there that are perfect for today’s market. They’re far less volatile than “regular” stocks, their payouts are tax-free, and (for now) you can get them for a steal—as cheap as 93 cents on the dollar!

That puts them high on the list of “refuges” from the speculative stocks the mainstream crowd is fleeing these days—and we want to make sure we get in first! (And we’ll do that with two muni-bond funds we’ll name below. Their tax-free yields could be worth up to 8.9% to you, depending on your tax bracket.)

I’m talking about municipal bonds—specifically municipal bonds we can buy through my favorite high-yield investment: closed-end funds (CEFs). (As you can probably tell from the name, municipal, or “muni,” bonds are issued by states, counties and municipalities to fund infrastructure projects.)

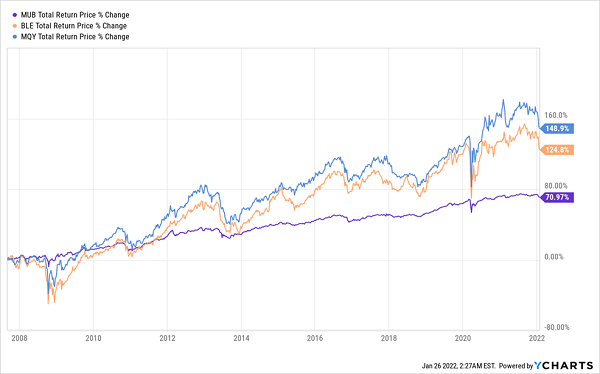

Also, it’s worth noting that both of the muni-bond funds we’re going to discuss made money during the rate-hike cycle, which ran from late 2015 to late 2019, as you’ll see in the chart of their long-term returns below. So if you’re worried about the Fed’s upcoming rate hikes hurting muni bonds, you don’t need to be.

What’s more, despite high-profile examples like Detroit and Puerto Rico, bankruptcies are nearly unheard of among munis: they have less than a 0.008% default rate—they’re that safe!

Make This Muni Mistake and You’re Guaranteed to Leave Money on the Table

When many folks buy munis, they take what they see as the easy route and buy the benchmark ETF for the asset class, the iShares National Municipal Bond Fund (MUB).

That’s a mistake, for two reasons: first, MUB yields just 1.9%. Sure, if you’re in the highest tax bracket, that equates to a 3.2% yield from taxable returns, such as payouts from stocks and corporate bonds, but it pales in comparison to dividends from muni-bond CEFs, many of which yield north of 5% before tax benefits.

Worse, many investors make the mistake of thinking actively managed funds like CEFs rarely beat their benchmark, so they’re better off saving themselves the fees and going with the ETF.

The trouble with that thinking is, while there’s some truth to it in stocks, it doesn’t hold up with smaller, more insular markets like munis. Here, savvy, well-connected human managers can get the inside track on the best new issues, which is something an algorithm-driven ETF could never do. This is why 90% of muni-bond CEFs have beaten MUB over the last decade, and none have lost money in that time.

And yes, that includes the two CEFs we’ll delve into now—the BlackRock Municipal Income Trust (BLE), in orange in the chart below, and the BlackRock MuniYield Quality Fund (MQY), in blue.

Our 2 Muni CEFs Lapped Their Benchmark

Let’s take a closer look at these “no-drama” income plays now.

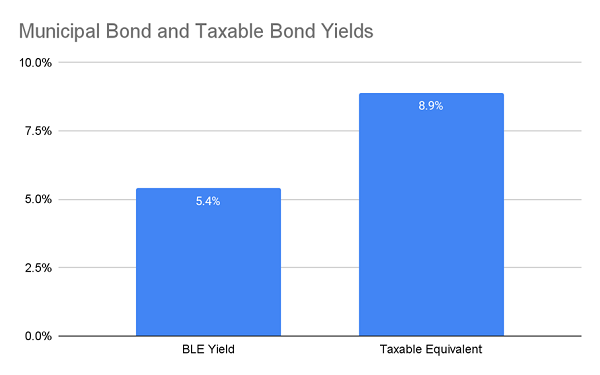

Muni-Bond CEF No. 1: An 8.9% Dividend Masquerading as 5.4%

The BlackRock Municipal Income Trust (BLE) invests across America and offers a 5.4% dividend yield. But the fund’s “hall pass” on taxes makes a big difference. For buyers in the highest tax bracket, that 5.4% yield is the same as 8.9% on a taxable-equivalent basis.

Source: CEF Insider

To say this fund’s portfolio is diversified would be a massive understatement. As I write, it holds 594 different bonds, leaving it very well protected against the already low odds of one (or even more) of its issuers running into financial trouble.

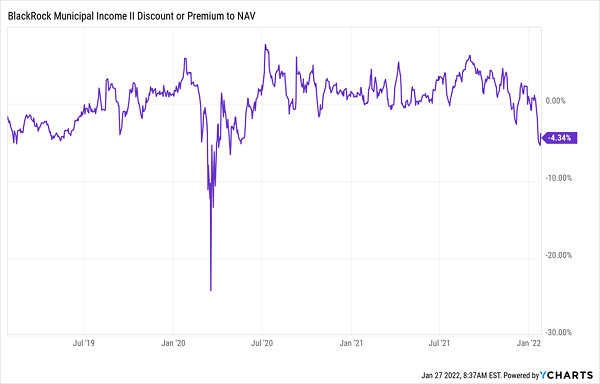

And there’s one more important advantage we get from a CEF like BLE: the discount to net asset value (NAV, or the value of the bonds in its portfolio). This measure, which only exists with CEFs, means that these funds often have market prices below their portfolio’s value.

The advantage of buying a CEF at a discount is twofold: 1) A wide discount is a good predictor of future upside as these markdowns snap back to more normal levels, and 2) A big discount helps hedge our downside, as it’s harder for an already cheap CEF to get a lot cheaper—we’ve got much greater odds that its next major move will be up.

And with BLE, we’ve got a chance to buy at a 4.3% discount, a level we haven’t seen since the March 2020 crash:

BLE Is on Sale

Muni-Bond CEF No. 2: The King of Diversification (for 93 Cents on the Dollar)

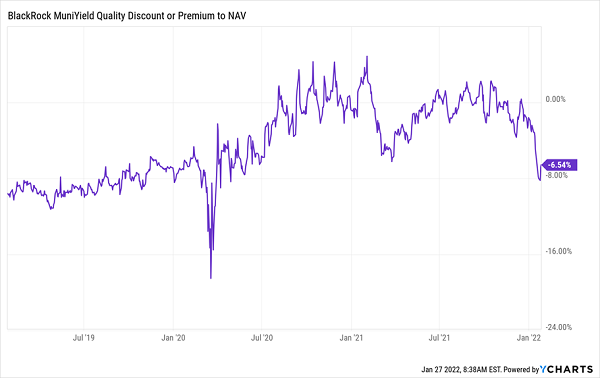

Our next CEF, the BlackRock MuniYield Quality Fund (MQY), yields 5.1% (or about 8.6% on a taxable-equivalent basis for a top-bracket earner).

MQY gives us even more safety than BLE, both due to its focus on higher-rated bonds and by the depth of its portfolio: the fund holds 767 different bonds in total. That’s as diversified as you can get in the least volatile asset class on earth (that’s no error—studies have shown muni bonds have less price volatility than all asset classes that don’t guarantee your principal, like a CD, for instance).

Better still, we can get MQY at an even bigger discount than BLE—6.5% as I write this. That, too, is the best deal we’ve seen on the fund since March 2020 and gives us a nice downside cushion (and upside potential) as it moves back toward more normal levels.

MQY Is Cheaper Than It’s Been in Months

Add it all up and with just these two funds you’ve got a nice opportunity for low-volatility upside, incredible diversification and dividends that won’t raise your tax bill. That makes these funds nice buys for high, tax-free income and gains as the rate-panicked crowd scrambles to safety.

This Rock-Solid CEF “Mini-Portfolio” Yields 6.9% (With BIG Upside)

Municipal bond CEFs, with their unbeatable stability and high, tax-free dividends are a great foundation piece for your portfolio … which is why I’ve dropped my top buy among municipal-bond CEFs into the high-yielding 5-CEF “mini-portfolio” I recently assembled.

These 5 funds are perfect for today’s uncertain market, handing you a big slice of your return in cash, thanks to the 6.9% cash dividend this mini-portfolio throws off. Plus these 5 funds are incredibly diverse: aside from municipal bonds, they hold blue-chip stocks, real estate investment trusts, top healthcare stocks and bargain-priced tech stocks, too.

What’s more, these funds are cheap now, setting us up for big upside as the income-starved crowd pours in to tap them for their steady, outsized payouts.

The kicker: four out of these five funds pay dividends monthly, so you won’t be waiting a full three months for your next payout to drop into your account!

Full details are waiting for you in the exclusive Investor Bulletin I’ve prepared for you. Go right here to read it and position yourself to start collecting these funds’ massive 6.9% dividend—with most of that cash coming your way monthly—today.

Recent Comments