It’s a piece of advice so common I’m sure you’ve heard it a million times. Too bad it’s dead wrong.

I’m talking about the so-called “wisdom” that index funds always beat funds with real, live human managers.

Before I get into why it’s wrong—and show you 10 smartly run funds that easily beat their ETF cousins (while dropping an unheard-of 7.5% average dividend into our laps)—let me explain the problem here.

First, I should say that there are cases where index investing makes sense. If you’re 20 years old and you’re putting 10% of your income into a retirement fund, planning to retire when you’re 60 and won’t touch your savings till then, index investing may work for you.

For just about everyone else, it’s wrong. A big reason why boils down to cash flow.

If you’re a retiree or nearing retirement, getting a 7% or 8% income stream from your portfolio is likely important to you. But index investors will tell you that this is impossible to sustain in the long run, because if you try that with a portfolio of index funds, you’ll quickly run out of money.

But you can get that kind of income much more easily with actively managed funds—many of which have been paying that amount out for over a decade, and some for much longer.

And when you get outside of regular stocks, things get really interesting. Because that’s where actively managed funds easily stand head and shoulders over the paupers of the index-investing world.

The best part? This is an opportunity that’s dead simple for us to exploit, starting with…

10 Index-Crushing Funds With 7.5% Cash Payouts

So let me show you those 10 funds I mentioned off the top—the ones that have beaten their benchmark index for more than a decade and pay a 7.5% average dividend yield, too.

For this example, I’ll choose preferred stocks—an asset class that’s very close to common stocks but also has a lot of elements of bonds. Most importantly, preferred stocks have a much higher yield than common stocks, which is how we can grab that fat income stream I just mentioned.

These 10 funds all have the same things in common, and they are the only funds that have these attributes. All 10 of these cash machines are:

- actively managed.

- focused mainly or entirely on preferred stocks.

- closed-end funds (CEFs).

- well-established, with histories stretching back a decade or longer.

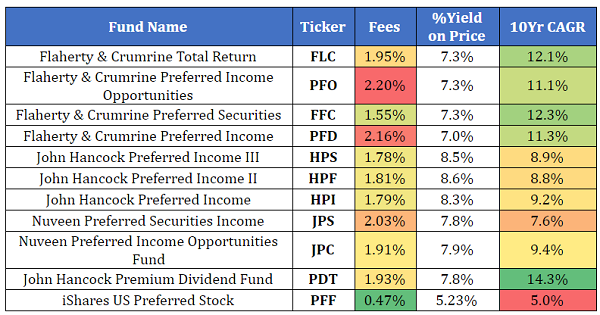

The 10 funds that match these 4 simple criteria have all beaten the preferred-stock benchmark, the iShares US Preferred Stock ETF (PFF), for over a decade. Take a look at the following table. You’ll see that it’s proof positive that the index-investing lie is just that—a lie.

Big Gains—and Dividends—From Human Managers

Let’s start with fees.

Notice that PFF is the cheapest by this measure, boasting fees that are less than a third of those on the cheapest actively managed fund here. And 3 of these funds have fees over 2%!

The passive index-investing aficionado would scoff at such fees and pat themselves on the back for choosing PFF, the “cheaper” option.

And in doing so, they would lose a lot of money.

First, let’s emphasize that the returns these funds gave investors are all after fees, and we are comparing total returns (capital gains and dividends) for all funds, so this is a truly same-basis comparison.

Now notice the “10Yr CAGR” column, which shows the average annual return of each fund over the last decade. The “dumb” index fund has given investors a 5% return over that time—less than two-thirds of gain on the lowest-performing actively managed fund (JPS), which is up 7.6% over the last decade.

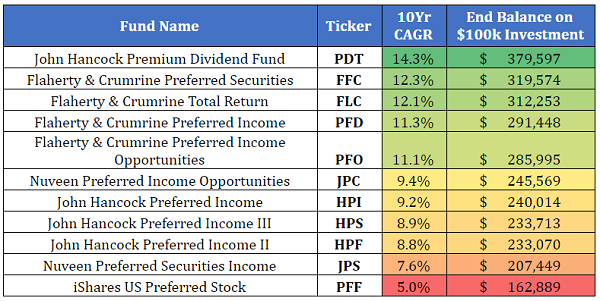

Let’s put some numbers behind this: $100,000 in PFF would be $162,890 after a decade—while JPS would give that same investor $208,030. That’s right, the “smart” index investor lost out on $45,140 by betting on the index fund!

And that’s the worst active fund.

Take a look at the profits the passive investor missed out on by choosing PFF over these actively managed options.

In the most extreme case, the investor missed out on $216,707—over double the initial investment! Even the investor who didn’t know which active fund to pick and simply put $10,000 into each one would have ended up with $274,868, or over $111,000 more than the PFF index investor.

If that’s not proof that an active approach crushes a passive one, I don’t know what is.

Just Released: 5 More 8.2% Dividends Wall Street Hides From You

Just last month, I released my 5 hottest CEF picks to buy now—and I’ll share them with you when you click here!

These 5 actively managed superstars have a lot in common with the 10 funds we just discussed, but with one crucial difference: unlike the 10 preferred-stock funds I just showed you, these 5 red-hot CEFs are all on my personal BUY list now.

Each of these funds throws off safe, and massive, dividend payouts—I’m talking an average 8.2% in CASH, with one of these beauties even handing you an outsized 10%!

Imagine what that would do for your retirement portfolio.

There’s more, though.

Because each one of these payouts is SAFE. And thanks to these funds’ massive discounts to net asset value (NAV, or the market price of the investments in a fund’s portfolio), we’re looking at a nice 20% price gain in the next 12 months, on top of that life-changing income stream!

To put that in dollars and cents, putting $400,000 into these funds today would immediately kick-start a $32,800 yearly cash stream. PLUS you’d be set up for a nice $80,000 in upside.

And because you’re getting a big chunk of your return in CASH, you’ve got some nice insulation from volatility here, too.

Wall Street: “Pay no attention to the man behind the curtain”

Funny thing is, you won’t hear a whisper about these obscure wealth builders from Wall Street. They’d much rather steer you into an ETF, like PFF or the SPDR S&P 500 ETF (SPY).

It’s a lot easier for them, because they don’t have to do a smidgen of research, and they get paid anyway.

That’s great for them, but terrible for you. And it’s exactly why I’ve rolled out these 5 incredible 8.2%-paying CEFs now.

I can’t wait to show them to you. All you have to do is CLICK HERE to get instant access to the name, ticker symbol, buy-under price and my complete research on each of these 5 cash machines!

Recent Comments