“Do you have cherries?” my buddy Ralph asked over the phone.

It was January 2021. Sports bars here in California were closed, so we naturally turned our backyard into one.

“No,” I replied. And sighed in an honest admission. “Only beer. Lots of beer.”

“No problem. I got ‘em.”

My buddy also had a mini-keg of delicious old-fashioneds. His creations were dangerously delicious. He’d begun making and aging fine adult beverages to pass time in the pandemic.

And the maraschino cherries he brought played no small role in his cocktail’s critical acclaim.

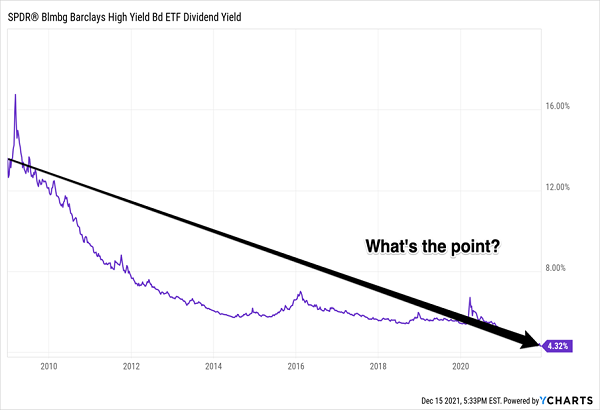

Is it five o’clock yet? Just kidding (mostly). We are talking about maraschinos in a dividend column because we finally have some bond funds worth cherry picking.… Read more

Recent Comments