Last time we had a July like this, REITs (real estate investment trusts) ran wild. The top plays delivered dividends plus price gains between 40% and 114%!

REIT Rhyme for 114% Returns?

Tell me if this sounds familiar:

- It was July,

- The stock market was hitting all-time highs,

- And the Fed was about to cut rates for the first time in a while.

We shall see if July 2019 continues to “rhyme” with July 1995. Back then, we had Fed Chair Alan Greenspan introduce the concept of the “Greenspan Put,” the inside joke that the Maestro would save any decline in stocks with rate cuts.

This time around, we have Jay Powell’s 180-degree “pivot” from hawk to dove. Whether he learned to listen to the markets, or the guy simply wants to keep his job (the President was pressing him to lower rates), he’s going to be the first Fed chair since Greenspan to cut rates with stocks soaring.

Overall, this is bullish for REITs, which benefit from:

- A strong overall economy (check!), and

- Easy money (check!).

The mainstream financial media lazily harps on number two (and only rule two), that falling rates are good for REITs and rising rates are bad. This is true in a vacuum, but we invest in the real world.

While these firms do tend to benefit from cheap money being available (because they often use debt to fund acquisitions and growth), it is more important that the rent checks are coming in on time. These are the cash flows that are directly passed on to investors as dividends.

With a healthy-enough economy today, this is a Goldilocks environment for many REITs. Business is good (because their tenants’ businesses are good) and money is cheap and getting cheaper. Check and checkmate!

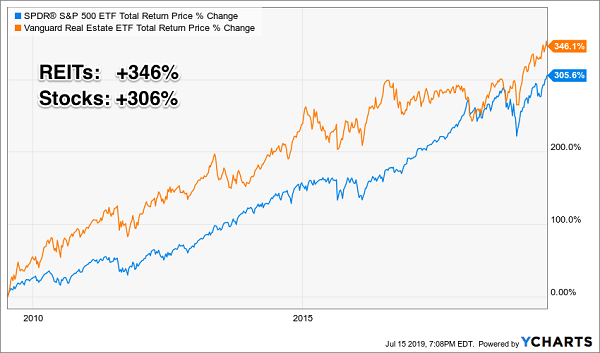

Thanks to their generous payouts, these REITs already tend to outperform their product-peddling peers. Over the last decade, Vanguard’s Real Estate ETF (VNQ) has outpaced the S&P 500 at-large:

Landlording’s Been Better Than Business

Of course, it’s easy enough to improve on VNQ, being the simple ETF it is. In fact, it’s very possible to double your money with REITs in short order. The secret is focusing on the firms that are most likely to increase their dividends in the years ahead.

Which means their stock prices will follow. Dividend growth REIT stocks have wonderful “built in” capital appreciation potential because their share prices rise as their dividends climb.

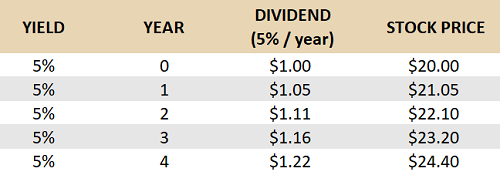

Let’s map out the case of a REIT dividend grower with some round numbers to make the math easy. We’ll say the stock is a 5% payer growing its dividend by 5% per year. Its current yield (left column) stays constant amidst the dividend growth because its stock price (right column) rises along with its dividend:

We can identify the REITs most likely to increase their dividends simply by finding those with FFO (funds from operations) growth. FFO represents the amount of cash a REIT actually generates from its operations. It’s where our dividend originates – which makes it the building block for everything else in the REIT world.

To calculate FFO, we start with net income. Then we add back depreciation and amortization (which are accounting expenses) and subtract profits from property sales (which are one-time events).

FFO is the driver of dividend growth for REITs. Figure out where FFO is going, and you know where the payouts are heading – and how fast.

If FFO is stagnant, a firm can only increase its payout by increasing its payout ratio. And this isn’t sustainable over time.

Rising FFO on a per share basis, on the other hand, will basically force management to raise its dividend. And that’s what ultimately drives the stock price higher, because dividend growth is all that matters for REITs. Figure out where the dividend is going, and you know where the stock price is heading.

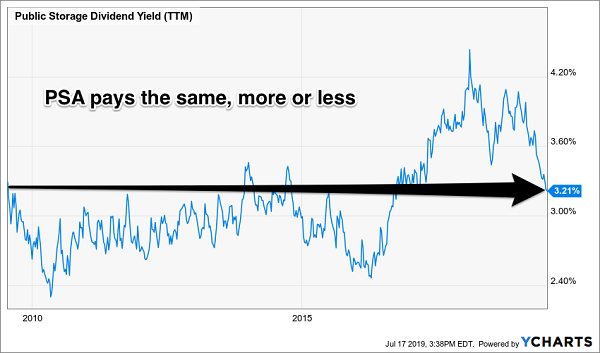

Reason being, REIT yields are relatively consistent over time. For example, blue chip self-storage name Public Storage (PSA) pays exactly what it did 10 years ago:

PSA’s Payout: Same As It Ever Was

But be careful – just because the current yield goes nowhere doesn’t mean the stock price goes nowhere. In fact, it’s quite the opposite.

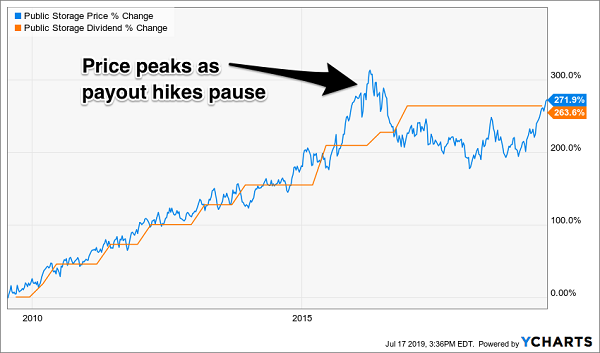

Over the last ten years, PSA has increased its dividend by an impressive 264%. Its stock has followed suit, delivering 272% total returns to shareholders!

PSA’s Dividend Drives its Stock Higher

Why’d the stock peak back in 2016? Simple–the dividend plateaued then. Without the promise of a higher payout, there was no catalyst to drive the stock price higher.

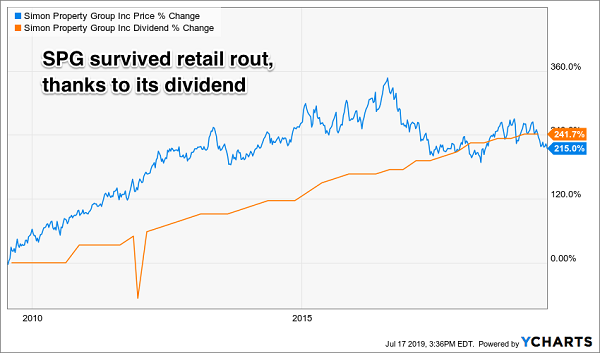

A-list retailer Simon Property Group (SPG), a mall REIT, has likewise been able to withstand much of the recent retail rout thanks to its rising dividend:

Simon Says: Higher Payout, Higher Prices

REITs can be excellent yield vehicles. But why not buy them for growth too? It is possible to have your dividend and enjoy price upside to boot – and it all starts with rising FFO.

PSA and SPG were good buys a decade ago, but their dividend growth has slowed. Fortunately, we have two REITs that we should focus on instead. Combined they yield up to 8.9% and they are likely to double their already-generous dividends in the years ahead. Which means their stock prices should double, too!

2 Urgent REIT Buys for 100%+ Gains and 8.9% Yields

I just completed my research on these two urgent REIT buys, and I’d like to email it to you now. These payouts are simply “going parabolic” and it’s important that you add these stocks to your retirement portfolio before their prices run away from us.

With Powell’s hand on the easy money spigot, it’s best to buy these stocks this week–before his doves cry to the financial media again. It won’t take much to send these growth REITs soaring. Please read through my 2019 REIT Playbook here to receive my full analysis on these urgent REIT buys with 114% upside.

Recent Comments