Well, that escalated quickly.

We contrarians have been ready for rising interest rates—and long-term rates have indeed begun the year with a moonshot.

The Federal Reserve has been a big buyer of US bonds since the spring of 2020. If it weren’t for this “whale” buying $80 billion in bonds per month, long rates would likely be higher already.

How much higher is anyone’s guess. But now that the Fed is “tapering” its monthly purchases from $80 billion all the way to zero, everyone is rushing to place bets. And income investors are speculating that a fair rate for the 10-year is higher than here.

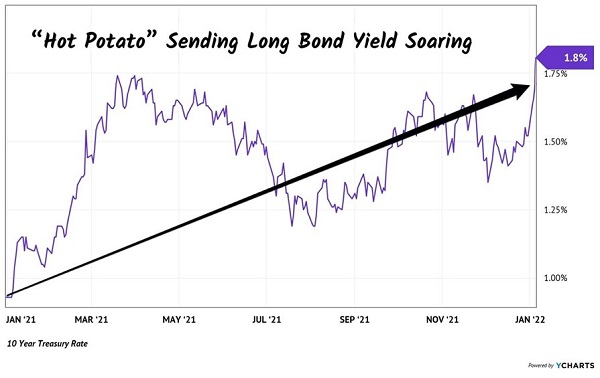

What a difference a year makes! In these pages exactly one year ago, we chatted about the likelihood of a rising 10-year Treasury rate. The benchmark yield had just cleared 1%. It eventually closed the year at 1.5% and, as I write, we’re already staring at 1.8%.

Nobody Wants the 10-Year Treasury

On a historical basis these rates are still low. But on a relative basis they’re a runaway train.

And hey, when it comes to making money in the stock market, it’s all relative.

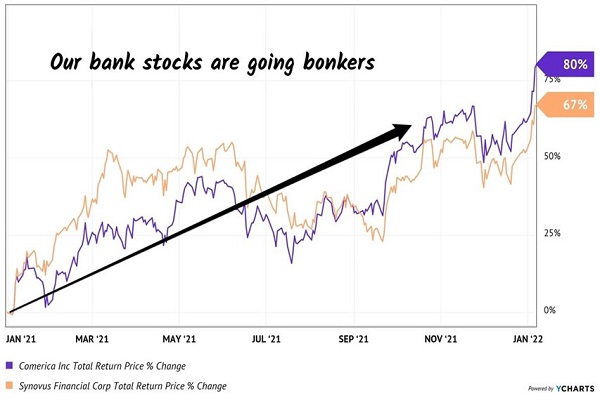

Take bank stocks, which are fun to own as long rates bounce. My favorites are the smaller, regional banks with the traditional banking model of “borrowing short and lending long.” The booming long rate drops right to the bottom lines of these banks.

These banks are still able to borrow for cheap, with short-term rates nailed to the floor. Meanwhile they’ve been able to lend for more, with long rates up a cool 80% over the past year. The “spread” between short and long rates is pure profit.

Many of these stocks entered last year as “coiled springs.” Small banks have had a rough last decade or so, with long rates stuck in the basement. But things have gotten a lot better over the last 12 months.

Their stock prices are already moving higher. If this keeps up, we’re going to see some serious dividend raises from this sector, too.

Shout out to my Contrarian Income Report readers, who have rolled with small banks Comerica (CMA) and Synovus (SNV). We identified these as two of our favorite dividends for rising rates and they have not disappointed:

Two of Our Favorite Dividend Stocks

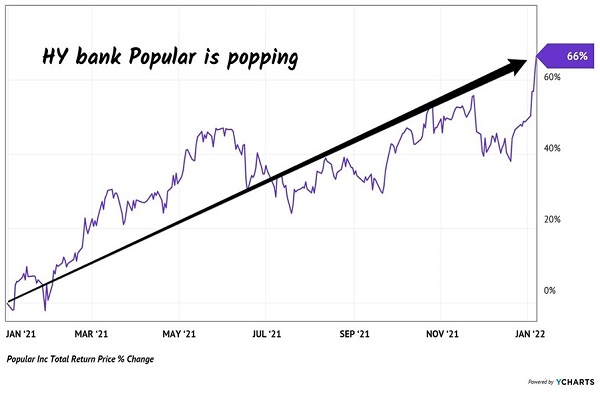

Our dividend growth service Hidden Yields has also been big on financial payers that directly benefit from rising long rates. For example, Puerto Rico bank Popular (BPOP) has really popped for us lately. BPOP often showers its shareholders with generous dividend raises. The firm has directly benefited from higher rates and profits, rewarding HY subscribers with 66% returns since the start of last year:

Buy Banks Like These When Long Rates Rise

With the 10-year yield on a tear, it feels like nothing can stop these stocks. However, we do need to keep an eye on the opposite (short) end of the yield curve.

Short rates are set by the Fed, and they will climb soon (possibly as soon as March.) Each Fed rate hike will flatten the yield curve, which could then put pressure on financial profits.

Short rates are going to rise because the Fed needs to tighten its loose (to put it nicely) monetary policy in order to reign in inflation. With price increases at a 40-year high, inflation has become a political issue. And the Fed, a political entity focused on self-preservation, needs to do what it can to take the pressure off of Main Street.

So we have the Fed leaving the bond market, which is bullish for long rates. But we have the same agency likely to hike short rates. We will see if bank spreads are able to further widen, or if profits need to be booked.

A purer play focused only on the long end of the yield curve is New Residential Investment (NRZ). NRZ is the largest non-bank owner of mortgage service rights (MSRs) in the world. These aren’t the loans themselves, but the rights to service these loans. A subtle but important difference.

Earlier this week, I received an email from Truist Bank that they collected my monthly mortgage payment. They had to work quite hard for it—(read: sarcasm)—they sweated a debit to my bank account. For their “effort” they received 0.25% of the payment.

Truist bought our MSR late last year. It’s a quarter-percent gravy train for the bank. The only thing that could foil their cash flow would be us refinancing our mortgage, in which case they would lose their right. Fortunately for Truist, we just refinanced last year and we won’t revisit our mortgage unless rates unexpectedly tank.

MSRs are the ultimate inflation train. This is reflected in NRZ’s book value, which rose 17% through the first three quarters of 2021.

With mortgage rates trending higher again, NRZ’s book value (BV) is rising, too. I anticipate management will report an even higher BV on its next earnings call.

Plus, this stock yields 9.2%. And unlike banks, NRZ doesn’t have to worry about the Fed raising short-term rates. Its only concern is the long end of the curve, which continues to slope higher as Powell packs his bags and leaves the bond market.

Now that’s the type of dividend that we want to own right now.

This is the secret to a secure retirement. Rather than buying stocks and hoping they’ll appreciate, we should instead focus on dividends that add up to 7%, 8% or even 9.2% annually.

This way we can retire on dividend income alone—without ever touching our capital.

Recent Comments