Most dividend investors understandably love the idea of an 8% No Withdrawal Portfolio. It’s a simple yet “game changing” idea that you don’t hear much from mainstream pundits and advisors.

Find stocks that pay 7%, 8% or more and you can retire comfortably, living off dividend checks while your initial capital stays intact (or even appreciates).

Now this strategy is a bit more complicated than simply finding 8% yields and buying them. Granted the recent stock market pullback has benefited investors like us because we can snag more dividends for our dollar. Yields are higher overall, and that’s a good thing.

Next we must smartly select the stocks that are going to pay our dividends securely – without tapping their own shares prices to pay us.

An Ideal 11.8% Dividend Payer That “Pivoted” Properly

As I write to you there are 123 stocks (trading on major US exchanges with market caps above $500 million) that yield 8% or more. A holiday basket of these dividends is going to be a mixed bag, however. While some of these stocks will shower you with quarterly (or even monthly) payouts with price appreciation to boot, others will lose some or all of your cash in price depreciation.

Of our 123 candidates, 99 have not delivered 40% total returns over the past five years. And this is the minimum we ask of an 8% payer – dish us our dividend and don’t lose our initial capital!

Granted this “back of the envelope” study is probably a bit harsh. We’re missing a few elite 8% payers that “graduated” to lower yields thanks to good stock performances. Still, the important lesson here is that 8% payout success is challenging (though not impossible, as we’ll see shortly).

Of these 99 high paying underperformers we have 57 “biggest losers.” These stocks have actually lost their investors money over the past five years. In other words, they have delivered their big dividends yet lost as much (or more) in price. Not good!

And remember, the S&P 500 returned 61% over the time period. So while we can expect our steadier strategy may underperform during roaring bull markets, we would expect a business to at least beat your mattress as a total return vehicle.

Exceptions? Sure. Business models can change, and past performance isn’t necessarily a predictor of future results.

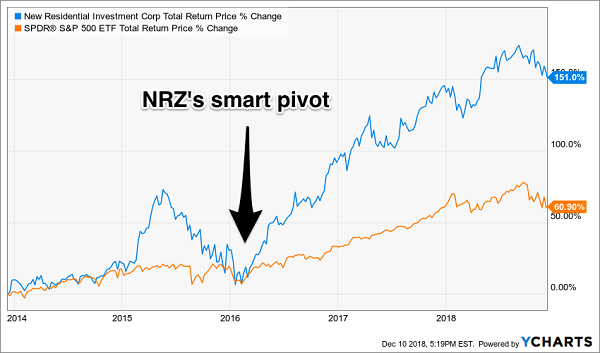

For example a subscriber recently wrote in to ask why New Residential Investment (NRZ) declined in price three years ago. Well, NRZ had a completely different portfolio now than it did then. Let me explain.

Mortgage REITs (mREITs) like NRZ typically buy mortgage loans and collect the interest. Their business model prints money when long-term rates are steady or, better yet, declining. When long-term rates drop, these existing mortgages become more valuable (because new loans pay less).

On the other hand, the mREIT gravy train usually derails when rates rise and these mortgage portfolios decline in value. Historically, rising rate environments have been very bad for mREITs and resulted in deadly dividend cuts.

But NRZ has actually doubled its investors’ money and the value of its own portfolio (its book value) in less than three years. Its secret? Rather than buying mortgages, NRZ has been investing in mortgage service rights (MSRs). This is “the right” to collect payments from a borrower. In other words, the firm doesn’t own these loans – it owns the rights to service these loans.

MSRs tend to rise in value when mortgage refinancing slows down. That’s exactly what happened, and this “pivot” has made many retirement riches. Happy NRZ investors have collected double-digit dividends while enjoying price appreciation to the tune of 151% total returns!

An Ideal 11.8% Dividend Payer

NRZ’s success story is, as discussed, more rare than not in 8%-ville. Let’s now call out a couple of popular “losers” that, despite their high current yields, don’t really belong in retirement portfolios.

2 Stocks Yielding Up to 20.1% to Avoid

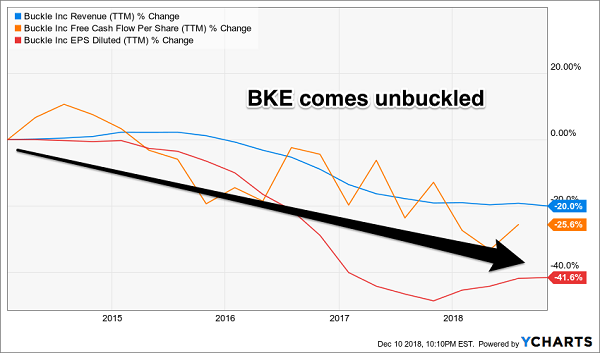

Fashion retailer Buckle Inc (BKE) has paid 14.7% of its current share price in dividends over the past twelve months (thanks to a $2 “special” payout). But the dividend well might run dry soon.

Buckle’s sales (the blue line below) have been in a slow-motion nosedive for three years, taking earnings (red line) and free cash flow (FCF, in orange) down with them:

Belt Tightens on Buckle’s Payout

Why are sales suffering? The firm’s revenues are drying up with its retail outlets. Buckle must pivot its business model to sell direct to consumers online in order to survive.

These “death of retail” market stresses, predictably, have driven up Buckle’s payout ratios: in the last 12 months, the company paid out more than it earned in dividends (140% of profits, to be precise), along with 123% of FCF.

I don’t like to see payout ratios above 50% from non-REITs, let alone 100%. This dividend has too high a risk of becoming unbuckled to belong in a No Withdrawal Portfolio.

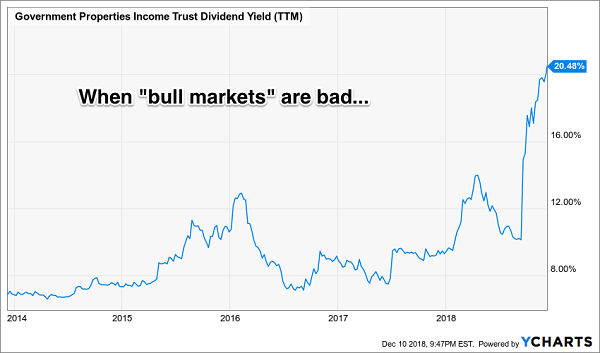

Government Properties Income Trust (GOV) meanwhile is a real estate investment trust (REIT) that frequently pops up on cute recession-proof dividend lists. Most of the company’s income comes from government entities, so it seems like a smart way to potentially tap Uncle Sam for rent checks.

And GOV’s big dividend usually qualifies itself for No Withdrawal consideration. However its recent runup in yield is actually a bad thing:

The Wrong Kind of Bull Market

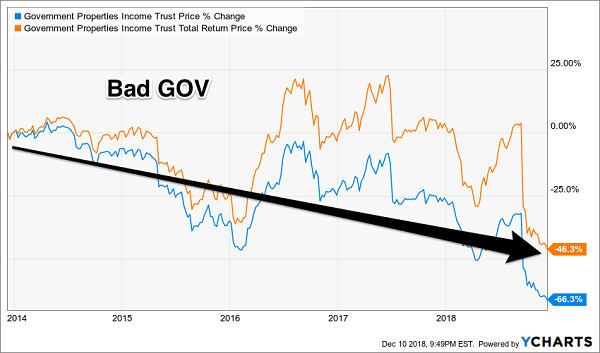

Problem is, this “bull market” in yield has happened because GOV’s stock has collapsed! Its share price is down 66% in five years. Even with the supposedly generous payout, GOV investors have the taste of stale government cheese in their mouths:

GOV Investors Down 46% With Dividends

There are a few reasons GOV has been crushed. First, its stated funds from operation (FFO) have been in decline. FFO per share is 24% lower today than it was five years ago, even though the dividend is the same.

Second, GOV may be overstating its FFO. The firm has been accused of conveniently excluding maintenance-related capital expenditures. Can you imagine old government buildings that don’t require any maintenance?

And finally, even if we give GOV the benefit of the doubt, it still seems to be paying cash it doesn’t have. Its annual dividend of $1.72 per share exceeds its trailing twelve-month FFO of $1.54. A more responsible 90% payout ratio (which is OK for a REIT) would mean a reduced dividend closer to $1.38 per share.

But the market is expecting worse, which is why GOV yields a “beyond contrarian” 20.1%. Stay away from this sketchy situation.

Yours Now: An Entire 19-Stock Portfolio With Safe Cash Payouts Up to 11%

As I showed you above, smart REITs like NRZ are your “dividend lifeboats” when the markets get rough. That’s because their massive cash payouts give you more of your profits in cash, rather than here today, gone tomorrow paper gains.

And by focusing on REITs and also bond funds with steady cash flow, you can make sure your nest egg stays intact—and grows for the future.

$40,000 in Income on $500k

I’ve got 6 more dividend plays to give you—all REITs and secure cash flowing funds—that fit this description to a T. Each one taps into the same kinds of surging trends as NRZ.

I’m talking 8% cash payouts, on average—enough to let you retire on dividends alone with a $500k nest egg, thanks to the $40,000 yearly income stream these defensive superstars give you.

That’s why I call this my “8% No Withdrawal Portfolio.” I can’t wait to show it to you.

That’s not all, either.

Because the newest issue of my Contrarian Income Report newsletter will publish the first week of January, with fresh updates on the 19 stocks and funds in the portfolio, handing our savvy CIR members massive yields up to 12%!

I want to send all 19 of these cash-rich plays your way, too. Don’t miss out. Click here and I’ll give you INSTANT access to my 8% No Withdrawal portfolio and the latest issue of Contrarian Income Report, with its 19 powerhouse income plays (yields up to 12%).

Recent Comments