One of the best things about closed-end funds (CEFs) is that, even though there are only about 500 or so of these 7%+ yielders out there, you can find CEFs that win in every kind of market.

So with a few clicks, you can build a diverse CEF portfolio yielding well north of 7%. (The 20 holdings in our CEF Insider service’s portfolio, for example, yield 7.7% on average and hold everything from tech stocks to municipal bonds and real estate investment trusts, or REITs.)

Below I’ve got an 8% monthly dividend payer that’s primed for “snap-back” upside as one group of stocks—those that sell discretionary products, from electronics to clothing—spring back to life. I’ll tell you more about this overlooked fund shortly, including how it uses a canny option strategy to fend off market volatility.

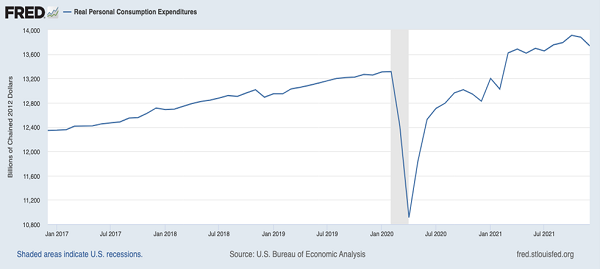

Spending Soars, Consumer Stocks Lag

I mention consumer-discretionary stocks because we’ve got an interesting setup in the sector, with the economy booming, Americans opening their wallets … and shares of retailers lagging.

As I write this, the typical consumer-discretionary stock has climbed 8% in the last year, compared to 16.5% for consumer staples and nearly 30% for market-leading financials. That disconnect makes zero sense, and it’s only a matter of time before these companies catch up, taking that CEF I just mentioned along for the ride.

I call rising consumer spending “the boom that everyone hates” because most folks are so focused on inflation, rising rates and geopolitical tensions that they just don’t want to hear about it! But it’s real, and it’s growing. The numbers tell the tale.

The first thing to consider is broader growth in the economy: while the fourth quarter of 2021 saw a renewed panic over Omicron, GDP still soared 5.7%, the highest growth rate in almost 40 years.

GDP growth is expected to continue in 2022, at a still-very-healthy 3.5%, according to economists surveyed by the Conference Board. More important than that headline number are the reasons for the growth: real consumer spending and non-residential investment, bolstered by imports and exports, are the highest categories to contribute.

Spending Continues to Soar as the Pandemic Eases

These details are important (and often overlooked) because there are different categories that can drive GDP growth, and some, like residential investment or government spending, are not the kinds of things you can rely on for a healthy economy: the former can create a real estate bubble and the latter can hinder governments’ ability to stimulate the economy in a downturn.

But as individual Americans spend more, there’s more reason to be optimistic about the growth of the economy in 2022. And even better, this spending isn’t adding to Americans’ debt load.

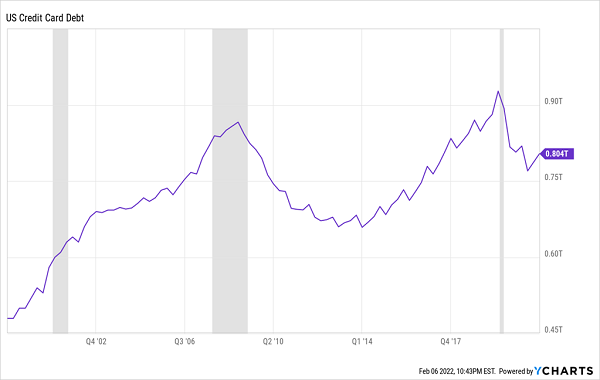

Spending Up, Debt Down

Since COVID-19 began, Americans have spent a lot of money paying down debt, helping credit card balances get to where they were at the end of 2016. They’re still in that general range, thanks to higher wages.

Those higher wages are also making that debt more manageable. An analysis from Nerdwallet suggests that the average US household has $6,006 in credit card debt, equivalent to a bit less than a month’s income for the median US household.

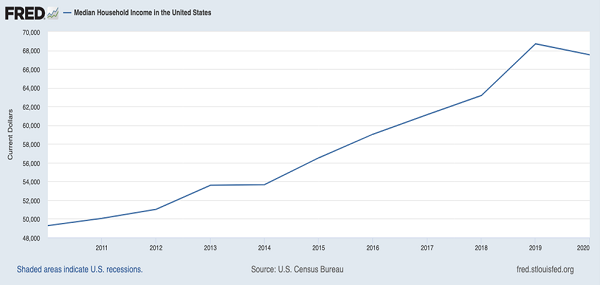

Higher Incomes = Easier Time Paying Off Debt

This ratio is unusually low; in 2019 it was a bit over a month’s wages, and at the peak of the subprime-mortgage crisis, it was equal to more than a month and a half of wages.

It’s also important to point out that we’re measuring this according to 2020’s wage numbers, the last year for which the federal government has data. Since incomes have increased significantly since then, it’s safe to say credit card debt is now far less than a month’s income for the median American household—an incredibly low level, historically speaking.

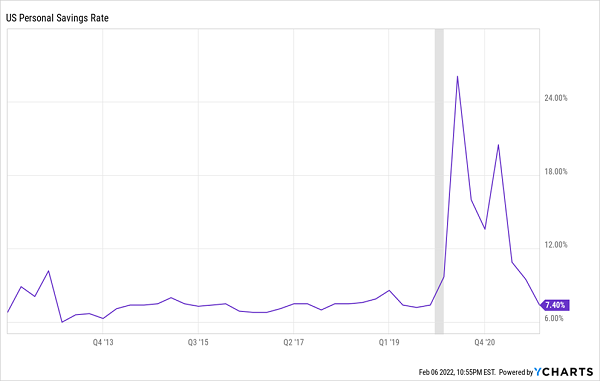

The reason for this is twofold: the stimulus checks people received in 2020 and 2021 were often used to pay down debt, and the mix of higher labor demand after the recent peak of the pandemic and hesitant spending during the pandemic encouraged more saving than normal.

A Massive Spike in Savings

Now, Americans are ready to spend more aggressively as Omicron fades. Additionally, deferred spending on things like cars (in short supply in 2021 due to chip shortages) will likely drive spending higher.

“Covered-Call” Funds Are a Smart Play in Today’s Market

Most folks would look to play the looming bounce in consumer-discretionary stocks through an ETF like the Consumer Discretionary Select Sector SPDR ETF (XLY), the benchmark for the space.

We CEF investors know better. We’d much rather buy in through a fund like the Eaton Vance Tax-Managed Buy-Write Fund (ETB), which holds consumer-oriented firms like Apple (AAPL), Home Depot (HD), Tesla (TSLA) and Walt Disney Corporation (DIS).

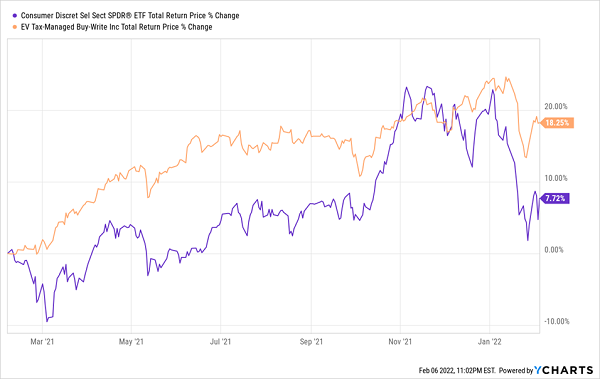

As mentioned, ETB pays an 8% dividend that comes your way monthly, and it’s handily beaten XLY over the past year, on a total-return basis, with much of its gain coming in dividend cash. (XLY, by contrast, yields a meager 0.6%.)

ETB Laps the Index

Another reason why ETB is a wise pick is that it is a “covered-call” fund, meaning it sells call options on its portfolio to generate extra income. These options give the buyer the right, but not the obligation, to buy the fund’s stocks when they hit a certain price. The buyer pays cash for that right, and the fund keeps this money no matter what the outcome of the trade.

These premiums help stabilize the fund in volatile times and give it extra income to enhance its dividend payout (which is why it pays more than the CEF average of around 7%).

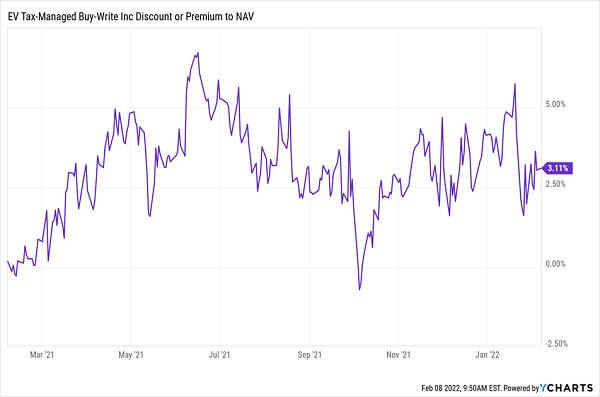

ETB’s Discount in Disguise

Finally, a word on valuation: as you can see above, ETB trades at a 3.1% premium to net asset value (NAV, or the value of the stocks in its portfolio). That looks expensive (who wants to pay a premium for anything?) But with CEF discounts, the important thing is the relative discount or premium, and 3.1% is about average for the past year. What’s more, ETB has traded at premiums north of 6% in that time, so we could see premium-driven gains here.

A 5-Fund “Safe-Dividend” CEF Portfolio Yielding 7.4%

One problem with ETB and other covered call funds is that their option strategies can hold back their gains in the long run, as their best stocks get “called away” when these option deals go through.

That makes them good funds to dip into and out of as market volatility ebbs and flows. But for the long term, I strongly recommend you take a serious look at the 5-CEF portfolio I recommend right here.

These 5 unloved picks yield an outsized 7.4% today, and they all trade at valuations much cheaper than that of ETB. In fact, these 5 funds are such bargains that I’m calling for 20%+ price upside from each of them in the next 12 months!

Plus, this portfolio is well-diversified: you’re getting funds holding blue chip stocks, pharma stocks, corporate bonds, real estate investment trusts (REITs) and cash-rich tech stocks.

Full details on this 5-CEF “mini-portfolio” are waiting for you now. Click here and I’ll give you these funds’ names, tickers, current yields, discounts, best-buy prices and everything else you need to know.

Recent Comments