“Not for individual resale.”

Ever see that label on a box of food, and scratch your head? Like who’s buying this big-mega bag of Chips Ahoy for the purpose of reselling the “individually packaged” helpings of cookies inside?

While you and I have better things to do than deconstruct groceries, we also have better ways to make money than deconstructing perfectly good bond funds.

My article about “preferred” shares a couple of weeks ago inspired a few questions. We’ve got a few adventurous income colleagues who are interested in unwrapping the perfectly good packaging we discussed. Let’s walk them back from this potential “Chips Ahoy moment” in a moment. First, let’s quickly recap the nuanced world of these income vehicles themselves.

Preferred shares are a brand of stock that most mainstream investors are not familiar with. The “first-level” types typically limit themselves to the common shares of stock, which are what you receive when you place an order to buy with your broker.

Preferreds are there, too, if you know where to look. Corporations issue them periodically to raise cash. These issues generally pay dividends that receive priority over those paid on common shares (a nice benefit during brittle economic times like these).

The dividends on preferreds are usually higher than on their common cousins, too. In this “zero interest rate” world, that’s a pretty sweet quality.

So how do we buy ‘em? Well, those of us with plenty of time on our hands these days could pop over to our sister website PreferredStockChannel.com and check out something like Citigroup’s Fixed Rate/Floating Rate Noncumulative Preferred Stock, Series K.

Wait. Series what?

If you can type in the right ticker, you’ll lock in a 6.4% yield, which certainly beats the 4.4% dividend on Citigroup’s mere “common” stock. But there are a few more reasons—aside from this initial headache—that we should instead choose a concierge to make this purchase for us.

First, there are two sides to any trade. If we buy the Series Ks ourselves, is there enough liquidity in the shares to make sure that we can get out when we want to sell?

Surely, there will be smart money hitting the sell button the moment something goes awry. If there’s a rush towards these exits, we should be aware that these are a bit narrow for rookies to finagle in and out of.

Second, preferred security selection is no joke. It requires a complex database with specific terms, interest rates, credit quality, and so on. Plus, analysis based on a variety of possible scenarios.

I prefer to “outsource” this research to a firm like Flaherty & Crumrine. And the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP) is the “go to” preferred fund for my Contrarian Income Report subscribers.

Don’t let the sleepy name put you to sleep. Since we added DFP to our CIR portfolio way back in October 2015, we’ve collected $8.39 in dividends—38%!—on our initial $22.26 purchase.

And guess what DFP’s top holding is? You got it—the Series Ks we mentioned earlier. Give us F&C as our preferred concierge, and we’ll let them worry about when to buy and sell the Ks.

Plus, we’re not interested in trading against the experts at F&C. We’d rather have that firm trading for us!

They also have access to free money. Well, just about free. As a closed-end fund (CEF), they are able to borrow at bargain basement rates. A no-brainer when buying safe preferreds paying 6%+.

What about fees? Sure, they charge a pretty annual penny at 1.06%, but we income VIPs can get that “comped” by buying smart.

August 2015 was one of those times. Our management fee was “on the house” because we were able to buy the fund at a discount to its net asset value (NAV). (Remember, fees for CEFs are debited directly from their NAVs. Every yield you see quoted at CIR is net of these fees.)

And because CEFs can trade at discounts to their NAVs—a benefit of the inefficiencies we can “exploit” in this underappreciated market, we can get our fees comped by purchasing funds when they trade at discounts to their NAVs. (If DFP sells for a 5% discount to NAV, for example, that’s well in excess of the 1.06% fee. It’s “free.”)

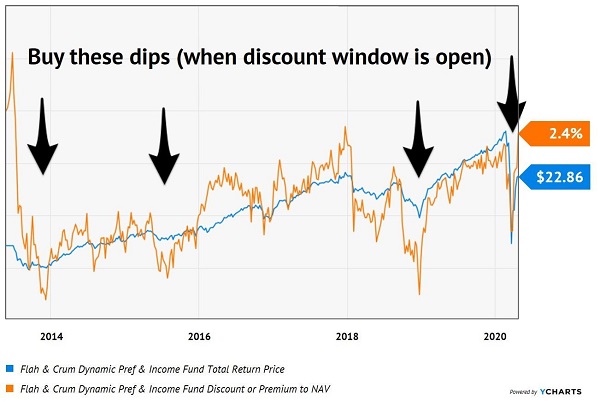

DFP is a great fund but it does go on sale every few years, for whatever reason (well, we know why—investors are crazy). When DFP is discounted, it’s the cornerstone of any dream retirement portfolio. The fund pays 7.1% and if you buy it at a big discount it tends to coincide with the dips in price nicely:

Buy These Discounts in DFP

Unfortunately, the fund has already bounced back from its pandemic sale, and it could be another year or two until we see DFP at a discount again. That’s OK because we have plenty of dream retirement stocks and funds to buy right now. I’m talking about immediate yields as high as 15% per year, and that’s not even considering price upside potential. Click here for my 4 favorite contrarian income investments yielding up to 15% right now, including names, tickers, current yields and more.

Recent Comments