The IRS already allows REITs (real estate investment trusts) to avoid paying income taxes if they pay out most of their earnings to shareholders. As a result these firms tend to collect rent checks, pay their bills and send most of the rest of the cash to us as dividends.

But the IRS considers the dividends you and I receive from our REITs “nonqualified” dividends. This means they are taxed at our regular income rate.

Until now, that is. REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the 2018 tax code. Investors will be allowed deduct 20% of their REIT dividend income (per U.S. News & World Report).

Interestingly, REIT income will be taxed at a lower rate than regular rental income (which would not receive the deduction). Which means if you don’t have a burning desire to change light bulbs and play landlord yourself, it will be cost-effective to simply sit back, make a few clicks and buy real estate stocks instead of physical properties!

Many subscribers have written in lately asking about the tax status of other income investments, too. While each investor’s tax situation is different, and I do not provide personalized tax advice, I have put together a general overview of the tax status of the dividends in our portfolio.

Municipal Bonds: Often Federal Tax-Exempt

Municipal – “muni” – bonds are issued by states, cities, and counties to raise money, usually for capital projects like public transportation and infrastructure improvements. Folks in high tax brackets love them because the interest paid by munis is often tax-exempt at the federal and/or state level.

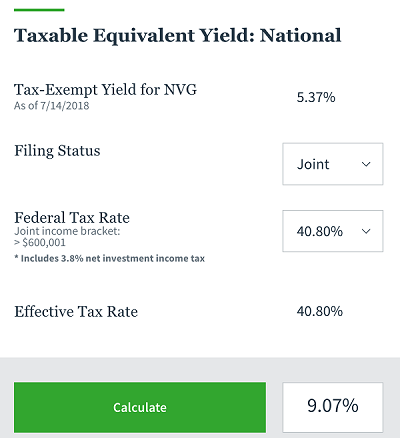

That’s right. The distributions you receive from funds such as the Nuveen Enhanced AMT-Free Municipal Credit Opportunities Fund (NVG) are federal tax-exempt. This means their listed nominal yield is actually much higher because of the tax advantage. And Nuveen provides a handy tool that lets you calculate the advantage – your “taxable equivalent yield” – on the fund’s website, which you can access here:

What looks like an okay-but-not-good-enough-for us 5.37% becomes a juicy 9.07%.

Qualified Dividends: Maximum 20% Tax Rate

Investors receive “qualified dividends” from the common shares they own in regular U.S. equities. Qualified dividends are taxed below the ordinary income rate. Their very favorable lower rate ranges from 0% to 20% depending on your tax bracket (read the specifics according to Wells Fargo Advisors here).

Closed-End Funds: A Mix of Tax Categories

Each closed-end fund (CEF) has one or more categories of income which are passed onto you, the investor. Your tax rate depends on the blend of these four potential sources:

- Interest payments

- Dividends

- Capital gains

- Return of capital

Fidelity has a comprehensive discussion of taxes on CEF distributions here.

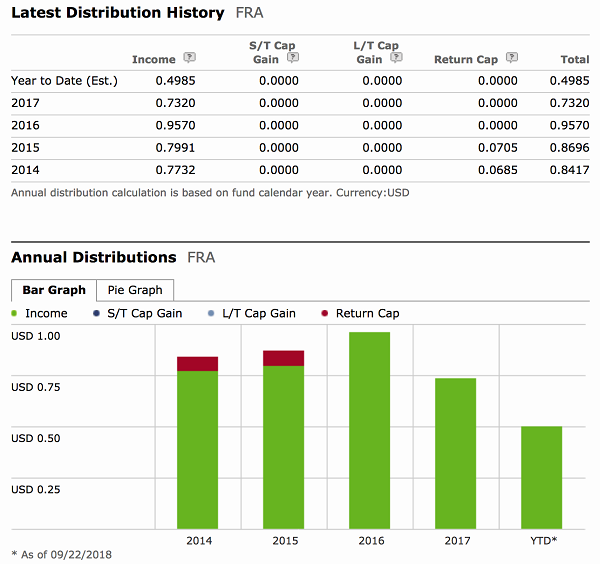

For the specifics on how your funds’ distributions were classified in previous years, you should contact them directly. This information typically appears on funds’ websites. Also, Morningstar.com does provide a breakdown of the fund’s latest distributions by income, short-term capital gains, long-term capital gains and return of capital. For example, here’s the breakdown for the BlackRock Floating Rate Strategies Income Fund (FRA):

Remember management’s primary goal is to make sure its distribution is fully funded. As a result it usually doesn’t provide investors with a “forecast” of how it plans to fund upcoming distributions, so that it has all options available at its disposal. But a quick review of previous distributions will give you a rough estimate of the current tax breakdown.

Avoiding the MLP “K-1 Headache”

Master limited partnerships (MLPs) are required to issue you a K-1 package at the end of the tax year. These are generally headaches for the person who does your taxes – whether it’s you or a professional.

A few years ago, my accountant calmly but sternly asked me to stop buying MLPs in my personal portfolio. I agreed, and I will return the favor to you too. There are better places to find high yield anyway, which is why we do not own any MLPs in our income-generating portfolios.

My Top 2 REIT Buys: Recession and Rate-Proof Landlords for 7.5%+ Yields with 25% Upside

Back to REITs – my two favorite tax-advantaged plays today are comfortably positioned in recession-proof industries. They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what President Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks, and then it sends most of the profits our way as dividends (a legal requirement to have REIT status).

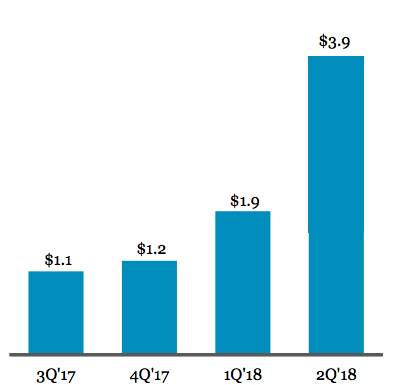

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

Quarterly Origination Volume ($ in Billions)

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, while it makes the investments which will drive its payout and share price higher from here.

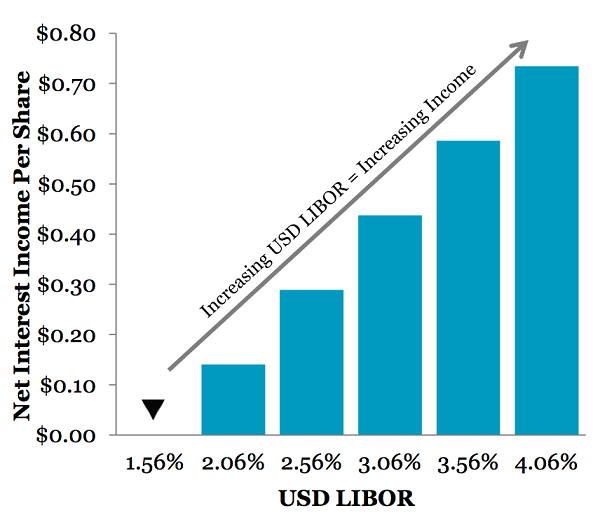

Plus, this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

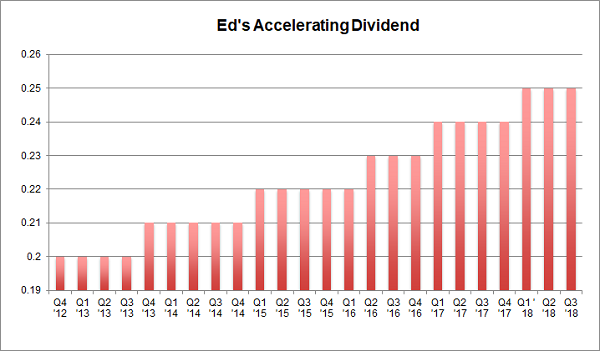

Its founder Ed admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well, his dream and plan were plenty – the visionary entrepreneur parlayed them into $6.7+ billion in assets!

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so it can afford to pay us shareholders more. And an accelerating payout is a flat-out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So, leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile, investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy (after we already own it, of course).

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever. Click here and I’ll share how you can get a complimentary copy of my premium REIT research.

Recent Comments