“Hey Brett. How’s the weather out there in California?”

My usual reply is “warm and sunny.” Simple. Gives the asker what they expect and keeps the pleasantries moving along.

If I was one for small talk, I would be tempted to mix in a confusing and way-too-detailed response. Like this:

“The weather? Well, Sacramento hit a low of 27 degrees in the early morning hours of February 24. And we cooked at an extreme 116 degrees on September 6. It has been quite the 12 months!”

Twelve months? Who cares about 12 months? Well, bond funds do.

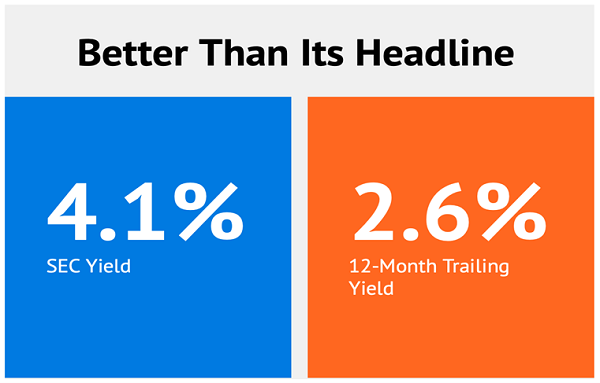

Last week, we highlighted the iShares 20+ Year Treasury Bond ETF (TLT): “It (TLT) boasts a 4.1% yield and has some serious upside potential.”

If you bought it then, nice work—TLT popped 3.9% the very next day. (That’s good for a comical 200%+ annualized return.)

Upside? Check. And even after the pop, TLT is still paying 4.1%.

Please note that many websites will say that TLT pays just 2.6%. This is the too-detailed-not-too-useful weather report version of this fund’s yield.

Yes, over the past 12 months, TLT has paid 2.6%. But second-level thinkers don’t care about what happened. We care about now and what’s ahead.

More recently (last 30 days), TLT has dished dividends at a 4.1% pace. This is what we’re buying—a fund likely to pay 4.1% ahead, over the next 12 months, not the last 12.

How do we find this? “SEC Yield” reflects the interest the fund earned, minus expenses, over the past 30 days. It’s fairer and more accurate calculation of what’s current and ahead than is the trailing twelve-month (TTM) yield.

With the SEC calculation, we’re changing our focus from the back of the car mirror to the road ahead. What’s TLT likely to pay over the next 12 months? Use SEC yield: 4.1%.

One of the most popular pickup requests from my daughters is to let one of their stuffed animals (“stuffies”) drive us home. Our stuffie guest driver will look at everything around except for the road ahead, while the kids laugh and scream: “Look at the road!”

Rear-view-staring is great for laughs, but not for buying bonds. Don’t be that stuffie.

Now, why do we care about SEC yields versus TTM yields all of a sudden? Because we are buying bonds to take advantage of a bounce in fixed income.

Bonds have had a bad year, to put it lightly. But hope is on the way as yields begin to “top out.”

I’m not sure the reason is cause for cheer. The Federal Reserve is engineering a recession to tame inflation. Recessions are bullish for duration (how long before the bond “ends”—is redeemed by the issuer) because rates fall. Which sends bond prices higher.

Since we are heading into a slowdown, we don’t want to buy just any old bond. Credit quality is going to come into focus. Heck, last week we saw a crypto exchange explode. More stuff is going to bust in the months ahead.

So, we want to own only the safest paper. TLT fits the bill because it owns US Treasuries, backed by the full faith, credit and printing press of America.

Again, for you contrarians scoring properly, TLT yields 4.1% (SEC). Not 2.6% (the flawed TTM calculation you see everywhere other than here).

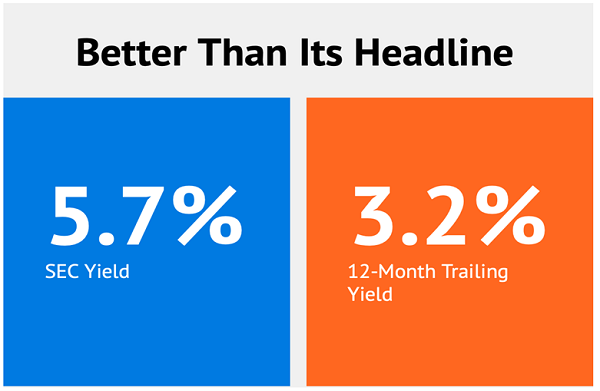

The iBoxx $ Investment Grade Corporate Bond ETF (LQD) is another good fund for a bond bounce. The fund holds-duh-investment grade corporate credit. Its bonds are secure.

Generally speaking, we rarely buy bond ETFs (we prefer CEFs). But when we do, we cherry pick deals. And LQD is poised to rally as bonds get up off the mat.

Once again, LQD’s yield is better than it looks. The computers say 3.2%, but don’t be fooled. The fund’s SEC Yield is a fantastic 5.7%.

Again, credit risk is not a big concern with LQD. It owns investment-grade bonds, the highest quality paper on the planet.

LQD never yields this much. Don’t be fooled by the wrong weather report! Other sites say that the fund pays just 3.2%, but this is the TTM yield. According to the SEC calculation, LQD yields a fantastic 5.7%.

Another nice thing about funds like TLT and LQD is that they dish out their dividends every month. Which means their credits will hit your account as your bills are being paid.

Most companies pay their dividends quarterly. Which means we must wait 90 days in between payments.

No thanks! Give us payouts every 30 days, so that our payouts line up with expenses. That’s a beautiful monthly-dividend-circle-of-life.

And for those of you not satisfied with 4.1% or even 5.7% annual yields, well, we can do better. While 5.7% will net us $57,000 in dividend income on a million-dollar portfolio, why not shoot for an elite 8% (and $80,000 in yearly income) if it’s available?

Thanks to the bond bear of 2022, these 8% yields are real. And spectacular. And paid monthly.

Just for you, my dear contrarian, I put together a special list of 8%+ dividends that are paid monthly. These bond funds are also likely to bounce in the weeks and months ahead. Please click here for my monthly dividend “hot list” now.

Recent Comments